Ramsey Budget Calculator: Build a Zero-Based Plan in Seconds

A zero-based budget forces your total income minus your expenses to equal exactly zero. The Ramsey budget calculator helps you assign every single dollar a job before the month begins. You start by funding your “Four Walls”—housing, utilities, food, and transportation. Next, you assign limits to lifestyle spending and wealth building. If you carry debt, activate the Gazelle Intense mode. This instantly cuts discretionary spending and funnels that cash directly into your debt snowball.

Stop letting random one-off expenses drain your bank account. Generic percentages fail when real life happens. Use this tool to expose hidden spending, protect your basic needs, and take total control of your money today.

Quick Facts

- Primary Goal: $0 Left to Assign

- Core Focus: The Four Walls (Needs)

- Debt Strategy: The Debt Snowball

- Updated Jun 16, 2026

- Reviewed by 100Calc Research Team

Zero-Based Planner

Ramsey Budget Calculator

Take control of your money. Build a perfect zero-based budget, protect your "Four Walls," and calculate your maximum debt payoff power.

Left to Assign (Goal: $0)

Debt Snowball Power:

Budget Allocation Breakdown

What is the 70 10 10 10 budget rule?

What is Dave Ramsey's biggest concern for 2026?

Is EveryDollar no longer free?

What is Dave Ramsey's 25% rule?

Explore More Calculators

Calculate exact cost per minute for salaries, factory overhead, and electricity. Convert hours and minutes to money instantly with our free CPM calculator app.

Try calculatorStop underbidding. Use this Heavy Equipment Hourly Rate Calculator to track O&O costs, fix idle time leaks, and set professional 2026 billing rates instantly.

Try calculatorDealerships hide massive lease rates in tiny decimals. Use this money factor calculator to convert MF to APR instantly and expose hidden markups.

Try calculatorBanks round transfers to 1,000 point blocks. Use our calculator to find exact points needed for 2026 award flights and avoid stranded airline miles.

Try calculatorExplore Related Tools

What Your "Left to Assign" Number Means

Your “Left to Assign” number reveals your exact budget accuracy before the month begins. This figure represents the gap between your total income and your planned expenses. It proves whether you have assigned every single dollar a specific job.

Understanding Your Result

This number exposes your financial reality on paper. It tells you exactly how much cash is floating around without a purpose. Idle money creates financial stress because it usually disappears on random impulse purchases.

This result acts as an early warning system. It shows you a planning error before you actually spend the money. Fixing this number guarantees your paycheck will cover your Four Walls and fund your goals.

Is Your Result Good or Bad?

A perfect zero means excellent financial health. You successfully assigned every dollar a job. Your income perfectly matches your planned outgoing cash. You have total control over your monthly cash flow.

A positive number means idle cash is sitting in your account. You have not finished budgeting. Leaving money unassigned is bad because it slows down your wealth building.

A negative number signals immediate danger. You are planning to spend money you do not have. This situation forces you to rely on credit cards to cover basic bills. You must fix this imbalance instantly.

What You Should Do Next

- If your result is exactly zero: Stop budgeting. Follow your plan and track your expenses throughout the month to ensure you stick to these exact limits.

- If your result is positive: Assign the extra cash immediately. Drop the remaining balance directly into your debt snowball or funnel it into your emergency savings.

- If your result is negative: Cut your lifestyle spending first. Reduce your restaurant or recreation limits until the balance hits zero.

A Quick Example to Test

Let’s say you want to test how unassigned funds affect your budget.

Input:

- Total Take-Home Pay: $4,000

- Four Walls Total: $2,500

- Lifestyle Total: $400

- Wealth (Giving + Snowball): $600

Process:

The calculator subtracts your total planned expenses ($3,500) from your income ($4,000).

Result:

Left to Assign: $500.

Meaning:

You still have $500 floating around without a purpose. You must go back to the calculator and increase your debt snowball by exactly $500. This forces your final result down to a perfect zero.

How to Use the Ramsey Budget Calculator

This zero-based budgeting tool helps you assign every single dollar a job before the month starts. It calculates your baseline income, prioritizes your basic survival needs, and tracks unassigned cash. This ensures your final balance hits exactly zero.

Set Your Income Baseline

Select your pay frequency from the options provided. Type in your total take-home pay. The system automatically converts weekly or bi-weekly paychecks into a reliable monthly total. This creates your starting budget baseline.

Fund Your Four Walls First

Enter your planned expenses for housing, utilities, food, and transportation. These categories represent your basic survival needs. The calculator tracks these costs against your total income to ensure your fundamental living expenses are secured.

Assign Discretionary Limits

Input your planned spending for lifestyle categories like clothing, recreation, and restaurants. The system continuously deducts these amounts from your remaining baseline. This step exposes how much cash you are leaking on non-essential purchases.

Determine Wealth Goals

Add your planned giving amount. Enter the base payment you plan to make toward your debt snowball or savings. Every dollar entered here directly reduces your unassigned cash balance and builds your financial momentum.

Balance to Exactly Zero

Adjust your category limits until your "Left to Assign" number hits exactly zero. If the number is negative, cut lifestyle expenses. If the number is positive, funnel that extra cash directly into your debt snowball category.

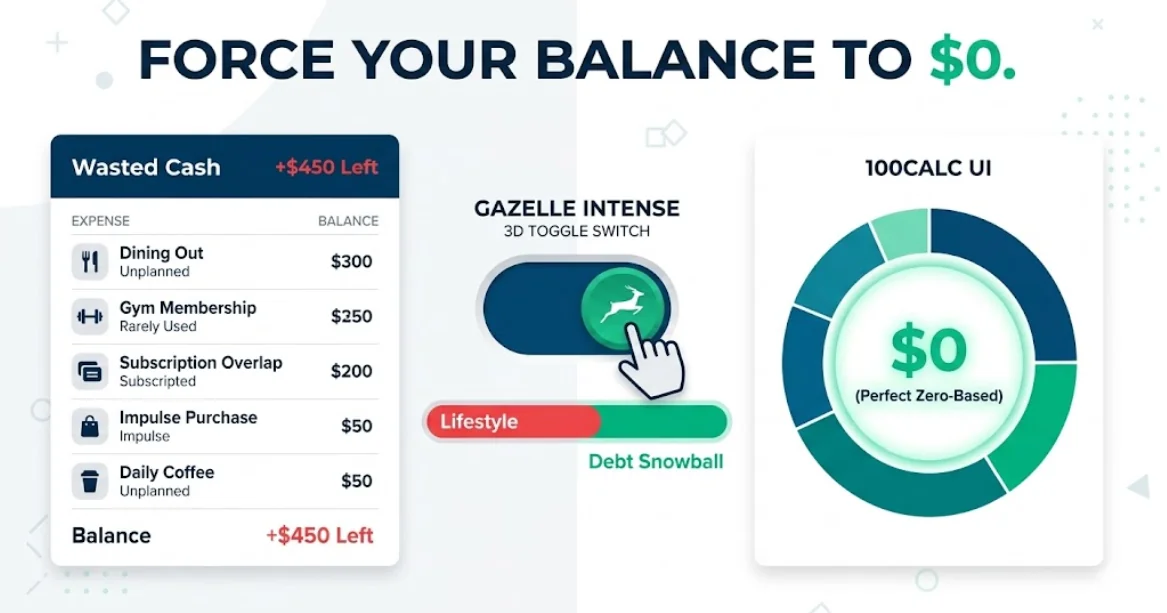

How does the Gazelle Intense toggle change a zero-based budget?

Read your current lifestyle expenses. Activating this mode instantly strips all non-essential spending to zero. It automatically transfers that exact dollar amount into your debt snowball.

Use these inputs in the calculator:

Total Take-Home Pay: $6,000

Four Walls Total: $3,000

Lifestyle Total(Restaurants/Fun): $800

Debt Snowball: $2,200

Process:

The calculator balances the budget perfectly to $0. You then click the Gazelle Intense toggle. The system overrides the $800 lifestyle budget to zero. It automatically adds that $800 directly to your debt payoff category

Final Result:

- Left to Assign: $0

- Debt Snowball Power: $3,000

Meaning:

You instantly increased your debt payoff speed by $800 a month without earning any extra income.

Accuracy Behind the Ramsey Budget System

This calculator runs strict zero-based accounting logic. It automatically normalizes varying pay frequencies into standard monthly figures so your bills align perfectly with your actual cash flow. This prevents the common budgeting error of underestimating expenses during three-paycheck months.

Key Features & Benefits

- Converts weekly and bi-weekly pay into accurate monthly totals automatically

- Highlights the critical 25 percent maximum housing threshold visually

- Gazelle Intense toggle cuts lifestyle spending to zero instantly

- Routes recovered lifestyle cash directly into your debt snowball automatically

- Tracks unassigned funds in real-time to enforce strict zero-based rules

Technical Process

Data Normalization

The engine multiplies weekly pay by 52 or bi-weekly by 26 and divides by 12 to establish a true monthly baseline.

Allocation Tracking

The system continuously subtracts your active category inputs from your monthly baseline to find your exact unassigned cash.

Gazelle Rerouting

Activating this mode overrides lifestyle variables to zero and mathematically injects that exact dollar amount into your snowball output.

How the Ramsey Budget Formula Works (Complete Breakdown)

The Ramsey budget calculator uses a strict zero-based accounting formula. It subtracts your planned expenses from your total monthly income to find your exact unassigned cash. Understanding this specific math helps you control where your money flows and stops paycheck leaks instantly.

Explaining the Math

The primary equation removes your three major expense buckets from your net income. This reveals if you have idle cash or a dangerous monthly deficit.

The override equation activates when you decide to crush debt aggressively. It wipes out discretionary spending entirely and transfers those exact funds straight into your payoff goals.

Standard Zero-Based Formula:

Left to Assign = Monthly Take-Home Pay - (Four Walls + Lifestyle + Wealth Building)

Gazelle Intense Override Logic:

New Lifestyle Expenses = $0.00

New Debt Snowball = Base Debt Snowball + Clothing + Recreation + Restaurants

Expected Ramsey Budget Variables Breakdown

Each variable represents a physical bucket for your money. Defining these inputs clearly prevents you from accidentally overspending or leaving idle cash in your checking account.

Take-Home Pay

This is your cleared income after taxes and payroll deductions hit your bank account. It acts as the mathematical ceiling for your entire monthly plan. Using your net pay rather than gross income ensures you are budgeting with actual possessed cash, preventing accidental overdrafts.

The Four Walls

These basic survival requirements keep your household running safely. This combined bucket covers your rent or mortgage, groceries, basic utilities, and essential transportation costs. Ramsey strictly caps housing at 25% of your net pay, a mathematical limit you must follow to avoid becoming house-poor.

Debt Snowball

You aggressively throw this total cash amount at your smallest debt each month while paying minimums elsewhere. Increasing this specific number accelerates your journey to financial freedom. Once you become completely debt-free, this variable shifts toward saving 15% for your retirement.

Gazelle Intense

This behavioral modifier overrides your normal math to maximize payoff speed. It strips all non-essential lifestyle spending—like streaming subscriptions, vacations, and restaurants—to absolute zero instantly. Every recovered dollar automatically fuels your snowball to eliminate consumer debt in record time.

Another Example Calculation (Step-by-Step)

Let us see how the calculator builds a zero-based plan using real numbers. Funding your basic needs first protects your household while exposing unassigned cash.

Given:

- Take-Home Pay = $5,200

- Four Walls Total = $3,100

- Lifestyle Total = $800

- Wealth Total = $1,300

Calculation:

Total Allocated = 3100 + 800 + 1300 = 5200

Left to Assign = 5200 - 5200 = 0.00

Result:

- Left to Assign: $0.00

- Budget Status: Perfect Zero-Based Budget

Meaning:

Every dollar earned has a strict purpose before the month begins. Your income perfectly covers your basic needs, fun money, and wealth goals. You successfully built a balanced financial plan without leaving any cash idle.

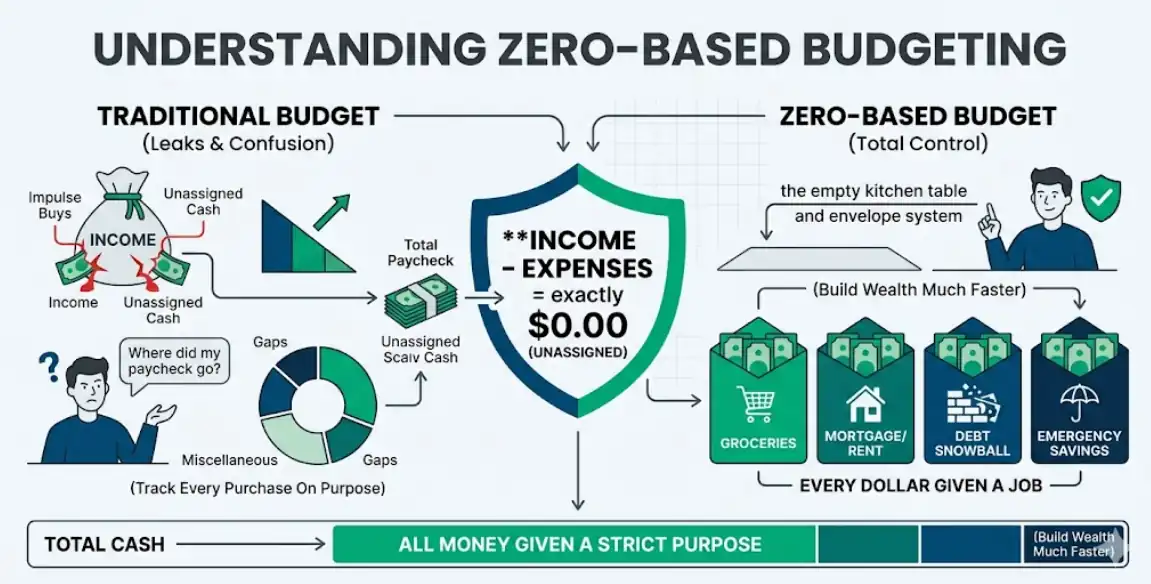

What is a Zero-Based Budget?

A zero-based budget forces your total income minus expenses to equal exactly zero dollars. You assign every single dollar a specific job before the new month begins. This method ensures no money sits unassigned. It stops you from wondering where your paycheck went at the end of the month.

Imagine you withdraw your entire paycheck in physical cash. You place that money on your kitchen table. You must put every single dollar bill into a labeled envelope. One envelope pays for groceries. Another covers your car payment. The last envelope holds your debt snowball cash.

Your kitchen table must be completely empty at the end of this process. You do not actually drain your checking account to zero. You simply leave no cash without a strict purpose. Idle money usually disappears on random impulse purchases.

Giving your money a name changes your daily habits. You stop reacting to surprise expenses. You take total control over your financial future.

Why this matters

This method builds strict personal accountability. You crush debt and build wealth much faster when you plan every purchase on purpose.

How do you calculate a Ramsey zero-based budget?

Calculate a Ramsey zero-based budget by subtracting all planned expenses from your total monthly take-home pay. Group your spending into basic needs, lifestyle, and debt payoff. The goal is reaching exactly zero dollars left over. Every dollar must have an assigned job before the month begins.

How do you budget a $2,000 bi-weekly paycheck?

A worker gets paid every other week and wants a reliable monthly plan without doing manual calendar math.

Use these inputs in the calculator:

- Pay Frequency: Bi-Weekly

- Take-Home Pay: $2,000

- Four Walls Total: $2,500

- Lifestyle Total: $800

- Wealth Total: $1,033

Process:

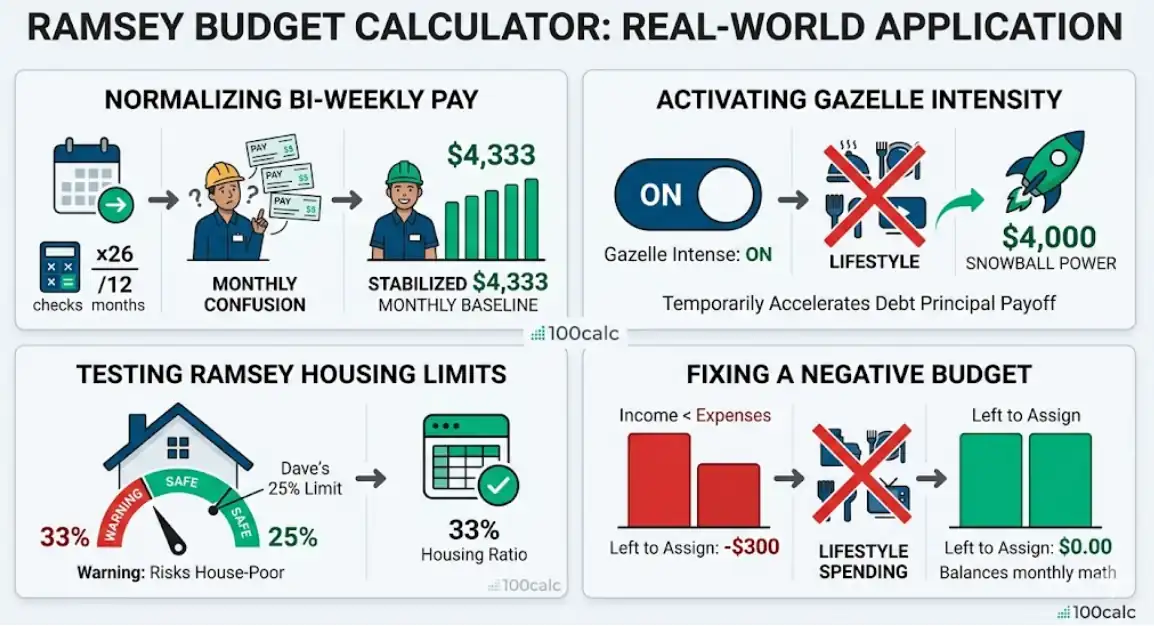

The system multiplies $2,000 by 26 paychecks and divides by 12 to establish a true $4,333 monthly baseline. It then subtracts the $4,333 allocated total from that income.

Result:

- Left to Assign: $0.00

Meaning:

Bi-weekly pay creates “extra” checks twice a year. Normalizing the math prevents budget shortages during standard two-check months. You now have a smooth, predictable plan.

What does Gazelle Intense look like for an $8,000 income?

A couple wants to crush their student loans fast by temporarily cutting out restaurants and vacations.

Use these inputs in the calculator:

- Pay Frequency: Monthly

- Take-Home Pay: $8,000

- Four Walls Total: $4,000

- Lifestyle Total: $1,200

- Base Debt Snowball: $2,800

- Toggle: Activate Gazelle Intense

Process:

The calculator overrides the $1,200 lifestyle budget to absolute zero. It adds those funds directly to the $2,800 base snowball.

Result:

- Left to Assign: $0.00

- Debt Snowball Power: $4,000

Meaning:

Sacrificing comfort temporarily maximizes debt payoff speed. This family just found an extra $1,200 to attack their loans without needing a second job.

Can I afford a $1,500 apartment on $70,000 a year?

A single professional is evaluating a new lease against Dave Ramsey’s strict housing limits.

Use these inputs in the calculator:

- Pay Frequency: Monthly

- Take-Home Pay: $4,500 (approximate net for $70k gross)

- Housing Category: $1,500

- Other Four Walls: $1,200

- Lifestyle Total: $800

- Debt Snowball: $1,000

Process:

The system totals the $4,500 expenses and subtracts them from the $4,500 net income. It also isolates the housing ratio.

Result:

- Left to Assign: $0.00

- Warning: Housing is 33 percent of take-home pay.

Meaning:

While the budget balances to zero mathematically, the housing cost exceeds the recommended 25 percent limit. This person risks becoming house-poor despite having a balanced spreadsheet.

How do you fix a negative zero-based budget?

A user enters their standard spending habits and discovers a dangerous monthly deficit.

Use these inputs in the calculator:

- Pay Frequency: Monthly

- Take-Home Pay: $5,000

- Four Walls Total: $3,000

- Lifestyle Total: $1,500

- Debt Snowball: $800

Process:

The calculator subtracts the $5,300 total expenses from the $5,000 net income.

Result:

- Left to Assign: -$300.00

Meaning:

This budget relies on credit cards to survive. The user must lower lifestyle spending by $300 immediately to balance the math and avoid taking on new debt.

Quick Valuation Rules to Remember

Give every single dollar a name. Your income minus your outgo must always equal zero. If your result is positive, fund your debt snowball. If your result is negative, cut your lifestyle expenses. Enter your own numbers in the tool above to build your financial plan today.

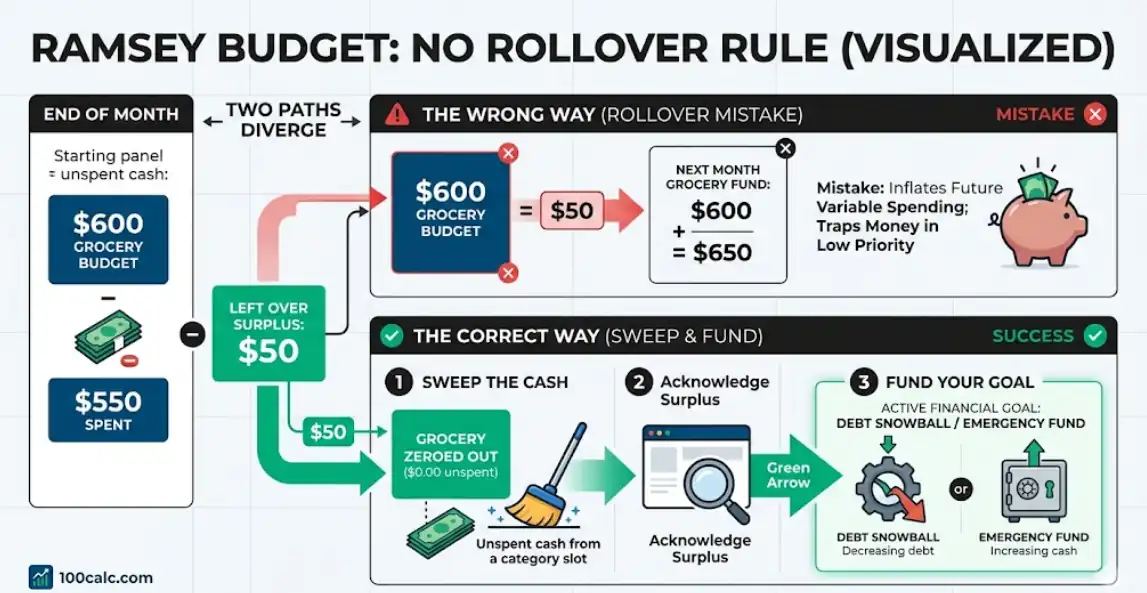

How to Handle Leftover Category Money (The Rollover Rule)

If you budget $600 for groceries but only spend $550 by the end of the month, you have a $50 surplus. Do not roll this over to inflate next month’s grocery fund.

- Close the Month: Acknowledge the $50 surplus in your lifestyle category.

- Sweep the Cash: Remove that $50 from your grocery allocation to zero it out.

- Fund Your Goal: Drop that $50 directly into your active Debt Snowball or Emergency Fund.

Simple rule to remember

Every new month starts fresh. Leftover cash should always fuel your current financial goal.

What Your Ramsey Budget Result Means by Range

Your “Left to Assign” number determines the health of your financial plan. A true zero-based budget requires perfect mathematical balance. Use this benchmark table to evaluate your calculator result and take immediate action to fix any hidden money leaks.

| Left to Assign | Status | Financial Meaning | Immediate Action | Ramsey Rule |

|---|---|---|---|---|

| Exactly $0 | Perfect | Every dollar has a specific job. | Follow your plan for the month. | The ultimate zero-based goal. |

| Positive (> $0) | Unassigned | Idle money is sitting in your account. | Move cash to your debt snowball. | Give every single dollar a name. |

| Negative (< $0) | Over Budget | You are spending more than you make. | Cut lifestyle expenses instantly. | Never rely on credit cards. |

Heads-up: A perfect zero does not mean your bank account is empty. It simply means zero dollars are left unassigned on paper.

Understanding Your Financial State

Hitting exactly zero means you successfully built a complete plan. Your income covers your basic needs and your wealth goals perfectly.

A negative result acts as a warning siren that you are overspending. You must fix this imbalance before the month starts. A positive result feels safe, but it actually means your budgeting job remains incomplete. Idle money vanishes easily on impulse purchases.

Pro Tip: The $300 Checking Account Buffer

A zero-based budget is a written mathematical plan, not your actual bank balance. Never drain your physical checking account to $0.00. Always keep a $100 to $300 cash buffer in your account to prevent accidental overdrafts from delayed transactions or auto-draft bills. The goal is to leave zero dollars unassigned on paper, not to empty your bank account.

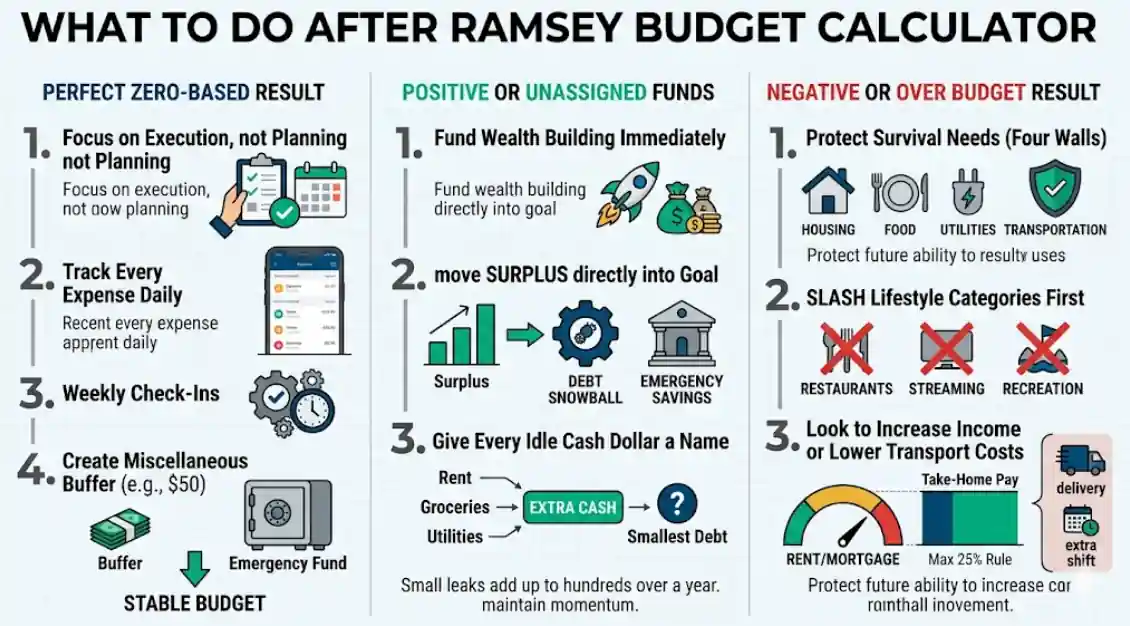

What to Do After Using the Ramsey Budget Calculator

Your result is only a plan until you take action. The next step is adjusting your spending to hit a perfect zero every single month. Use these insights to optimize your cash flow, protect your survival needs, and build wealth faster using the core Ramsey methodology.

For Perfect Zero-Based Results

Focus on execution rather than planning if your balance is exactly zero. Your primary job is tracking every expense daily to ensure reality matches your paper budget. Set up a weekly check-in to confirm you are staying within your chosen categories. This prevents small leaks from growing into month-end deficits. Create a small miscellaneous category to handle random one-off expenses. A fifty dollar buffer stops you from dipping into your emergency fund when small surprises happen. It keeps your overall budget balance stable throughout the entire month.

For Positive or Unassigned Funds

Fund your wealth building goals immediately when you have extra cash. Having unassigned money feels safe but actually makes you lazy with your spending habits. Move every dollar of that surplus directly into your current debt snowball or emergency savings. Giving that idle cash a specific name stops it from vanishing on impulse purchases. Users often leave small amounts unassigned thinking it does not matter. These small leaks add up to hundreds of dollars over a year. Assign that extra cash to your smallest debt immediately to maintain your financial momentum.

For Negative or Over Budget Results

Slash your lifestyle categories first to protect your survival needs. Never reduce your housing or food budget to fix a negative balance. Cut restaurants, streaming services, and recreation until the number hits zero. If you are still over budget, look for ways to increase income or lower transportation costs. Sticking to the twenty-five percent housing limit is crucial to avoid becoming house-poor during 2026 inflation spikes. Keep your rent or mortgage under one-quarter of your take-home pay. This protects your ability to save and invest for the future.

You Might Also Find These Helpful

Personal Finance 4

No tools published here yet.

Explore Related Tools

Common Errors When Using the Ramsey Budget Calculator

Small data entry errors can ruin your financial plan before the month even starts. Most people struggle with distinguishing between their total salary and actual take-home pay. These common mistakes often lead to a negative balance or unassigned cash sitting idle in your checking account.

- Entering your gross annual salary instead of your actual after-tax take-home pay.

- Leaving funds unassigned because you think zero-based means draining your bank account to zero.

- Forgetting to include irregular sinking funds like annual car registration or insurance premiums.

- Lumping basic grocery needs and weekend restaurant trips into a single spending category.

- Ignoring a negative result instead of slashing lifestyle expenses to reach a perfect zero.

Frequently Asked Questions (FAQs)

50/30/20 Budget vs. Zero-Based Budget: Which is better?

The 50/30/20 rule offers more wiggle room for lifestyle spending. However, the Dave Ramsey zero-based method provides superior accountability. It forces you to give every single dollar a specific job before the month starts. This level of detail is critical for anyone trying to escape debt quickly.

Is a $1,000 emergency fund enough in 2026?

Dave Ramsey still teaches that $1,000 is the standard for Baby Step 1. Many financial forums and modern budgeters now recommend $2,000 to cover today’s higher inflation. This larger starter fund better handles 2026 auto repair and utility costs while you aggressively attack your debt snowball.

What does Gazelle Intense mean?

Gazelle Intense describes a behavioral state of extreme focus on debt payoff. You cut all non-essential spending like restaurants and vacations to absolute zero. This allows you to funnel every spare cent into your smallest debt. The goal is to outrun debt like a gazelle runs from a cheetah.

Does zero-based budgeting mean my bank account goes to zero?

No. A zero-based budget means you have zero unassigned dollars on your written plan. You should always keep a cash buffer in your checking account to prevent overdrafts. The “zero” refers only to your mathematical plan. It ensures every dollar has a name before the month begins.

How do I handle a 3-paycheck month in my budget?

If you get paid bi-weekly, you will receive three paychecks during two months of the year. Your standard budget should rely on only two paychecks. Treat the third paycheck as a massive bonus. This allows you to make a huge leap forward in your current Baby Step.

How do I budget with irregular or commission income?

Budget using your lowest expected monthly income baseline. Cover your Four Walls first with this conservative number. If you earn more than expected, assign that surplus to your debt snowball or savings immediately. This strategy prevents you from overextending during low-income months.

What is the difference between a sinking fund and an emergency fund?

A sinking fund is for expected future costs like car tires or Christmas. You save a small amount for these items every month. An emergency fund is for true surprises like a job loss or medical bill. Zero-based budgets use both to prevent financial shocks.

Why Use This Over an Excel Budget Template or PDF?

Manually updating a Dave Ramsey budget worksheet PDF or Excel file is time-consuming and prone to formula errors. This free cloud-based calculator automates the zero-based math instantly. It automatically normalizes your bi-weekly income and routes your money to exactly $0 without requiring you to build complex spreadsheet formulas or pay for premium subscription apps.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.