Personal Finance Calculators: Run the Numbers Before the Bank Does

What are personal finance calculators? They are free digital tools that reveal the exact math behind your money. You can estimate monthly loan payments, uncover true interest rates, and build a rock-solid household budget. These tools turn confusing bank terms into clear numbers.

Most people blindly accept the monthly payment a lender offers. That is a massive mistake. You need to know the true cost of debt before signing any paperwork.

Browse our full suite of personal finance tools below. Find the exact numbers you need to compare loans, value credit card points, and track your daily expenses with total confidence.

- Instant free estimates

- Standard banking math

- No signup needed

Find the Best Personal Finance Tools

Pick the exact tool you need to map out your money. Every calculator below solves a specific financial problem. Select the option that matches your current goal. You will get clear numbers and instant results to help you plan your next move.

Personal Finance 5

Wondering where your paycheck vanishes? Use this free Ramsey budget calculator to expose leaks, fund your Four Walls, and force your balance to exactly…

Try calculatorCalculate exact cost per minute for salaries, factory overhead, and electricity. Convert hours and minutes to money instantly with our free CPM calculator app.

Try calculatorStop underbidding. Use this Heavy Equipment Hourly Rate Calculator to track O&O costs, fix idle time leaks, and set professional 2026 billing rates instantly.

Try calculatorDealerships hide massive lease rates in tiny decimals. Use this money factor calculator to convert MF to APR instantly and expose hidden markups.

Try calculatorBanks round transfers to 1,000 point blocks. Use our calculator to find exact points needed for 2026 award flights and avoid stranded airline miles.

Try calculatorOther Finance tools you may find useful

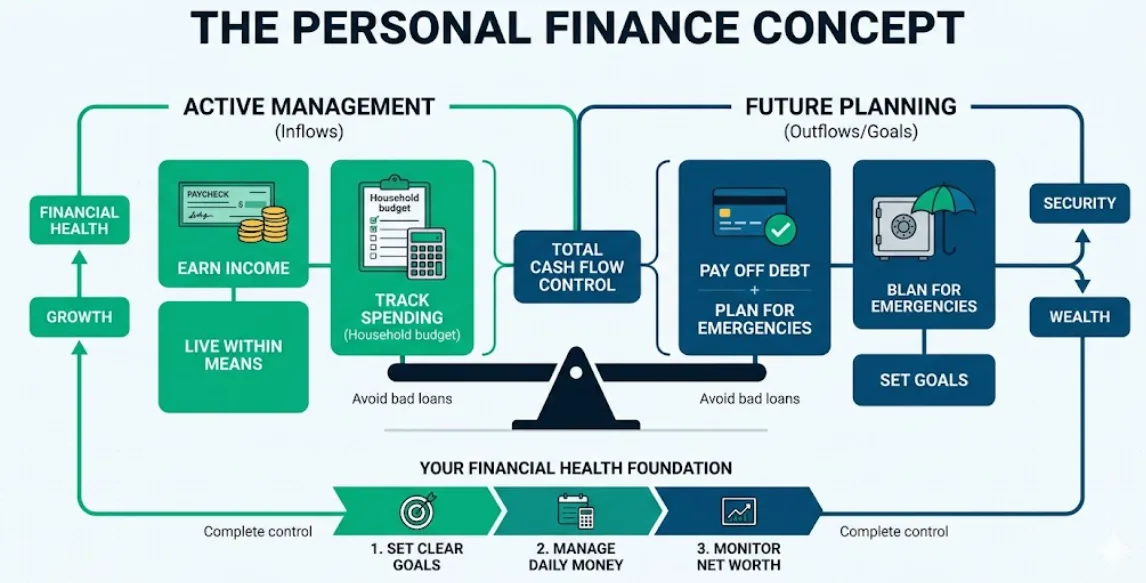

What Is Personal Finance?

Personal finance is the process of managing your individual money. It covers how you earn income, track daily spending, build savings, and pay off debt. Good financial management means living within your means today while planning safely for future expenses and unexpected emergencies.

Managing your money requires balancing what comes in against what goes out. Many people focus only on their paycheck. Real financial health looks at your entire cash flow. This includes your monthly household budget, everyday expenses, and your overall net worth.

Imagine you bring home a high salary but carry heavy credit card balances. Your income looks great on paper. Your actual financial picture is weak because interest payments eat up your extra cash. Fixing this requires a clear action plan.

Building a strong foundation means setting clear financial goals. You must allocate funds for basic living costs, smart debt management, and an emergency fund. Tracking these specific numbers gives you complete control over your future.

Micro Insight

Mastering these basic concepts stops financial stress before it starts. Knowing your exact numbers helps you avoid bad loans and keeps your daily spending aligned with your real priorities.

Stop Guessing Your Debt: What These Financial Tools Actually Reveal

A great personal finance calculator turns raw numbers into clear answers. You plug in basic details like total loan amounts or interest rates. The system immediately shows your monthly costs and payoff timelines. This lets you make safe decisions without ever touching a complicated spreadsheet.

Popular Tasks

Estimate monthly loan payments

See exactly what a new car or personal loan costs every thirty days.

Compare true interest rates

Uncover the real cost of debt hidden behind confusing bank terms.

Calculate payoff timelines

Find out exactly the month and year you will finally be debt-free.

Build realistic household budgets

Track your real income against fixed living expenses to find extra cash.

Core Inputs Used

Total loan amount

The full dollar amount you plan to borrow or currently owe a lender.

Annual Percentage Rate (APR)

The yearly interest rate your bank charges you to use their money.

Loan term length

How many months or years you have left to pay off the final balance.

Monthly take-home income

Your actual spendable cash after taxes and regular paycheck deductions.

Why Bank Documents Differ From Online Estimates

Our personal finance tools process your inputs using proven banking math. We apply exact amortization schedules and standard compounding formulas to calculate true costs. This gives you a precise baseline to build budgets, compare loans, and verify lender offers before signing any official paperwork.

How These Calculations Work

These tools map your core inputs against a fixed financial timeline. The system takes your starting balance, applies the stated interest rate, and divides it across the total months. It instantly outputs your required monthly payment and the total lifetime interest.

Most debt tools use a declining balance model. As you make regular payments, the principal amount shrinks. This lowers the interest charged in the following cycle. The system seamlessly recalculates this shift for every single payment period.

Insight: Banks use this exact declining balance logic to heavily front-load interest payments during the first few years of a new loan.

Logic & Formula Approach

We rely on standard amortization equations for loans and exponential growth models for savings. This ensures your projections mirror the exact mathematical practices used by retail banks, credit unions, and certified financial planners rather than using rough guesswork.

We do not use simple flat-rate assumptions. Flat-rate math hides the true cost of borrowing and makes debt look much cheaper than it actually is. Our underlying logic breaks down the compound effect so you see the real, long-term financial impact.

Insight: Lenders often quote simple interest verbally to secure a deal, but they will process your actual loan using compound interest.

Accuracy & Real-World Factors

Mathematical accuracy depends heavily on the hidden variables your lender applies behind closed doors. Our tools provide a mathematically perfect estimate based strictly on the raw numbers you enter. However, real-world payments typically shift if your bank adds extra origination costs.

Taxes and insurance also distort the final picture. A pure calculation cannot automatically predict your local property tax rate, mandatory auto insurance premiums, or sudden changes in inflation.

Insight: Always compare the Annual Percentage Rate (APR) instead of the base interest rate, as the APR officially includes those hidden processing fees.

When Results May Vary

Your actual bank documents will generally look slightly different than an online estimate. This variance happens because lenders often calculate interest based on the exact calendar days in a month, whereas standard calculators assume every month is perfectly equal.

Additionally, online tools assume perfect payment behavior. If you make a payment two days late or split your payments bi-weekly without alerting the system, your actual amortization schedule will immediately drift away from the original estimate.

Insight:A variation of ten to twenty dollars a month is completely normal when moving from a free online estimate to a legally binding contract.

Updates & Improvements

We regularly update our underlying calculation models to ensure they match current financial regulations. We audit our logic processing to guarantee that changes in standard loan structures or new budgeting methods reflect accurately in your final results.

The financial industry constantly shifts how it handles specific technical cases, like early payoff penalties or variable rate adjustments. When the official banking standard changes, we adjust the formulas behind the scenes.

Insight: Using an outdated spreadsheet formula from five years ago is the fastest way to accidentally underestimate your current debt obligations.

Currency-Agnostic Banking Math

Our calculation models are entirely currency-agnostic. Whether you are budgeting in US Dollars (USD), British Pounds (GBP), Indian Rupees (INR), or UAE Dirhams (AED), the underlying amortization and compound interest formulas remain exactly the same. You can use these tools safely anywhere in the world.

Insight: Because standard financial math does not change across borders, you can enter your local currency into any of our tools and get perfectly accurate local results.

Important note: Results are estimates. For major decisions, verify with a qualified professional.

Are You Overpaying? Standard Financial Benchmarks

Knowing your exact monthly payment is only half the battle. You also need to know if that payment is actually fair. These standard benchmarks help you judge whether a lender is offering a competitive rate or trying to trap you in bad debt.

| Financial Metric | Status | Target Range | What It Means For You |

|---|---|---|---|

| Debt-to-Income (DTI) | Healthy | Below 36% of gross income | Lenders view you as a safe borrower for new loans. |

| Personal Loan Rates | Average | 10% – 15% (Good Credit) | Rates vary wildly; always compare multiple bank offers. |

| Housing Costs | Warning | Above 30% of gross income | You are likely "house poor" and lacking extra savings. |

Heads-up: These are general guidelines. Exact rates depend heavily on your current credit score and economic inflation.

Why Tracking Your Cash Flow Matters

Managing your money requires balancing what comes in against what goes out. Many people focus only on their gross paycheck. Real financial health looks at your actual leftover cash flow. These tools help you figure out exactly how much salary you have left after your fixed costs and loan payments are covered each month.

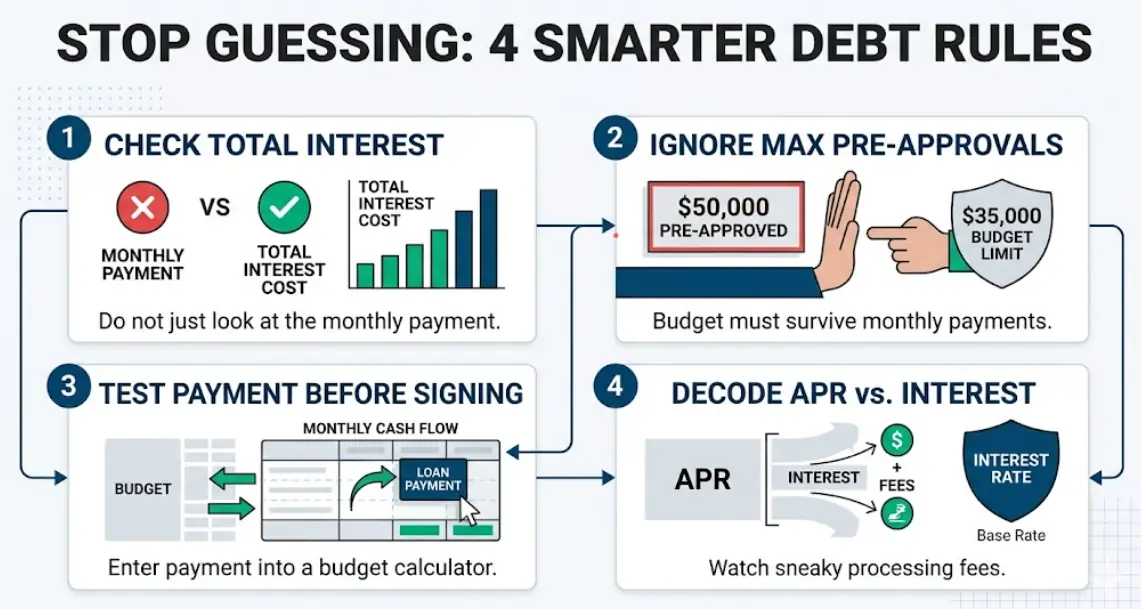

Stop Guessing: 4 Rules for Smarter Debt Decisions

- Always check the total interest: Do not just look at the monthly payment. A lower payment over a longer term often costs thousands more in hidden interest.

- Do not max out pre-approvals: Just because a bank approves you for a $50,000 loan does not mean your household budget can survive the monthly payments.

- Test your budget before signing: Enter your proposed loan payment into a budget calculator. Live with that artificial expense for a month to see if it breaks your cash flow.

- Watch the difference between APR and Interest: Interest is the base rate. APR includes the sneaky processing fees banks charge to open the account.

- Work backward from your monthly limit: Do not ask a bank how much you can borrow. Decide the maximum monthly payment your budget can handle, and use a loan calculator to reverse-engineer your maximum borrowing capacity.

The 5 Most Expensive Calculator Mistakes People Make

- Entering gross income when the tool requires actual net take-home pay.

- Forgetting to include property taxes and insurance in monthly mortgage estimates.

- Assuming credit card minimum payments will eventually clear the total debt balance.

- Using an outdated interest rate instead of checking the current daily market average.

- Ignoring inflation when planning a long-term retirement savings goal.

Frequently Asked Questions (FAQs)

How do I calculate a personal loan monthly payment?

You need your total loan amount, the annual interest rate, and the loan term length. Enter these into a personal loan payment calculator to see your exact monthly cost, whether you are taking out a $10,000 or $50,000 loan.

Does a longer loan term mean I pay less?

A longer term, like a 5-year or 10-year loan, lowers your required monthly payment. However, it increases the total amount of interest you pay to the bank over the life of the loan. Stretching debt out makes it much more expensive overall.

What makes a good budget calculator?

A great budget calculator helps you track income against the cost of living and debt payments. It shows you exactly where your money goes so you can stop thinking and start saving. A reliable tool focuses on real cash flow rather than strict accounting rules.

Can I calculate a personal loan rate for free?

Yes. You can use our free tools to reverse-engineer your payments and find the exact interest rate a bank or dealership is charging you. This reveals the true cost of borrowing before you commit to any lender agreement.

How do I find the average interest rate for multiple loans?

You need to calculate a weighted standard based on the current balance of each loan. A debt consolidation calculator does this automatically by combining your separate balances into one clear percentage. This helps you decide if refinancing is a smart move.

How can I see how much of my payment goes toward interest?

An amortization calculator breaks down every single monthly payment into principal and interest. During the first few years, most of your money simply pays off bank interest. Tracking this schedule shows you exactly when you start making a real dent in the actual debt.

Should I calculate my budget using gross or net income?

You must always build your budget using your net take-home pay. Using your gross income is a common mistake that leads to severe overspending. Your net income reflects the actual, usable cash that lands in your bank statement after taxes and employer benefits.

Does using an online finance calculator hurt my credit score?

No. Using an online financial calculator has absolutely zero impact on your credit score. These tools do not pull your credit report or trigger a “hard inquiry.” They simply run mathematical formulas based on the numbers you manually type into the boxes.

How do extra monthly payments affect my loan balance?

Most personal loans use a “reducing balance” model. Paying even a small extra amount each month directly reduces your principal balance. This forces the bank to charge you less interest the following month, shaving years off your loan term.

How much of an emergency fund should I calculate into my budget?

Standard financial guidelines suggest saving three to six months of essential living expenses. If you have a variable income or work in an unstable industry, you should adjust your budget to build a runway of up to twelve months for maximum security.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.

Ready to Take Control of Your Money?

You now know exactly what to look for. It is time to stop guessing and map out your actual cash flow. Choose the personal finance calculator that solves your immediate problem. Every tool gives you instant clarity without requiring any complicated math. Enter your numbers and make your next big financial move with total confidence.