Free Cost Basis Calculator: Stop Overpaying the IRS Now

Cost basis represents the exact tax-free capital inside your investment. Accurately tracking it proves your true net profit to the IRS. Our free cost basis calculator blends multiple stock purchases into one exact average cost. It also adjusts your real estate purchase price using capital improvements and claimed depreciation.

Millions of investors hand the government too much money every tax season. Many forget to include brokerage trading fees or reinvested dividends. This simple tracking error artificially inflates your taxable profit. You end up paying capital gains tax on money you already own.

Stop guessing your tax liability. Enter your investment data below to reveal your true shielded capital. Estimate your exact capital gains accurately before you decide to sell.

Quick Facts

- Best for: Retail investors, crypto traders, and homeowners.ss tracking.

- Key output: Total adjusted cost basis and estimated capital gains.

- Supported assets: Multi-lot equities, cryptocurrency, and real estate.

- Tax advantage: Factors in trading fees and dividend reinvestments automatically.

- Updated Jun 16, 2026

- Reviewed by 100Calc Research Team

Tax & Investment Tracker

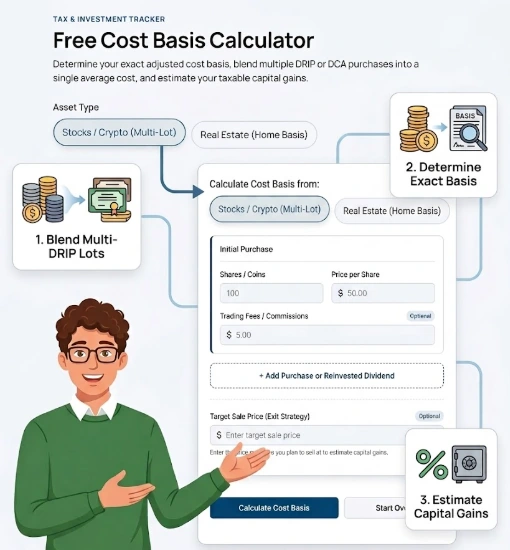

Free Cost Basis Calculator

Determine your exact adjusted cost basis, blend multiple DRIP or DCA purchases into a single average cost, and estimate your taxable capital gains.

Total Adjusted Cost Basis

Average Cost:

Cost Basis Composition

How do I calculate my cost basis?

How does IRS verify cost basis real estate?

How much capital gains tax will I pay on $300,000?

What happens if you don't have a cost basis for stock?

Explore More Calculators

Gross returns are a massive trap. Most investors ignore hidden fees and inflation. Uncover your exact net profit with our return on investment calculator.

Try calculatorHigh dividends often mask decaying stock prices. Use our expected capital gains yield calculator to isolate true growth and avoid risky value traps.

Try calculatorUse our free Stock Split Calculator to find your exact post-split share price, total holdings, and tax cost basis. Calculate fractional cash payouts instantly.

Try calculatorExplore Related Tools

Which Investment System Matches Your Asset?

Different investments require completely different math. A standard stock formula fails if you use it for a rental property with a mortgage. Crypto trades include hidden gas fees. Solar panels focus purely on breakeven timelines. Choose the correct calculator model below to get an accurate number.

| Mode | Category Label | Required Input Data | Tax Form Standard | Real-World Purpose |

|---|---|---|---|---|

| Stocks & ETFs | Equities | Share quantity, purchase price, and broker fees. | Requires Form 1099-B for IRS tracking. | Blends DRIPs and multi-lot purchases into one average cost. |

| Cryptocurrency | Digital Assets | Fractional coins, network gas fees, and dates. | Requires Form 1099-DA for digital assets. | Aggregates dollar-cost averaging (DCA) into a single baseline. |

| Real Estate | Property | Closing costs, renovations, and depreciation. | Requires Form 1099-S for property sales. | Finds your adjusted home basis by subtracting claimed wear and tear. |

Heads-up: Real estate mode automatically deducts claimed depreciation from your basis to meet strict property tax reporting laws.

What Your Adjusted Cost Basis Means

Your final output reveals the exact portion of your investment shielded from capital gains tax. A higher baseline means a lower IRS tax bill.

Understanding Your Result

This number represents the total tax-free money you have tied up in an asset. The IRS only taxes your profit above this exact figure.

If your total basis is $10,000, you owe zero taxes on the first $10,000 you get back during a sale. Accurately tracking every fee and reinvestment increases this protected amount.

Is Your Result Good or Bad?

A high cost basis relative to your current market value is excellent for tax purposes. It shrinks your taxable profit margin significantly.

Seeing a basis higher than your target sale price means you face a capital loss. You can use this loss legally to offset taxes on other successful investments. A very low basis means you face a massive tax hit upon selling.

What You Should Do Next

- Harvest your capital losses if your basis sits above the current market price.

- Wait at least 31 days before purchasing the same stock back to avoid the IRS wash sale penalty.

- Gather all receipts for real estate improvements to defend your numbers during an audit.

- Hold profitable assets for at least one year to secure cheaper long-term tax rates.

How to calculate you cost basis (Real-World Examples)

Let us see how the calculator works using real financial scenarios. These steps follow the exact logic required by major trading platforms and the IRS.

Input:

- Asset Type: Stocks / Crypto

- Lot 1 Shares: 50

- Lot 1 Price: $100.00

- Lot 1 Fees: $10.00

- Lot 2 Shares (DRIP): 10

- Lot 2 Price: $90.00

- Lot 2 Fees: $0.00

- Target Sale Price: $150.00

Expected Result:

Total Adjusted Cost Basis: $5,910.00

Average Cost: $98.50 per share

Total Shares: 60

Estimated Capital Gain: $3,090.00

Meaning:

The investor grew tYour exact breakeven point is $98.50 per share. Selling all 60 shares at $150 generates $9,000 in total cash. The IRS will only tax the $3,090 profit margin. Your original $5,910 basis remains entirely tax-free.

How to Use the Free Cost Basis Calculator

Our tool tracks complex financial transactions to determine your exact tax liability. It processes multiple purchase lots, fees, and real estate improvements automatically behind the scenes.

Select Your Asset Type

Choose the correct mode before entering any financial data. Pick the equities option to blend multiple stock or crypto purchases into one average cost. Switch to the property mode to calculate an adjusted home basis.

Log Your Original Purchase

Type in your starting share quantity and the original price paid. Property owners should enter their full initial home purchase amount. The system uses this baseline number as the foundation for all future tax adjustments.

Add Extra Value Inputs

Include any subsequent share purchases or reinvested dividends. Homeowners must input the total cash spent on major capital improvements. The calculator merges these new numbers with your original baseline to raise your protected equity.

Factor In Closing Costs and Fees

Input all allowable transaction expenses attached to your investments. This covers standard brokerage trading commissions or legal real estate closing costs. The math engine automatically adds these mandatory fees to lower your final taxable margin.

Check Estimated Capital Gains

Provide an optional target sale price for your asset. The logic subtracts your newly adjusted cost basis from this hypothetical exit value. You immediately see the exact profit margin exposed to the IRS.

What result should you expect when dollar-cost averaging into a mutual fund with trading fees?

This is a classic multi-lot example that helps you test the calculator’s average cost blending engine. It perfectly mirrors the real-world investments executed by retail investors on platforms that charge per-transaction fees.

Use these inputs in the calculator:

Asset Type: Stocks / Crypto

Lot 1: 50 shares at $100.00 with $10.00 fees

Lot 2: 25 shares at $90.00 with $5.00 fees

Lot 3 (DRIP): 5 shares at $95.00 with $0.00 fees

Target Sale Price: $120.00

Expected output:

Total Adjusted Cost Basis: $7,740.00

Average Cost: $96.75 per share

Total Shares Accumulated: 80

Estimated Capital Gain: $1,860.00

Status: VERIFIED

Expected interpretation:

The mathematical engine successfully aggregates all three purchases. It includes the zero-fee reinvestment lot and the $15 in total trading commissions. Your true breakeven point becomes exactly $96.75 per share. Selling all 80 shares at $120 generates $9,600 in total cash. The IRS will only tax the precise $1,860 profit margin.

Accuracy Behind the Cost Basis Engine

Basic financial calculators often ignore the strict nuances of tax law. Unlike a static cost basis calculator Excel template that requires constant manual updates, our live engine instantly blends multi-lot purchases and automatically adjusts for mandatory property depreciation. It directly mirrors official IRS Schedule D reporting logic, ensuring your final financial profile remains accurate and fully audit-ready.

Key Features & Benefits

- Aggregates multiple DCA crypto purchases into a single reliable average

- Adds mandatory closing costs to real estate baseline values accurately

- Deducts historical property depreciation to help prevent IRS audit flags

- Projects exact capital gains liabilities based on hypothetical exit prices

- Processes reinvested dividends cleanly to protect against unfair double taxation

Technical Process

Data Capture

The engine logs your initial capital, subsequent investments, and allowable trading fees securely.

Tax Adjustment

The system applies strict compliance rules by subtracting claimed depreciation for real estate assets.

Result Generation

The output displays your total adjusted basis and projects your future taxable capital gains.

How the Free Cost Basis Calculator Formula Works (Complete Breakdown)

The free cost basis calculator formula adds your total reinvested dividends, capital improvements, and allowable transaction fees to your original purchase price. For real estate, it also subtracts any claimed tax depreciation. This standard accounting math reveals the exact amount of tax-free money sitting inside your investment.

The Standard Equations

Stocks & Crypto Formula:

Total Adjusted Cost Basis = Base Capital + Added Capital + Total Fees

Average Cost Per Share = Total Adjusted Cost Basis / Total Shares

Capital Gain = (Total Shares × Target Sale Price) - Total Adjusted Cost Basis

Real Estate Formula:

Total Adjusted Cost Basis = Base Capital + Closing Costs + Capital Improvements - Depreciation Claimed

Capital Gain = Target Sale Price - Total Adjusted Cost Basis

What This Formula Does

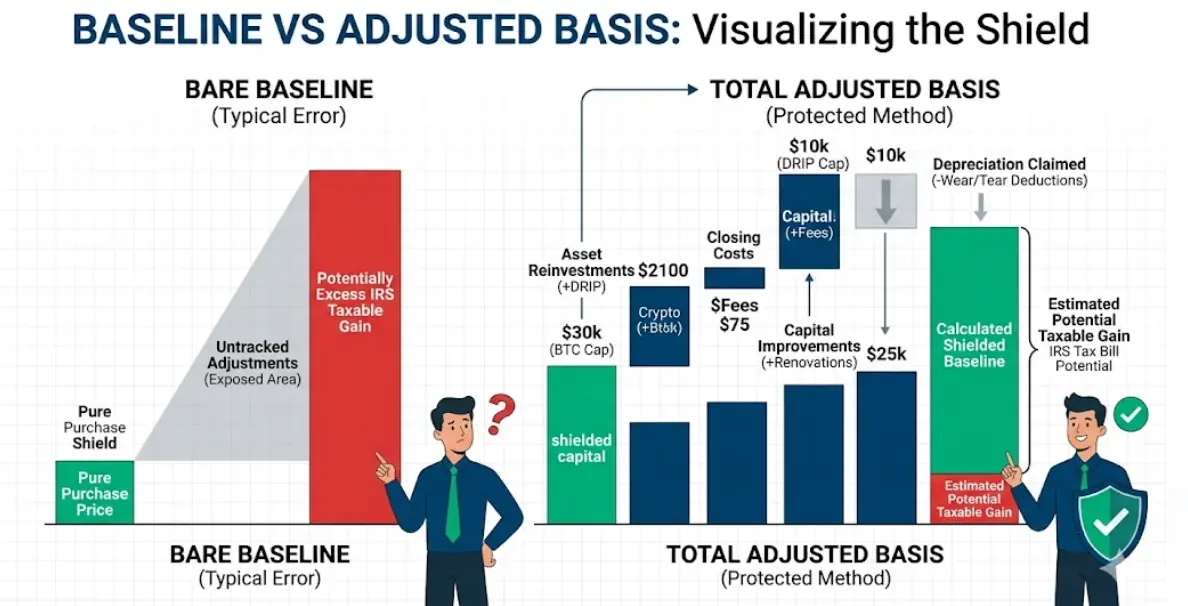

This math isolates the exact tax-free baseline of your investment. It ensures every legal IRS deduction is counted correctly. The system merges your initial purchase with all subsequent fees and DRIP reinvestments. It then subtracts that total from your exit price to show your true taxable profit margin.

Demystifying the IRS Variables

Every variable connects directly to the financial inputs you gathered from your brokerage or property records. Knowing what these terms mean helps you maximize your tax deductions safely.

Base Capital

This represents your raw starting point. For stocks, it equals your initial share quantity multiplied by your original purchase price. For property, it is the raw dollar amount you paid the previous owner.

Added Capital

This variable captures new value injected into the asset over time. It aggregates reinvested stock dividends (DRIPs) and extra fractional share purchases. For real estate, this field tracks the cost of major renovations that permanently increase the home’s value.

Total Fees

These are the unavoidable costs of executing a transaction. The IRS allows you to add brokerage trading commissions, load fees, and mandatory real estate closing costs to your baseline. This legally shrinks your taxable profit.

Depreciation Claimed

This variable applies strictly to rental properties. It tracks the yearly tax deductions you previously claimed for the physical wear and tear on the building. You must subtract this exact dollar amount from your baseline, which raises your final tax bill upon sale.

Another Example Calculation (Step-by-Step)

Let us see how the cost basis calculator works using a real scenario involving an Employee Stock Purchase Plan (ESPP). This helps you understand how to adjust your input price so you do not pay taxes on your company discount twice. The calculation follows the exact logic required by the IRS when your brokerage Form 1099-B shows an incorrect, unadjusted baseline.

Given:

- Total Shares Purchased = 100

- Discounted Price Paid = $42.50 per share

- Grant Date Fair Market Value = $50.00 per share

- Target Sale Price = $75.00

Calculation:

Discount Taxed on W-2 = $50.00 - $42.50 = $7.50 per share

Adjusted Purchase Price = Price Paid + W-2 Income = $50.00

Raw Capital Invested = 100 × $50.00 = $5,000.00

Total Sale Value = 100 × $75.00 = $7,500.00

Capital Gain = $7,500.00 - $5,000.00 = $2,500.00

The system requires your true, legally adjusted purchase price. Brokerages often report your $42.50 discounted price to the IRS automatically. You must manually calculate your adjusted $50.00 price and input that into the calculator to find your accurate tax exposure.

Result:

Adjusted Cost Basis: $5,000.00

Correct Price per Share: $50.00

Estimated Capital Gain: $2,500.00

Meaning:

Reporting your $42.50 discounted price as your baseline artificially inflates your taxable profit to $3,250. You already paid ordinary income tax on that $7.50 per share discount via your W-2 paycheck. By entering the adjusted $50.00 price into the calculator, your true baseline becomes $5,000. You legally shrink your capital gains exposure down to the correct $2,500 margin.

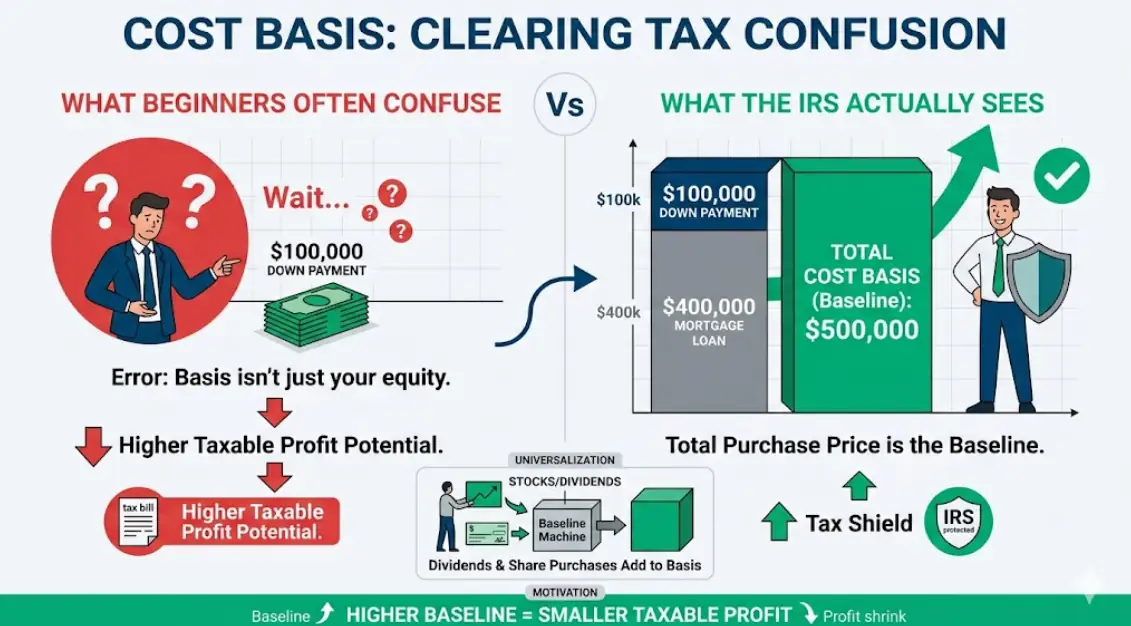

What is Cost Basis?

Cost basis is the total original value of an asset for tax purposes. It represents the money you already paid taxes on. The IRS uses this baseline number to figure out your exact profit or loss when you sell an investment.

Many beginners confuse cost basis with equity or cash out-of-pocket. If you buy a $500,000 house using a $100,000 down payment, your cost basis is still $500,000. Your mortgage loan does not lower your basis. The IRS only cares about the total purchase price plus allowable closing costs.

The Stepped-Up Basis Loophole

Inherited assets follow a completely different tax rule called a stepped-up basis. If you inherit property or stocks, your new baseline becomes the fair market value of the asset on the exact day the original owner passed away. You do not use their historical purchase price. This legal rule often shields families from massive capital gains taxes.

Why this matters

A higher baseline always shrinks your taxable profit. Tracking your exact cost basis ensures you never pay capital gains tax on money that legally belongs to you.

How do you calculate your cost basis?

Calculate your baseline by adding your original purchase price to all related transaction fees. For stocks, add reinvested dividends and extra share purchases. For real estate, include closing costs and major capital improvements, then subtract any claimed depreciation. Compare this total against your final sale price.

How do you calculate cost basis for crypto dollar-cost averaging?

A crypto investor buys Bitcoin across multiple months using an exchange that charges high trading fees.

Use these inputs in the calculator:

- Asset Type: Stocks / Crypto

- Lot 1: 0.50 coins at $60,000 with $50 fees

- Lot 2: 0.25 coins at $50,000 with $25 fees

- Target Sale Price: $70,000

Process:

Lot 1 capital is $30,000. Lot 2 capital is $12,500. Total fees equal $75. The calculator adds these values to find the exact tax-free baseline for the accumulated 0.75 BTC.

Result:

- Total Adjusted Cost Basis: $42,575.00

- Average Cost: $56,766.67 per coin

- Estimated Capital Gain: $9,925.00

Meaning:

The true breakeven price is $56,766.67 per coin. Selling the entire 0.75 BTC stash for $70,000 generates $52,500 in total cash. The IRS only taxes the $9,925 profit margin.

What is the average cost basis for stocks with dividend reinvestment?

A retail investor buys an index fund and lets dividends automatically purchase new fractional shares over time.

Use these inputs in the calculator:

- Asset Type: Stocks / Crypto

- Lot 1: 100 shares at $400.00 with $0 fees

- Lot 2 (DRIP): 5 shares at $420.00 with $0 fees

- Target Sale Price: $450.00

Process:

The initial $40,000 investment merges with the $2,100 generated from reinvested dividends. The system divides the new $42,100 total by the 105 accumulated shares.

Result:

- Total Adjusted Cost Basis: $42,100.00

- Average Cost: $400.95 per share

- Estimated Capital Gain: $5,150.00

Meaning:

Tracking reinvested dividends raises your baseline significantly. This tracking prevents you from paying capital gains taxes on dividend money already taxed as income.

How does depreciation affect a rental property cost basis?

A landlord prepares to sell a rental property after owning it for a decade and claiming yearly wear and tear deductions.

Use these inputs in the calculator:

- Asset Type: Real Estate

Purchase Price: $350,000 - Closing Costs & Fees: $7,500

- Capital Improvements: $25,000

- Depreciation Claimed: $10,000

- Target Sale Price: $450,000

Process:

The calculator adds the $7,500 closing costs and $25,000 in major renovations to the original price. It then legally subtracts the $10,000 in claimed depreciation.

Result:

- Total Adjusted Cost Basis: $372,500.00

- Estimated Capital Gain: $77,500.00

Meaning:

Claiming depreciation over the years legally lowered the baseline. Selling the property for $450,000 exposes $77,500 to potential capital gains tax and depreciation recapture rules.

Quick rule to remember

Always document your mandatory trading fees and real estate closing costs. Tracking every small reinvestment raises your baseline over time. You can enter your own numbers into the calculator above to see your exact shielded capital.

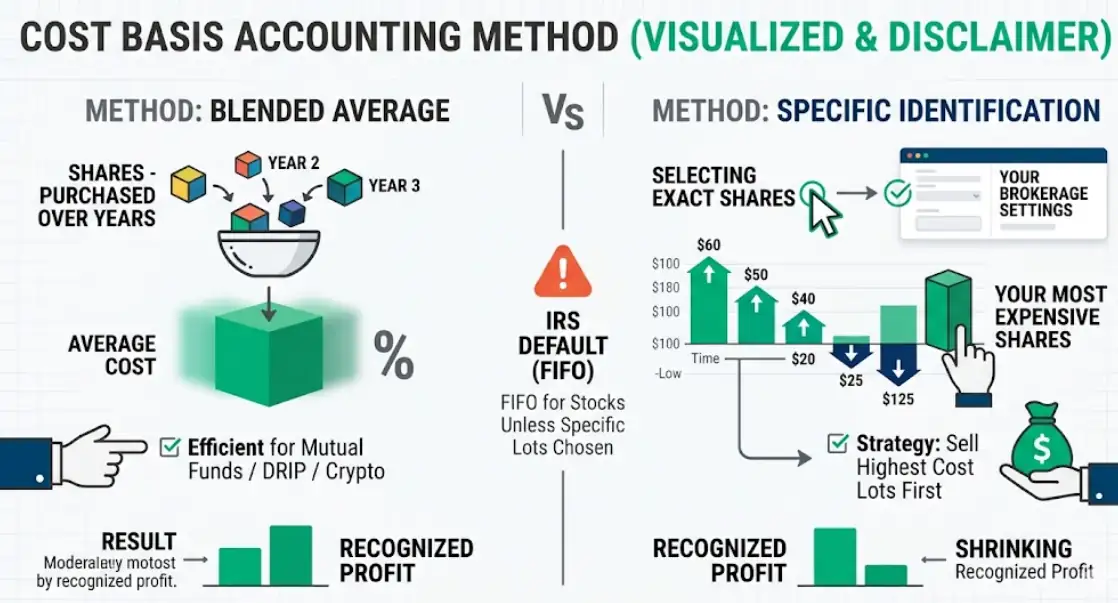

Understanding Your Accounting Method (Disclaimer)

Our tool natively computes the Average Cost method. This is highly efficient for tracking mutual funds, dividend reinvestments, and crypto dollar-cost averaging.

However, be aware that the IRS usually defaults to First-In, First-Out (FIFO) for individual stock sales unless you instruct your broker otherwise. If you use Specific Identification to choose exactly which tax lots to sell, your final taxable margin will differ from a blended average. Always verify your chosen accounting method with your brokerage before filing taxes.

What this means for your decision

Your chosen accounting method dictates exactly which shares you are officially selling. If you bought assets at various price points over several years, switching from a blended average to Specific Identification might allow you to sell your most expensive shares first. This legal strategy shrinks your recognized profit. Always check your brokerage settings to lock in the most tax-efficient method before executing a major portfolio sale.

Cost Basis Calculator Result Benchmarks

Your final profit margin dictates how the government taxes your investment. Tracking your exact gain or loss percentage helps you plan a smarter exit strategy. Review the financial benchmarks below to evaluate your current tax exposure and protect your wealth.

| Gain / Loss Margin | Category | USA Tax Rule | India Tax Rule | Investor Strategy |

|---|---|---|---|---|

| > 20% Profit | High Gain | Hold >1 year for lower LTCG rates (0-20%). | Hold >1 year for lower LTCG rates (12.5%). | Avoid selling early to prevent massive tax hits. |

| 0% to 19% Profit | Moderate Gain | Taxed up to 37% if held under one year. | Taxed at 20% if sold as short-term gain. | Offset these gains with other portfolio losses. |

| Below 0% (Loss) | Capital Loss | Deduct up to $3,000 against ordinary income. | Carry forward capital losses for up to 8 years. | Harvest these losses to shield other profits. |

Heads-up: Tax rules change based on your personal income bracket. Always consult a certified CPA before making major portfolio sales.

Interpretation

A negative result provides a valuable tax shield. You can use capital losses to offset taxes owed on winning investments. Moderate gains represent standard market growth with manageable tax bills. High gains require careful timing. Selling a highly profitable asset too early triggers expensive short-term tax penalties.

Pro Tip

Always wait at least 366 days before selling a profitable asset. This simple delay switches your tax burden from expensive short-term rates to much cheaper long-term capital gains brackets.

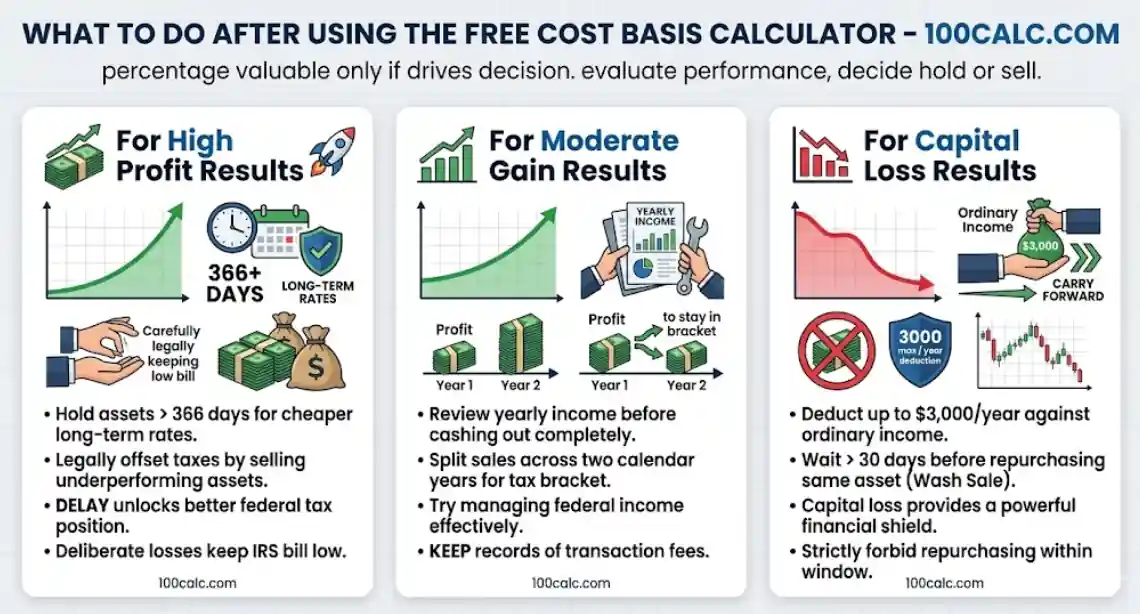

What to Do After Using the Free Cost Basis Calculator

Your calculated result dictates your immediate tax strategy. Knowing your true profit margin helps you decide exactly when to sell an asset. The following steps show you how to protect your money based on the specific gain or loss range you just calculated.

For High Profit Results

Seeing a massive gain means you face a heavy tax burden. You should hold volatile assets for at least 366 days before selling. This delay automatically unlocks much cheaper long-term capital gains rates.

Consider selling other underperforming assets in your portfolio at the exact same time. You can use those deliberate losses to legally offset the taxes owed on this high-performing investment. This strategy keeps your overall IRS bill low.

For Moderate Gain Results

A moderate gain gives you more flexibility to sell without triggering a massive penalty. Review your current yearly income before cashing out completely.

Selling too many profitable assets at once might push you into a higher federal tax bracket. Try splitting your sales across two different calendar years to manage your total taxable income effectively. Always keep strict records of the transaction fees that helped lower this final margin.

For Capital Loss Results

A negative result provides a powerful financial shield. You can deduct up to $3,000 of these capital losses against your ordinary working income each year. Any remaining loss carries forward into future tax seasons automatically.

Be very careful about buying the same stock back too quickly. The IRS wash sale rule strictly forbids claiming a loss if you repurchase the exact same asset within thirty days. Wait until that window fully closes before re-entering your market position.

You Might Also Find These Helpful

Investment 3

No tools published here yet.

Related Tools People Use Next

Common Mistakes When Using the Cost Basis Calculator

A small data entry error can drastically change your taxable profit margin. Many investors accidentally skip mandatory tax adjustments or misunderstand IRS rules regarding property upgrades. Review the list below to ensure your final calculation accurately reflects your true financial liability.

- Forgetting to add brokerage trading commissions and exchange fees to your original purchase price.

- Confusing standard property repairs with permanent capital improvements that legally raise your baseline.

- Failing to track reinvested stock dividends which forces you to pay taxes on them twice.

- Ignoring previously claimed depreciation on rental properties when calculating your final adjusted sale value.

- Assuming the IRS or your current broker will automatically find your missing historical purchase data.

Frequently Asked Questions (FAQs)

How do I find the cost basis for RSUs or ESPP shares?

Your employer usually reports the vested value as ordinary income on your W-2. You must manually add this already-taxed amount to the baseline shown on your 1099-B. Forgetting this adjustment means you will pay taxes on that exact same money twice.

Are reinvested dividends included in my total cost basis?

Yes. You already pay income taxes on stock dividends during the year they are issued. Adding these reinvested amounts to your baseline ensures you do not pay capital gains tax on them again when you finally sell your shares.

What is the cost basis for inherited stocks or property?

Inherited assets receive a step-up in basis. Your new baseline is the fair market value of the asset on the exact date the original owner passed away. You do not use their historical purchase price. This legal rule often eliminates massive tax burdens instantly.

How do I fix an incorrect cost basis on my 1099-B?

Brokerages often report missing baselines for transferred accounts or old employee stock plans. You must file IRS Form 8949 alongside Schedule D to manually adjust the reported number to the correct amount. Keep your historical pricing statements securely as proof.

Does the primary home sale exclusion change my cost basis?

No. The IRS allows someone to exclude up to $250,000 of asset gain on a primary residence. This exclusion shields your final profit from taxes. However, it does not mathematically alter the original adjusted cost basis of the property itself.

Can I estimate my basis if my purchase records are lost?

Yes. The IRS permits a good-faith estimate using historical pricing data if your original statements are destroyed. You must document exactly how you reverse-engineered the price. If you get audited, the IRS may reject your math and assume a zero-dollar baseline.

Can I switch from average cost to FIFO for mutual funds?

Generally, no. Once you sell shares of a mutual fund using the average cost method, the IRS locks you into that accounting style for those specific shares. You cannot suddenly switch to First-In, First-Out later just to lower your tax liability.

Do property taxes and insurance count toward real estate basis?

No. The IRS classifies yearly property taxes, home insurance premiums, and standard maintenance as personal expenses. Only major capital improvements permanently extend the lifespan of the home. Examples include adding a new roof or building an extension. Only these upgrades increase your cost basis.

Do cryptocurrency network gas fees increase my total basis?

Yes. Any network transaction fees or exchange commissions paid specifically to buy a digital asset are allowable acquisition costs. Adding these mandatory expenses directly to your initial purchase price mathematically lowers your final taxable profit when you trade the coin.

How does a stock split affect my cost basis?

A stock split lowers your price per share but keeps your total investment value exactly the same. You just divide your original purchase amount by your new share count. This mathematical adjustment ensures your overall tax liability does not increase.

Does a wash sale change my cost basis?

Yes. Buying the exact same stock within thirty days of selling it at a loss triggers the wash sale rule. The IRS forbids claiming the immediate tax deduction. Instead, you must add that disallowed loss directly to your new purchase price.

This legal adjustment raises your total baseline. It delays your tax benefit until you finally sell the new shares permanently.

What is the cost basis of a gifted asset?

Gifted assets usually keep the original owner’s purchase price. If a family member bought shares for $500 and gives them to you, your starting baseline remains $500. Selling the asset means you will owe taxes on all profits generated since that initial purchase.

Why is my cost basis missing after changing brokers?

Transferring accounts between different brokerages often causes historical purchase data to drop off. Financial institutions have up to fifteen days to send the proper tax lots over the ACATS network. You must manually enter your original purchase data into a calculator if the transfer fails.

Does moving crypto between wallets trigger a taxable event?

Transferring digital assets between your own personal wallets does not create a taxable event. Your original purchase price remains completely unchanged. You only report capital gains when you sell the coin for fiat cash or trade it for another cryptocurrency.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.