Maximum Allowable Offer Calculator: Stop Letting 2026 Holding Costs Kill Your Flips

A maximum allowable offer calculator determines the absolute highest price you can pay for an investment property. It subtracts your total repair budget, fixed closing fees, and monthly holding costs from the after repair value. This provides a strict financial ceiling to secure your true profit margin.

Many house flippers are actively losing money in the current market. High hard money interest rates mean every unsold month aggressively drains your equity. A minor contractor delay can easily cost you thousands in extra loan payments. Relying on a simple blind guess practically guarantees a financial loss.

You need a reliable number before signing any contract. This tool calculates your exact strike price based on real project timelines. Enter your estimated repair costs and wholesale assignment fees below. The system immediately reveals the maximum amount you should offer the seller today.

Quick Facts

- The 70% Rule Base: Reserves a strict 30% margin to cover your gross profit and expensive closing fees.

- Holding Cost Guard: Actively reduces your offer price to absorb high 2026 bridge loan interest.

- Wholesale Buffer: Protects your assignment fee while keeping the contract highly attractive to end buyers.

- Underwater Alerts: Signals instantly when high repair budgets make a property too risky to purchase.

- Updated Jun 17, 2026

- Reviewed by 100Calc Research Team

Real Estate Deal Analyzer

Maximum Allowable Offer Calculator

Instantly calculate your strict MAP (Maximum Allowable Price) to protect your profit margins. Whether you need a standard 70 percent rule flipping calculator or a dynamic wholesale calculator app, this engine factors in holding times, fixed costs, and smart repair estimates.

Maximum Allowable Offer (MAO)

Projected Flipper Profit:

The Deal Breakdown (ARV)

What is the maximum allowable offer formula?

How does the AI repair cost and MAO calculator work?

Can I use this instead of a MAP calculator excel sheet?

How to use a wholesale calculator app or MAO tool?

Explore More Calculators

Use our Car Trade-In Tax Savings Calculator to uncover your exact discount instantly. Stop losing money to hidden showroom math and beat private sales.

Try calculatorBuying a family home? Calculate your exact gift of equity to bypass PMI instantly. See your new mortgage payment, tax limits, and get a…

Try calculatorNominal gains lie. Use our real estate appreciation calculator to track compound growth, subtract inflation, and reveal your true property equity.

Try calculatorExplore Related Tools

What Your Maximum Allowable Offer Means

Your result represents the absolute financial limit for a property purchase. This number acts as a shield for your business capital. It covers your intended profit while leaving room for all project expenses. Think of it as your final “walk away” price.

Understanding Your Result

This number shows the exact contract price required to hit your target profit. Many investors assume the gap left by the 70% rule is pure cash profit. That is a dangerous mistake. This 30% margin must absorb your buying costs, selling costs, and agent commissions. It also pays for your monthly loan interest while the house sits empty.

The calculator output tells you where negotiations must end. If a seller asks for more than this result, you are actively losing money. Sticking to this number ensures you stay profitable despite the current high interest rates in 2026.

Is Your Result Good or Bad?

Context depends on your local market competition. An MAO based on the 70% rule is considered an optimal deal. It provides a massive safety net to absorb repair delays or market shifts. You should feel very confident making this offer.

If your calculated limit feels too low to win bids, you are likely in a hyper-competitive market. Some investors push to the 75% or 80% rule in hot areas. This is risky. Any MAO that results in a negative number means the project is “underwater.” Those deals are fundamentally broken and should be avoided entirely.

What You Should Do Next

Compare your result to the seller’s asking price immediately. Use this specific number to ground your negotiations in hard data rather than emotion. If the numbers do not align, do not be afraid to walk away.

Audit your repair estimates if the deal looks too tight. High 2026 material costs can easily ruin a budget. If you are wholesaling, check your assignment fee. A fee that is too high might kill the deal for your end buyer. Always prioritize your equity safety over closing a bad contract.

A Quick Example to Test

Imagine you find a distressed rental property with a $250,000 ARV. You want to use the standard 70% safety rule. Use these inputs to see how the numbers break down.

Input:

- ARV: $250,000

- Rule: 70%

- Repairs: $30,000

- Fixed Fees: $5,000

- Holding Costs: $800 per month for 5 months ($4,000 total)

Result:

Your MAO is $136,000.

Meaning:

You must secure the contract at $136,000 to protect your equity. This offer allows you to spend $30k on rehab and $9k on carrying costs while still hitting your profit goal. If the seller demands $150,000, you are sacrificing $14,000 of your own profit before the work even starts.

Micro Insight:

Lenders and hard money providers want to see strict offer discipline. Following your MAO builds long-term trust and makes it significantly easier to secure fast funding for future projects.

What is the maximum allowable offer?

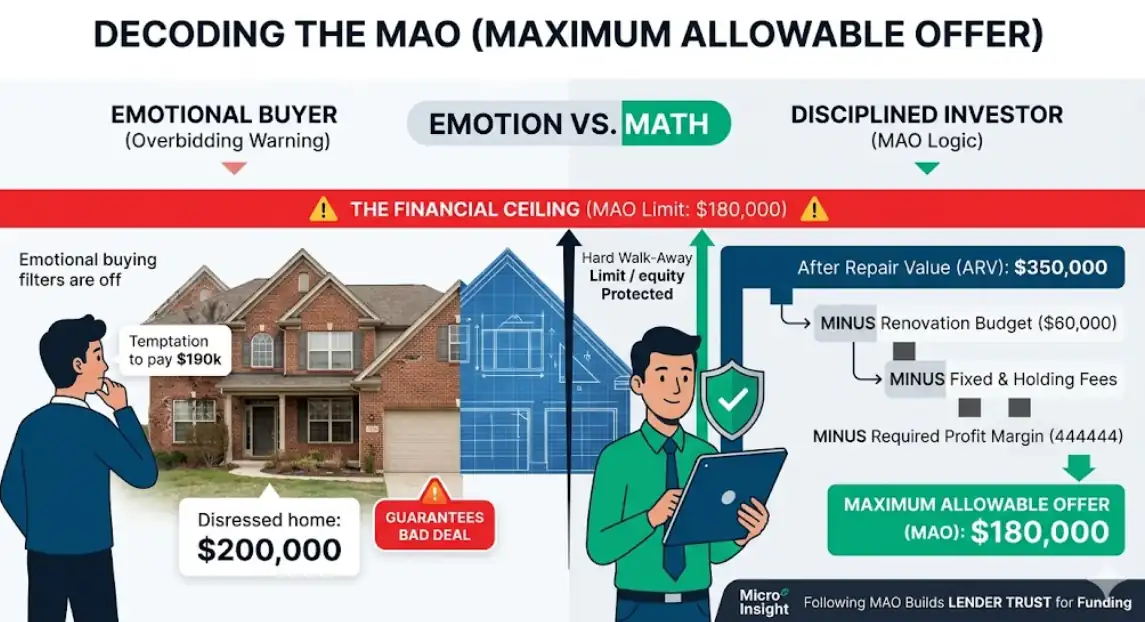

The maximum allowable offer (MAO) is the absolute highest price an investor can pay for an investment property while maintaining their target profit margin. It acts as a strict financial ceiling, calculated by subtracting repair costs, fixed fees, and holding costs from the After Repair Value. This limit accounts for the future sale price, repair budgets, and required profit margins. Paying anything above this number guarantees a bad deal.

Investors use this concept to filter out emotional buying. It transforms a house from a physical building into a pure math equation. By setting this limit early, you remove the temptation to overbid during a bidding war. You stop looking at the beautiful brick exterior and start seeing the actual financial risk.

Think of it as a safety net for your business capital. Real estate markets can shift quickly. A strict MAO ensures that even if your project takes longer than expected, your initial equity remains protected. It provides the firm “walk-away” number required for successful flipping or wholesaling.

Imagine you find a distressed suburban home listed for $200,000. Your math shows it could sell for $350,000 after a $60,000 renovation. If your calculated MAO is $180,000, that is your hard limit. Even if the seller is friendly, you cannot pay $190,000. Sticking to this number ensures your profit margin survives the project.

Which Equity Rule Should You Use for Your Market?

The 70 percent rule is the classic safety net, but shifting 2026 market conditions—like tight inventory and institutional buying—force investors to adapt. High-demand areas push buyers to accept tighter margins, while distressed markets require deeper discounts. Choose your rule limit based on local competition and your renovation speed.

| Rule Limit | Label | USA Guideline | Global/Hot Market | Notes |

|---|---|---|---|---|

| 70% or Below | Conservative | Standard for rural and slower suburban flips. | Ideal for beginner investors in most countries. | Highest safety margin for unexpected rehab costs. |

| 75% | Competitive | Common in growing metro areas with high demand. | Standard for high-growth cities in UK and Canada. | Requires an efficient crew to protect thin margins. |

| 80% or Above | Institutional | Used by large funds in hyper-hot coastal cities. | Found in central London or luxury turnkey markets. | Extremely high risk; often used for long-term rentals. |

Heads-up: Most 2026 bridge loan lenders require at least a 20% equity cushion to approve your project funding.

Note:

Choosing a higher percentage increases your winning bids but completely destroys your margin for unexpected repair errors. If you are new to the local market, stick to the 70 percent rule until you master your renovation budgets.

How to Use the Maximum Allowable Offer Calculator

This MAO calculator breaks down a complex real estate deal into a simple equation. It calculates exactly what you can pay by subtracting your costs from your expected sale price. Follow these steps to find your final contract price.

Set ARV and Strategy

Enter your target after repair value first. This number represents the final retail price of the renovated home. You must also select your investment mode. Choose the flipper option or pick the wholesaler mode to include an assignment fee.

Choose Your Limit

Adjust the percentage slider to reserve your gross equity. The standard safety margin sits at 70 percent. Highly competitive markets might require pushing this limit higher. This setting protects your baseline profit before any construction work begins.

Estimate Repairs

Input your total expected rehab budget directly into the field. You can also open the smart estimator tool. This feature calculates a baseline repair cost using the property square footage. It helps prevent you from underestimating your construction needs.

Add Hidden Costs

Enter your fixed closing fees and agent commissions next. Then add your monthly carrying costs like hard money interest and utilities. The calculator uses your estimated project timeline to multiply these monthly expenses. This reveals your true financial burden.

Review the Maximum Allowable Offer

Check your exact contract strike price at the bottom. The system instantly reveals the absolute highest amount you can pay the seller. It also projects the total cash needed to close the deal. Use this number to negotiate safely.

How do you calculate a tight margin flip?

Read the local market data to establish your ARV. To find your strike price in a hot market, adjust your rule limit to 75 percent. Then subtract your total repair and holding costs. This is where many new investors miscalculate.

This classic flip scenario tracks a high-demand property. Buyers often struggle with pricing because they ignore monthly bridge loan costs.

Use these inputs in the calculator:

- ARV: $350,000 Rule

- Limit: 75% Repairs: $45,000

- Fixed Fees: $12,000

- Holding Costs: $1,200 per month for 3 months

Process:

The formula multiplies the ARV by the 75 percent limit. It then subtracts the $60,600 in total deductions.

Final Result:

Your Maximum Allowable Offer is $201,900

Meaning:

You must secure the property for $201,900 or less. This protects your required margin while covering three months of expensive carrying costs.

Accuracy Behind the Real Estate Deal Analyzer

Basic spreadsheets often ignore the time value of money. This engine factors in the exact months you hold the property. It prevents you from overpaying by actively deducting monthly hard money interest before delivering the final offer price. You get real-time logic instead of outdated Excel formulas.

Key Features & Benefits

- Subtracts monthly expenses based on your exact project timeline

- Calculates instant baseline repair budgets using local square footage rates

- Automatically reserves the end buyer's profit and your assignment fee

- Shows exactly where the ARV equity goes via a dynamic chart

- Warns you instantly if a deal becomes financially underwater or too tight

Technical Process

Equity Locking

Isolates your gross profit buffer using the ARV and rule percentage.

Cost Scrubbing

Subtracts all repairs, fixed fees, and timeline-based carrying costs.

Strike Calculation

Delivers a strict contract price ensuring you never overpay for equity.

How the Maximum Allowable Offer Formula Works (Complete Breakdown)

The maximum allowable offer formula is the mathematical shield investors use to protect their profit. It calculates your highest safe bid by multiplying your ARV by the 70 percent rule. The system then subtracts all repairs and carrying costs to guarantee you never overpay for a property.

The Core MAO Calculator Equation

This formula uses standard real estate subtraction to isolate your profit margin. It takes your gross equity limit and removes every projected expense to reveal your exact strike price.

Formula:

Cash Buyer MAO = (ARV * Rule%) - (Repairs + Fixed Costs + [Monthly Holding * Holding Time])

Wholesale MAO = Cash Buyer MAO - Assignment Fee

This mathematical equation prevents emotional buying. By locking in a strict percentage of the after repair value, the formula creates a reliable gross profit margin. It then actively deducts your construction bids, agent fees, and monthly loan interest. The final number is the absolute maximum cash you can safely spend.

Understanding Your Deal Variables

Each value below connects directly to your calculator inputs. These numbers represent the real-world costs used to protect your business capital.

After Repair Value (ARV)

This means the estimated market value of the property after all renovations. Recent 2026 market data requires pulling comps from the last 90 days to avoid dangerous overestimation.

Rule Percentage (Rule%)

This fraction of the ARV protects your equity. Current investor forums suggest standard markets use 70 percent. Highly competitive markets might push this to 75 percent, but you must execute the rehab flawlessly.

Total Repairs

This is the exact dollar amount required to fix the property. It must include materials, labor, and a strict contingency buffer. Many experienced flippers add a 5 percent fudge factor here for unexpected structural issues.

Fixed Costs

These are one-time expenses that remain constant regardless of your timeline. They include buying closing costs, selling fees, and agent commissions. They usually account for 4 to 6 percent of the total project cost.

Monthly Holding

These cover high-interest bridge loans, taxes, and utilities paid every 30 days. Elevated 2026 interest rates make holding costs the primary reason flips fail. This time-based variable actively reduces your offer price.

Assignment Fee

This represents the specific profit a wholesaler takes for finding the deal. Subtracting this from the cash buyer maximum offer ensures the end investor still hits their target margin.

Another Example Calculation (Step-by-Step)

Let’s see how the formula works using a real fix and flip scenario. This helps you understand how monthly loan interest aggressively reduces your final contract price. The calculation follows strict investment standards.

Given:

- Total ARV: $400,000

- Rule Limit: 70%

- Repairs: $45,000

- Fixed Costs: $12,000

- Monthly Holding: $1,500

- Holding Time: 5 Months

Calculation:

(400,000 * 0.70) - (45,000 + 12,000 + [1,500 * 5]) = 215,500

Your gross equity limit is $280,000. Subtracting your $45,000 in repairs, $12,000 in fixed closing costs, and $7,500 in total holding costs leaves $215,500.

Result:

- Target Strike Price: $215,500

- Total Deductions: $64,500

Meaning:

You must lock the contract at $215,500 to secure your expected profit. If the project gets delayed by two extra months, your holding costs increase by $3,000. Your true maximum allowable offer would drop instantly to $212,500.

How do you calculate the maximum allowable offer?

Calculate your maximum allowable offer by multiplying the home’s after repair value by your chosen equity limit. Subtract your total repair costs, fixed closing fees, and monthly carrying expenses from that number. The final result reveals the highest safe price you can pay for the property.

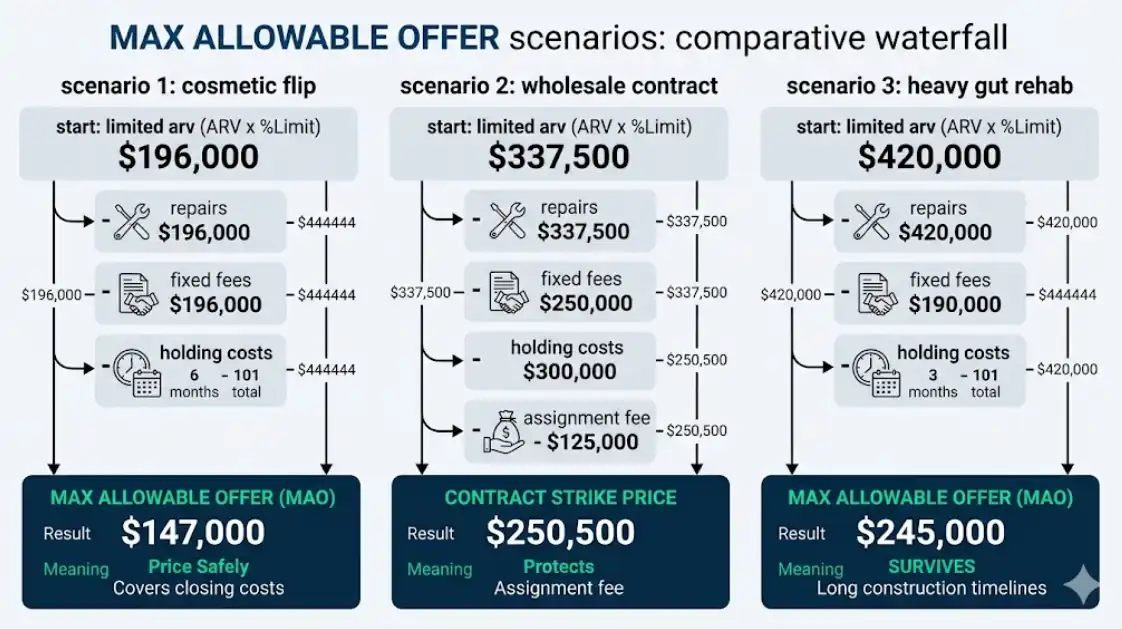

What is the MAO for a standard cosmetic flip?

A real estate investor finds a dated house needing basic cosmetic updates to sell fast.

Use these inputs in the calculator:

- ARV: $280,000

- Rule Limit: 70%

- Repairs: $35,000

- Fixed Fees: $10,000

- Holding Costs: $1,000 per month for 4 months ($4,000 total)

Process:

Multiply $280,000 by 0.70 to get $196,000. Subtract $49,000 in total deductions to find the strict price limit.

Result:

Your Maximum Allowable Offer is $147,000.

Meaning:

The investor must buy the house for $147,000 or less. This price safely covers all closing costs and secures the required profit margin.

How do you calculate an offer for a wholesale contract?

A wholesaler locates a distressed property in a hot neighborhood where cash buyers accept tighter 75 percent margins.

Use these inputs in the calculator:

- ARV: $450,000

- Rule Limit: 75%

- Repairs: $50,000

- Fixed Fees: $15,000

- Holding Costs: $2,000 per month for 5 months ($10,000 total)

- Assignment Fee: $12,000

Process:

Multiply $450,000 by 0.75 to reach $337,500. Subtract $75,000 in project costs to find the buyer’s limit of $262,500. Deduct the $12,000 assignment fee.

Result:

Your Contract Strike Price is $250,500.

Meaning:

The wholesaler needs to lock the seller contract at $250,500. This protects their assignment fee while leaving enough equity to keep the end buyer happy.

What is the maximum offer for a heavy gut rehab project?

A contractor plans to completely rebuild an abandoned house. This requires a much longer construction timeline and expensive bridge loans.

Use these inputs in the calculator:

- ARV: $600,000

- Rule Limit: 70%

- Repairs: $120,000

- Fixed Fees: $25,000

- Holding Costs: $3,000 per month for 10 months ($30,000 total)

Process:

Find 70 percent of $600,000, which equals $420,000. Subtract all hard expenses totaling $175,000 from that starting capital.

Result:

Your Maximum Allowable Offer is $245,000.

Meaning:

Long timelines destroy equity. The buyer must demand a massive discount upfront to survive ten months of expensive hard money interest and high repair bills.

Quick rule to remember

Look closely at your holding timeline and fixed fees before making an offer. Those hidden numbers often ruin great deals for new investors. Once you verify local property values, enter your own numbers into the calculator to find your exact strike price.

Maximum Allowable Offer Result Benchmarks Explained

Your calculated offer depends heavily on your chosen rule percentage. This equity limit defines your exact financial safety net. Different real estate markets demand different risk tolerances to win contracts. Review these benchmarks to evaluate your deal’s safety before submitting any offer.

| Range | Label | USA Standard Markets | USA Hot Markets | Notes |

|---|---|---|---|---|

| Below 70% | Deep Discount | Found mostly in distressed or rural areas. | Virtually nonexistent on public listings. | Massive equity build. Guarantees high profit. |

| 70–74% | Optimal Deal | The proven safety standard for most US cities. | Hard to secure without direct marketing. | High safety margin. Protects against rehab delays. |

| 75–80% | Tight Margin | Too risky for average fix and flip projects. | Frequently required to win competitive bids. | High risk. You must control timelines perfectly. |

Heads-up: Market conditions dictate your limit. Always confirm local sold comps before locking in a high-risk margin.

Interpretation

Maintaining a 70 percent limit is the safest goal for most investors. This buffer absorbs unexpected repair costs and expensive bridge loan interest. Pushing your limit toward 80 percent removes that safety net completely. One minor plumbing issue or contractor delay can push your entire project underwater. Consistent discipline keeps your business profitable.

Pro Tip:

Never increase your equity limit just to win a bidding war. Walking away from a bad deal is always better than trapping your cash in an unprofitable house.

What to Do After Using the Maximum Allowable Offer Calculator

Your result is only a number until you use it to negotiate. The next step involves comparing your offer limit against the seller’s asking price. Most investors fail because they ignore time-based carrying costs. Use these insights to protect your equity and win better deals in the current market.

For Optimal Low Risk Deals

Move toward a contract immediately when your offer falls in this safe range. You have a massive safety net that protects against unexpected plumbing or structural discoveries. Veteran investors still add a 15% contingency to the rehab budget to stay safe. Secure the property before a competitor offers a slightly higher price in this comfortable profit zone.

Verify your renovation plan before signing the final papers. A safe margin allows you to use higher-quality finishes that attract better buyers. This rule limit ensures your profit survives even if the project takes two months longer than expected. Speed is still helpful but you are not fighting for survival in this category.

For Tight Margin High Risk Deals

Control your contractor schedule with absolute precision to survive these thin margins. High 2026 interest rates make every extra week of holding time a direct hit to your profit. Negotiate harder with the seller or look for ways to reduce the renovation scope without hurting the final value. Avoid these deals unless you have a proven team that can finish the work under budget.

Review your fixed closing costs and agent commissions one more time. Small errors in your fee estimates will quickly push a tight deal into a financial loss. You should consider asking for seller concessions to bring your total cash needed down. If the seller refuses to budge, walk away and look for a property with a better equity gap.

For Deep Discount Rare Deals

Confirm your comparable sales data before getting too excited about the high margin. A deal below 70% often indicates a mistake in your estimated after-repair value. Search for 3 to 5 sold properties from the last 90 days to verify the price ceiling. If the numbers hold up, use your cash position to close the deal before other investors spot the equity.

Check the title for hidden liens or legal issues that might explain the low price. Deep discounts sometimes come with structural problems that a standard rehab budget cannot cover. Perform a thorough walkthrough to ensure your repair estimate is realistic. These deals are rare in 2026 and require immediate action once you verify the facts.

You Might Also Find These Helpful

Real Estate 3

No tools published here yet.

Related Tools People Use Next

Why Your Maximum Allowable Offer Result May Be Incorrect

Even a highly accurate MAO calculator fails if your inputs are flawed. Most investors lose money because they underestimate hidden fees or use unrealistic property values. Review these frequent errors to ensure your calculated strike price actually protects your business capital in the real world.

- Relying on automated online Zestimates instead of pulling accurate sold comps from your local MLS.

- Forgetting to include back-end seller agent commissions and closing costs in your fixed fee total.

- Failing to multiply your monthly hard money interest and utilities by the total months you hold the property.

- Demanding a wholesale assignment fee that pushes the end cash buyer out of their safe profit margin.

- Assuming the equity buffer reserved by the 70 percent rule represents pure cash profit instead of gross margin.

Frequently Asked Questions (FAQs)

Does the 70% rule work for high-end luxury flips?

No. In luxury markets with high after repair values, the 70% rule creates offers that are far too low. Professional investors switch to a “Fixed Profit” model, subtracting a specific dollar amount for profit rather than a massive percentage.

How do I use the MAO formula for a BRRRR rental property?

Use the 75% or 80% rule instead of the standard 70%. Banks typically refinance investment properties at 75% of the appraised value. Buying at this higher limit allows you to recover your capital while keeping the property as a cash-flowing rental.

What should I do if my calculated MAO offends the seller?

Use your calculation as an objective negotiation tool. Show the seller your detailed repair estimates and local sold comps to justify your offer. If the gap remains too wide, walk away. Overpaying on your MAO guarantees a financial loss.

Should I include a contingency buffer in my repair estimates?

Yes. Always add a 10% to 15% contingency buffer to your rehab budget before calculating your final offer. This financial cushion protects your profit margin from hidden structural issues, mold discoveries, or sudden 2026 material price hikes.

Does the maximum allowable offer include agent commissions?

Yes. Your MAO must account for all fixed acquisition and disposition costs. This includes the commission for the agent finding the deal, plus all closing costs. Failing to subtract these specific fees creates a deal that barely breaks even.

What is the difference between ARV and MAO?

After Repair Value (ARV) represents the estimated market price of the home after all renovations are finished. Maximum Allowable Offer (MAO) is the heavily discounted price you must pay upfront to secure the deal. ARV is your retail finish line. MAO is your strict wholesale starting point.

When should I use the 65 percent rule instead of 70 percent?

You should drop your equity limit to 65 percent if you plan to sell the finished house using a real estate agent. This extra reduction safely absorbs standard realtor commission fees. It also provides a vital safety net when flipping houses in a slower buyer’s market.

Does the MAO formula apply to Subject-To or creative finance deals?

No, the standard MAO calculation is built specifically for cash or hard money purchases. Creative finance deals prioritize monthly cash flow, existing interest rates, and loan terms over the raw purchase price. Taking over a low-rate mortgage often justifies paying much closer to the actual retail value.

How much cash should I set aside for a rehab reserve fund?

You need to hold 10 to 20 percent of your total renovation budget in a dedicated reserve fund. Older properties require the full 20 percent to cover hidden foundation or plumbing issues. This emergency cash ensures unexpected contractor discoveries do not stall your entire project.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.