Money Factor Calculator: Convert to APR & Expose Dealer Markups

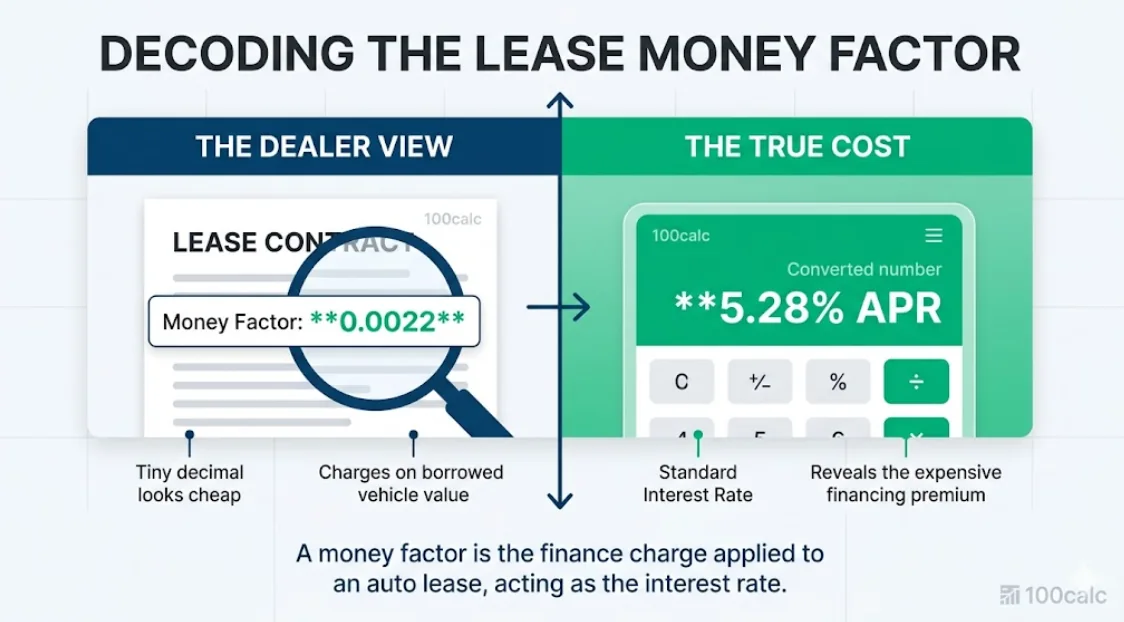

A money factor determines your auto lease interest rate. Car dealerships present this rate as a tiny decimal to hide the true cost of borrowing. You can convert a lease money factor to a standard Annual Percentage Rate (APR) by multiplying the decimal by 2400.

Stop guessing what your car lease actually costs. Finance managers often inflate this hidden number to increase their profit margin. A tiny fraction like 0.00350 actually equals a massive 8.4 percent interest rate.

This free money factor calculator instantly converts that confusing decimal into a clear APR. It breaks down your exact monthly rent charge. Enter your lease quote below to catch inflated rates and secure a fair deal before you sign any contract.

Quick Facts

- Primary Goal: Find your true lease APR

- Conversion Rule: Multiply the decimal by 2400

- Warning Sign: APR over 7 percent for prime credit

- Bonus Feature: Reverse engineers hidden dealership rates

- Updated Jun 16, 2026

- Reviewed by 100Calc Research Team

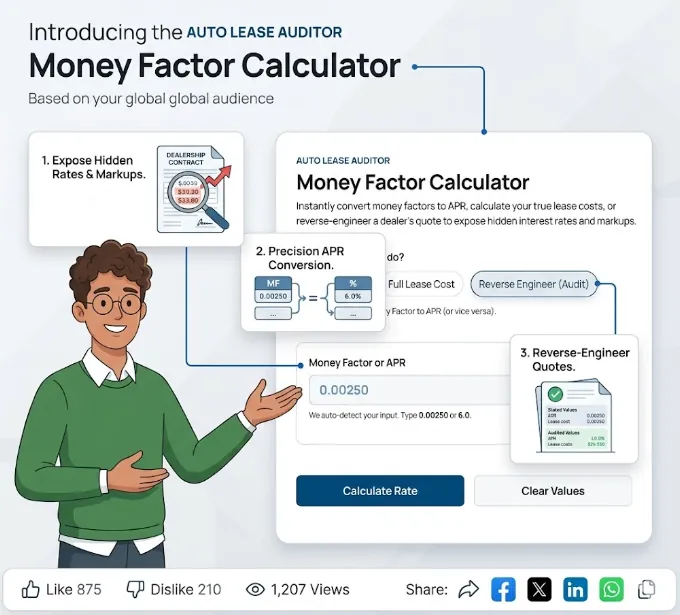

Auto Lease Auditor

Money Factor Calculator

Instantly convert money factors to APR, calculate your true lease costs, or reverse-engineer a dealer's quote to expose hidden interest rates and markups.

Instantly convert a Money Factor to APR (or vice versa).

Equivalent APR

Money Factor:

Monthly Lease Breakdown

How do you calculate the money factor to an interest rate (APR)?

What is a good money factor on a lease?

Explore More Calculators

Wondering where your paycheck vanishes? Use this free Ramsey budget calculator to expose leaks, fund your Four Walls, and force your balance to exactly…

Try calculatorCalculate exact cost per minute for salaries, factory overhead, and electricity. Convert hours and minutes to money instantly with our free CPM calculator app.

Try calculatorStop underbidding. Use this Heavy Equipment Hourly Rate Calculator to track O&O costs, fix idle time leaks, and set professional 2026 billing rates instantly.

Try calculatorBanks round transfers to 1,000 point blocks. Use our calculator to find exact points needed for 2026 award flights and avoid stranded airline miles.

Try calculatorExplore Related Tools

What Your Equivalent APR Means

The output converts the dealership decimal into a standard percentage. This number exposes the actual borrowing cost of your auto lease. It tells you exactly how much extra cash the dealer is keeping.

Understanding Your Result

Your result breaks down the finance fee. Dealerships call this the rent charge. It represents pure profit for the bank and the dealer.

A tiny decimal often hides a massive interest rate. Converting it to an Annual Percentage Rate levels the playing field. You can finally compare this car lease against a traditional auto loan.

Is Your Result Good or Bad?

A good result means your equivalent APR sits below six percent. This usually happens when manufacturers offer promotional buy rates to move inventory.

A bad result triggers our dealer markup warning. This happens when the finance manager inflates the base rate to earn a larger commission. An APR over seven percent for prime credit signals a bad deal.

What You Should Do Next

- Demand the base buy rate from the finance manager immediately.

- Check for manufacturer lease specials on the official brand website.

- Compare the total rent charge against buying the vehicle outright.

- Walk away if the dealer refuses to remove their hidden markup.

A Quick Example to Test

Let us say a dealer offers you a luxury sedan lease. Enter these values into the tool above to test the math.

Input:

- Net Capitalized Cost: $45,000

- Residual Value: $27,000

- Quoted Rate: 0.00315

- Term: 36 Months

Process:

The system multiplies the decimal by 2400. It calculates your monthly rent charge using the vehicle values.

Result:

- Equivalent APR: 7.56 percent.

- Monthly Rent Charge: $226.80.

Meaning:

The tiny decimal hides a high interest rate. You will pay over two hundred dollars every month just in finance fees. This rate triggers a markup warning for prime credit buyers. You must negotiate a lower rate before signing.

How to Use the Money Factor Calculator

This tool reverses dealership math to expose your true lease costs. The system breaks down confusing fractions into clear percentage rates and monthly fees. Follow these simple instructions to audit your auto lease quote quickly.

Choose a Calculation Mode

The tool offers three distinct functions based on your needs. Pick the quick converter to translate a simple decimal into a percentage. Select the full lease cost option to break down your entire monthly payment. Use the reverse engineer mode to audit a quoted payment.

Enter the Quoted Finance Values

Type the exact money factor decimal provided by the dealership. The system automatically detects whether you entered a decimal or a standard percentage. If you are auditing a hidden rate, input the total monthly payment the sales manager quoted you instead.

Provide the Vehicle Price Data

Add your final negotiated vehicle price after trade-ins or cash down. Then input the residual value provided in your lease contract. The calculator uses these two figures to separate the actual depreciation of the car from the monthly finance fees.

Select Your Estimated Credit Tier

Pick the credit score range that best matches your financial profile. This step is completely optional but highly recommended. The system uses this tier to compare your quoted rate against national averages. It helps flag inflated dealer numbers accurately.

Review the True Cost Breakdown

Hit calculate to reveal the true Annual Percentage Rate hidden inside the lease. The tool displays your exact monthly rent charge in plain dollars. Check the warning section to see if the dealer padded your quote with a hidden interest markup.

How do you reverse-engineer a hidden lease rate?

Read your printed lease quote from the dealership. To find your hidden interest rate, subtract the actual vehicle depreciation from the quoted monthly payment. This isolates the pure finance fee. This is the biggest sticking point for modern car buyers who only focus on the monthly payment.

This classic dealership scenario hides the true borrowing cost. Buyers often struggle to spot inflated finance charges on the showroom floor.

Use these inputs in the calculator:

Net Capitalized Cost: $40,000

Residual Value: $25,000

Lease Term: 36 Months

Quoted Monthly Payment: $550.00

Process:

The system isolates the base depreciation first, then uncovers the rent charge to find the rate.

- Depreciation: ($40,000 – $25,000) ÷ 36 = $416.67

- Rent Charge: $550.00 – $416.67 = $133.33

- Money Factor: $133.33 ÷ ($40,000 + $25,000) = 0.00205

- APR Conversion: 0.00205 × 2400 = 4.92%

Final Result:

- Hidden Money Factor: 0.00205.

- True APR: 4.92 percent.

Meaning:

The dealership is charging you nearly five percent interest on this lease. If you have excellent credit, you should immediately ask the finance manager if this is their base buy rate or a marked-up sell rate.

What is a Money Factor?

A money factor is the finance charge applied to an auto lease. It acts as the interest rate on the borrowed vehicle value. Dealerships express this fee as a tiny decimal instead of a standard annual percentage to make the borrowing cost look virtually invisible on paper.

Buying a car means paying interest on the entire loan balance. Leasing works differently because you only finance the depreciation of the vehicle. However, the bank still purchases the entire car for you to drive, and they require a profit on that tied-up cash.

This leasing fee calculates the cost of borrowing their asset. It charges you a monthly rate based on the average value of the car during your contract. Salesmen prefer the decimal format because a fraction like 0.00250 looks significantly less intimidating to a buyer than a standard loan rate.

Think of it like renting an apartment. You do not own the building, but you pay the landlord a premium for living there. This finance charge is the premium you pay the leasing company for driving their new vehicle off the lot.

The Micro Insight

Negotiating a car lease requires knowing the true cost of borrowing. Financial managers use small fractions to make expensive rates look cheap. Expose the math to protect your wallet.

How the Money Factor Calculator Formula Works (Complete Breakdown)

This money factor calculator uses standard automotive banking logic to expose your true lease costs. It relies on two primary equations to break down confusing dealership quotes. The first translates fractions into standard percentages. The second isolates the exact dollar amount burning on interest every month.

The Math Behind the Quotes

The system relies on a universal conversion constant to turn lease decimals into standard Annual Percentage Rates. It then uses the total average value of your vehicle to calculate the exact monthly finance fee.

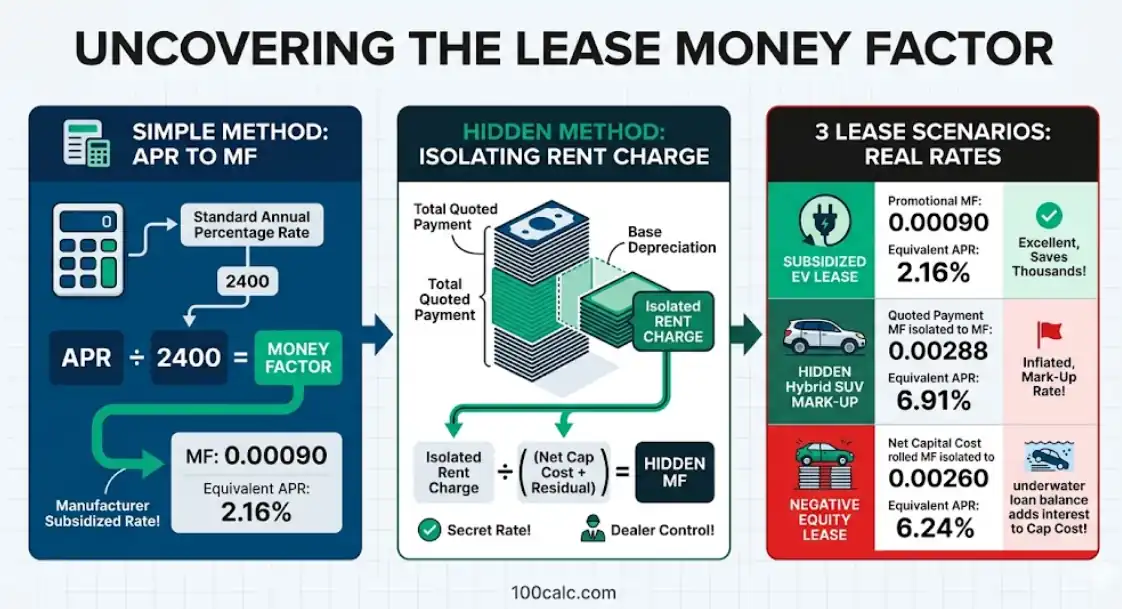

APR Conversion Formula:

APR = Money Factor × 2,400

The Math Behind the Quotes

Monthly Rent Charge = (Net Capitalized Cost + Residual Value) × Money Factor

Explaining the Math

The first equation relies on the number 2,400. This is a mathematical constant used universally in auto finance to account for twelve months in a year and convert a decimal into a percentage.

The second equation calculates your actual monthly interest fee. It adds your negotiated vehicle price to the estimated final value. It multiplies that total by the money factor decimal to determine how much the bank charges you to borrow their asset.

Expected Money Factor Variables Breakdown

Each value below represents a specific component of your lease agreement. Entering these numbers accurately guarantees a perfect calculation that matches your dealership paperwork.

Money Factor

This tiny decimal represents your lease interest rate. Dealerships use this format to make expensive financing look incredibly cheap on standard lease contracts.

Equivalent APR

This represents the Annual Percentage Rate of your lease fee. It converts the confusing dealership decimal into a standard format you can compare against normal auto loans.

Net Capitalized Cost

This is the final negotiated price of the vehicle. It includes any extra fees but subtracts all down payments, factory rebates, or trade-in values.

Residual Value

This figure represents the estimated worth of the car when your lease contract ends. The bank sets this value, and it is almost never negotiable.

Rent Charge

This is the exact dollar amount you pay in pure interest every month. It represents the fee the bank charges you for tying up their cash in a depreciating asset.

Another Example Calculation (Step-by-Step)

Let us see how the system reverse-engineers a dealership quote using fresh numbers. This process isolates the hidden finance fee and exposes the true borrowing rate.

Given:

- Net Capitalized Cost = $42,000

- Residual Value = $26,000

- Lease Term = 36 Months

- Quoted Monthly Payment = $600.00

Calculation:

Monthly Depreciation = (42,000 - 26,000) ÷ 36 = $444.44

Monthly Rent Charge = 600.00 - 444.44 = $155.56

Money Factor = 155.56 ÷ (42,000 + 26,000) = 0.00228

APR = 0.00228 × 2400 = 5.47%

Result:

- Equivalent APR: 5.47%

- Money Factor: 0.00228

- Monthly Rent Charge: $155.56

Meaning:

This calculation proves the dealership is charging you an interest rate of 5.47 percent. You are spending over one hundred and fifty dollars every month just on finance fees. If you have super-prime credit, this rate is slightly above average and should be negotiated.

Accuracy Behind the Money Factor Auditor

This tool relies on standard automotive banking formulas to ensure absolute precision. Our system reverses dealership math to expose the true cost of your lease and prevents hidden finance markups. You can trust these outputs because the underlying engine mirrors the exact accounting logic used by major auto lenders.

Key Features & Benefits

- Converts confusing lease decimals into standard percentage rates instantly

- Calculates exact monthly rent charges to expose total finance costs

- Isolates actual vehicle depreciation from inflated dealership borrowing fees

- Reverse-engineers hidden interest rates directly from quoted monthly payments

- Estimates credit-based dealer markups using national average auto loan data

Technical Process

Rate Conversion Logic

The engine multiplies the decimal by 2400 to find the APR or divides the APR to find the money factor.

Lease Breakdown Processing

The system isolates the principal from the finance fee using your negotiated capitalized cost and residual value inputs.

Markup Detection Output

The tool compares your calculated APR against national average interest rates for your credit tier to flag inflated quotes.

How do you calculate the money factor?

To calculate the money factor from an interest rate, divide the Annual Percentage Rate by 2400. If you only have a monthly lease quote, subtract the vehicle depreciation from the payment first. Then divide that remaining rent charge by the sum of your capitalized cost and residual value.

What is the money factor for a subsidized EV lease?

A buyer wants an electric vehicle featuring a promotional manufacturer interest rate.

Use these inputs in the calculator:

- Net Capitalized Cost: $45,000

- Residual Value: $28,000

- Lease Term: 36 Months

- Quoted Rate: 0.00090

Process:

Depreciation equals $472.22 per month ($17,000 ÷ 36). The rent charge is $65.70 per month (($45,000 + $28,000) × 0.00090).

Result:

- Equivalent APR: 2.16%

- Base Monthly Payment: $537.92

- Monthly Rent Charge: $65.70

Meaning:

The manufacturer subsidized this deal heavily to move electric inventory. A 2.16 percent APR is excellent and saves the buyer thousands in finance fees compared to standard bank rates.

How do you find the hidden money factor on a hybrid SUV?

A family gets a high monthly quote on a popular hybrid and wants to check the real interest rate.

Use these inputs in the calculator:

- Net Capitalized Cost: $48,000

- Residual Value: $30,000

- Lease Term: 36 Months

- Quoted Payment: $725.00

Process:

Base depreciation is $500.00 per month ($18,000 ÷ 36). Subtracting this from the $725 payment leaves a $225.00 rent charge. The secret factor equals $225 ÷ ($48,000 + $30,000).

Result:

- Hidden Money Factor: 0.00288

- Equivalent APR: 6.91%

- Monthly Rent Charge: $225.00

Meaning:

The dealership marked up the interest rate because this specific hybrid is in high demand. The family should negotiate this inflated sell rate down to the base buy rate.

How does negative equity change your lease money factor?

A driver rolls a $4,000 underwater loan balance into a new compact car lease.

Use these inputs in the calculator:

- Net Capitalized Cost: $32,000 (includes negative equity)

- Residual Value: $17,000

- Lease Term: 36 Months

- Quoted Rate: 0.00260

Process:

Depreciation costs $416.67 per month ($15,000 ÷ 36). The rent charge is $127.40 per month (($32,000 + $17,000) × 0.00260).

Result:

- Equivalent APR: 6.24%

- Base Monthly Payment: $544.07

- Monthly Rent Charge: $127.40

Meaning:

Adding negative equity increases the total capitalized cost immediately. This higher starting balance forces the driver to pay interest on both the new car and the old loan at the same time.

Quick rule to remember

Dealerships rely on tiny fractions to make expensive financing look cheap. Never sign a contract based solely on the monthly payment. Take control of your negotiation and convert every quote into a true percentage first.

Money Factor Result Benchmarks Explained

Your equivalent APR tells you exactly how much your lease truly costs. Comparing your money factor against current national averages helps you spot bad deals immediately. Use this breakdown to see if your quoted rate matches your credit score or hides dealer markups.

| APR Range | Money Factor | Label | Typical Profile | Action Required |

|---|---|---|---|---|

| Under 4.0% | < 0.00166 | Excellent | Super Prime (780 plus) | Sign the deal. This represents a subsidized manufacturer rate. |

| 4.1% to 6.5% | 0.00170 to 0.00270 | Average | Prime (660 to 779) | Normal market rate. Verify it matches the base bank rate. |

| Over 6.5% | > 0.00270 | High / Markup | Sub-Prime or Dealer Markup | Stop and negotiate. Ask them to remove the inflated sell rate. |

Heads-up: Promotional lease rates change monthly. Always check the official manufacturer website for current buy rate specials.

Interpretation

Any rate below four percent is a fantastic deal usually backed by factory incentives. A rate jumping past six or seven percent means you face credit penalties or severe dealership markups. Always compare this percentage against standard auto loan rates before signing any lease paperwork.

Pro Tip

Call multiple local dealerships and ask for their base lease money factor on the exact same car. Compare those numbers to find the true baseline and refuse to pay any markup above it.

How to Improve Your Money Factor Result

Your calculated equivalent APR is only useful if it changes your dealership strategy. Use these results to secure a lower monthly payment, block hidden markup fees, and stop overpaying for basic borrowing costs.

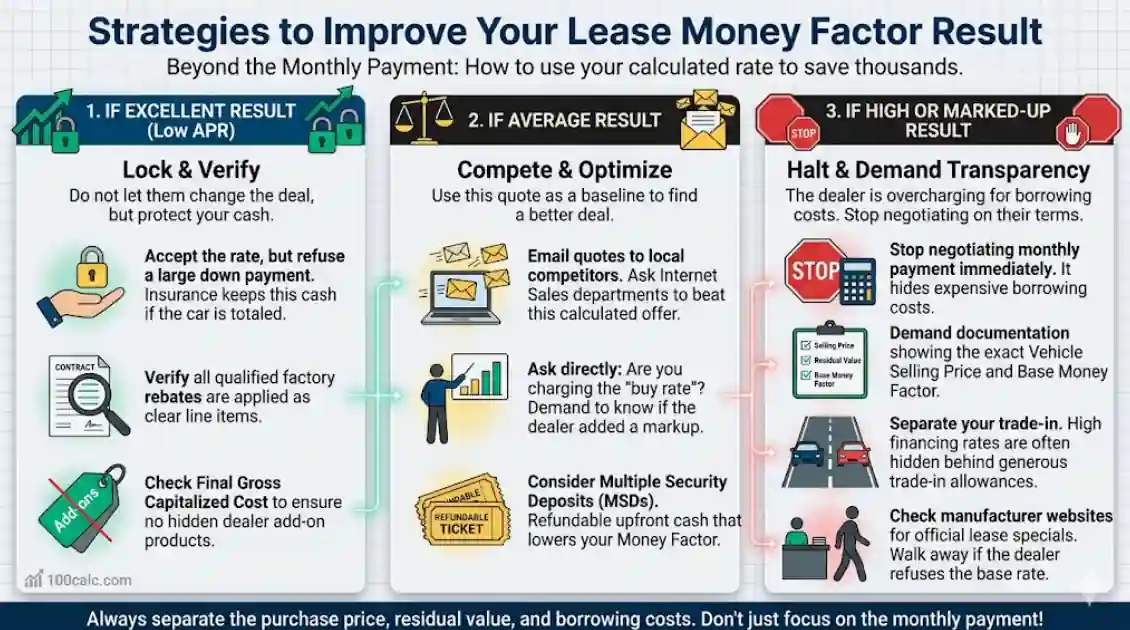

For Excellent Results

Lock in this promotional rate immediately, but refuse to make a large down payment. If the leased vehicle gets totaled, the insurance company keeps the car and your upfront cash disappears forever. Instead, verify that the dealer applied all your qualified factory rebates as clear line items. Review the final capitalized cost to ensure they did not hide expensive add-on products inside this cheap financing.

For Average Results

Email this calculated quote to several local dealerships and ask their internet sales departments to beat it. Understand that “Captive Lenders” (like Toyota Financial or BMW Financial) set the base buy rate, not the local dealer. Ask your finance manager directly if they are charging the captive bank’s base rate or adding their own markup. You can also ask to use Multiple Security Deposits (MSDs). These fully refundable upfront deposits lower your money factor directly and save you hundreds in finance fees over the lease term.

For High or Marked-Up Results

Stop negotiating based on the monthly payment immediately. Demand a single document showing the exact vehicle selling price, residual value, and base money factor. Separate your vehicle trade-in from this deal completely, as dealers often hide high interest rates behind generous trade allowances. Check the official manufacturer website for factory-subsidized lease specials, and walk away if the local dealer refuses to honor the base rate.

You Might Also Find These Helpful

Personal Finance 4

No tools published here yet.

Explore Related Tools

Common Mistakes When Calculating Your Lease Money Factor

Car buyers often miscalculate their lease terms because dealership contracts use confusing financial jargon. Entering the wrong vehicle values or misunderstanding how interest applies can ruin your negotiation strategy. Avoid these frequent errors to ensure your finance audit is completely accurate.

- Subtracting the residual value from the capitalized cost instead of adding them together for the rent charge.

- Putting large cash down payments to hide a high interest rate inside a lower monthly payment.

- Focusing entirely on the monthly payment target while completely ignoring the underlying finance rate.

- Accepting the dealership sell rate without asking the finance manager for the original bank buy rate.

- Typing the money factor as a standard percentage instead of the exact decimal printed on the quote.

Frequently Asked Questions (FAQs)

Can you negotiate the lease money factor?

Yes. Dealerships often inflate the bank’s base interest rate to increase their profit margin. You should always ask the finance manager for the original buy rate and refuse to pay their inflated markup.

What is the money factor for a Tesla lease?

Tesla acts as its own direct lender and uses a fixed money factor for all leases. The company does not negotiate or mark up lease rates. Your specific interest charge depends entirely on your credit tier and current factory promotions.

How do dealers hide lease interest rates?

Dealerships present the lease interest as a tiny decimal fraction instead of a standard APR percentage. A rate like 0.00350 looks very small to a buyer. It actually equals a massive 8.4 percent interest rate.

What is the difference between the buy rate and sell rate?

The buy rate is the minimum interest rate the lending bank approves based on your credit score. The sell rate is the higher percentage the dealership actually charges you. The financial difference between these two numbers becomes pure dealer profit.

What is the APR for a 0.002 money factor?

A money factor of 0.002 equals exactly a 4.8 percent APR. You find this by multiplying the decimal by 2400. This rate represents an average interest charge for buyers with prime credit scores negotiating a standard auto lease.

Do dealerships have to disclose the money factor?

No. Dealerships are not legally required to print the money factor decimal on your lease contract. Federal law only mandates the disclosure of the total rent charge in dollars. You must calculate the exact rate yourself using the total payment and vehicle values.

Does a down payment lower the money factor?

No. Putting cash down on a lease reduces your capitalized cost, but it never changes the underlying interest rate. The money factor remains exactly the same regardless of how much cash you pay upfront.

Can Multiple Security Deposits (MSDs) reduce my lease rate?

Yes. Many captive auto lenders allow you to put down fully refundable security deposits at signing to reduce your money factor. Each deposit buys down the interest rate slightly. You receive this money back at the end of your contract.

What is the 1 percent rule in car leasing?

The one percent rule suggests that a good monthly lease payment should not exceed one percent of the vehicle’s total MSRP. If a car costs fifty thousand dollars, the ideal payment sits around five hundred dollars with zero money down.

Is the lease money factor based on my credit score?

Yes. Banks use tiered credit brackets to assign your base lease rate. Excellent credit scores unlock the lowest promotional money factors. Lower credit scores trigger higher risk brackets and significantly more expensive finance fees.

How does the rent charge differ from the money factor?

The money factor represents the interest rate percentage disguised as a decimal. The rent charge is the actual dollar amount you pay in interest over the life of the lease. The factor dictates how high that total fee climbs.

Does negative equity increase the lease money factor?

Rolling negative equity into a new lease does not change the base money factor itself. It does increase your total capitalized cost. That higher starting balance forces you to pay much more total interest because the rate applies to a larger loan amount.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.