Gift of Equity Calculator: Lock In Equity & Avoid Tax Traps

A gift of equity occurs when a family associate sells you a home below its appraised market value. The price difference becomes your instant equity. Lenders treat this “paper money” as your actual down payment. You can secure a mortgage and bypass private mortgage insurance without bringing physical cash to closing.

Buying a parent’s house feels like a massive financial shortcut. Most families accidentally trigger IRS audits or leave the seller financially underwater. You need to know if this transfer is a true head start or a hidden financial trap.

Our calculator reveals your exact new loan amount. It tracks the seller’s actual net cash profit to ensure their old mortgage is cleared. You will also instantly generate the exact legal gift letter your underwriter requires.

Quick Facts

- Instant Down Payment: Replaces cash out of pocket.

- PMI Bypass: Eliminates mortgage insurance if the gift exceeds 20 percent.

- Tax Alerts: Checks transfers against the IRS annual exclusion threshold.

- Auto-Letter: Generates a lender-approved document instantly.

- Updated Jun 17, 2026

- Reviewed by 100Calc Research Team

Family Real Estate Transfer

Gift of Equity Calculator

Calculate the exact equity gift, the buyer's new mortgage payment, and the seller's net cash proceeds. This simple mortgage calculator with gift of equity also flags IRS tax thresholds and auto-generates your lender-required gift letter.

Total Gift of Equity

Effective Down Payment:

The Home Value Breakdown

Buyer's Side

Seller's Side

Your Automated Equity Gift Letter

Lenders require formal documentation. Copy the pre-filled template below.

How to calculate gift of equity?

What is 1 equity of 1 crore?

What is the gift of equity rule?

Is there a maximum gift of equity?

Explore More Calculators

Calculate your exact strike price with our free Maximum Allowable Offer Calculator. Factor in the 70% rule, repairs, and 2026 holding costs fast.

Try calculatorUse our Car Trade-In Tax Savings Calculator to uncover your exact discount instantly. Stop losing money to hidden showroom math and beat private sales.

Try calculatorNominal gains lie. Use our real estate appreciation calculator to track compound growth, subtract inflation, and reveal your true property equity.

Try calculatorExplore Related Tools

What Your Gift of Equity Result Means

Your result breaks down the entire family transaction. The total gift shows exactly how much wealth transfers to the buyer without exchanging physical cash. The buyer section reveals the exact size of the new mortgage required to finalize the purchase. The seller section provides a critical reality check by tracking their actual cash payout.

Understanding Your Result

The final numbers separate your family discount from the actual bank loan. Lenders care deeply about the effective down payment percentage. A higher percentage lowers the lender’s risk and makes mortgage approval much easier.

Sellers must watch their net cash at close. This specific metric subtracts their existing mortgage payoff from the agreed family sale price. It shows true profit and protects the seller from taking an accidental loss.

Is Your Result Good or Bad?

A good result leaves the buyer with at least 20 percent instant equity. Hitting this exact mark completely eliminates private mortgage insurance. Skipping PMI saves the buyer thousands of dollars over the life of the loan.

A bad result leaves the seller financially underwater. If the net cash drops below zero, the family sale price fails to cover the seller’s original bank loan. The seller must bring personal cash to the closing table just to get rid of the house.

What You Should Do Next

- Review your effective down payment percentage to see if the buyer needs to add extra cash to avoid PMI.

- Verify the seller’s net cash to ensure the parents or relatives do not lose money at closing.

- Copy the automated gift letter below the calculator and send it straight to your loan officer.

- Consult a certified public accountant if the IRS Form 709 warning triggers for your family structure.

A Quick Example to Test

Imagine parents selling a home appraised at $400,000 to their son for $320,000. They currently owe $250,000 to their original lender.

Input:

- Appraised Value: $400,000

- Family Sale Price: $320,000

- Extra Cash Down: $0

- Seller Mortgage: $250,000

Result:

The son receives an $80,000 gift. This creates a perfect 20 percent down payment. He skips mortgage insurance entirely.

Meaning:

The new loan amount sits at $320,000. The parents clear their old debt and walk away with $70,000 in pure net cash. The transaction protects the seller while giving the buyer a massive financial head start.

Micro Insight

A gift of equity turns a family home into a financial head start. It bypasses the hardest part of buying a house by eliminating the cash down payment. You gain instant wealth while keeping the property safely in the family legacy.

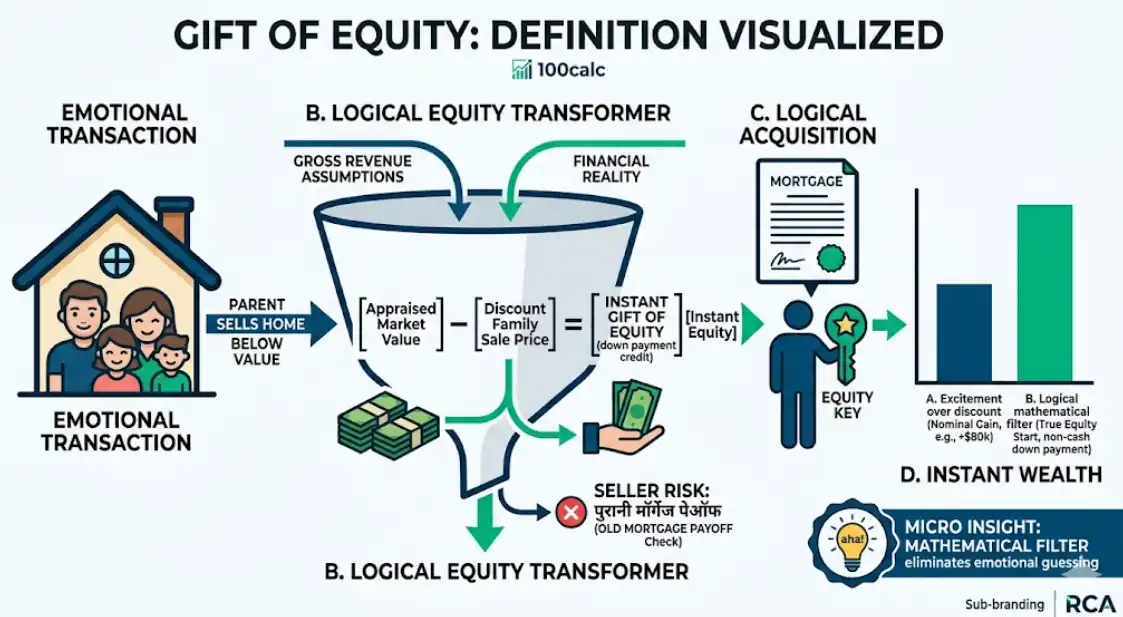

What is a Gift of Equity?

A gift of equity happens when a relative sells you a property below its official market value. The seller gives the price difference as a credit to the buyer. This credit acts as a down payment. It helps buyers secure a mortgage without needing personal cash.

Lenders view this equity as a non-cash down payment. It allows parents or relatives to transfer wealth and homeownership simultaneously. Unlike a cash gift, no physical money moves from the seller to the buyer’s bank account. The discount simply becomes the buyer’s initial stake in the home.

Imagine an uncle selling a $400,000 house to his niece for $320,000. The $80,000 difference represents the gift. The niece gets a loan for the lower price but starts with 20 percent equity. This setup helps her avoid monthly mortgage insurance fees completely.

Sellers must remain careful about their remaining loan balance. The discounted sale price must completely cover their existing mortgage. Failing to verify this can force sellers to pay their bank just to leave the house. Most banks also require a formal letter to prove the transfer is permanent.

Which Loan Type Allows a Gift of Equity?

Different mortgage programs have specific rules on how you can apply gifted equity toward your down payment and closing costs. Review the 2026 standards below to ensure your family transaction meets your lender’s strict underwriting guidelines.

| Loan Program | Flexibility | Acceptable Donors | Eligible Properties | Notes |

|---|---|---|---|---|

| Conventional (Fannie Mae) | High | Direct family, fiancés, or domestic partners. | Primary residences and second homes. | Can cover 100% of the down payment and all closing costs. |

| FHA Loan | Medium | Family, close friends, or employers. | Primary residences only. | Easily covers the 3.5% minimum down payment and standard fees. |

| VA & USDA Loans | Medium | Family or close friends (no interested parties). | Primary residences only. | Applies directly to closing costs, as no down payment is required. |

Heads-up: Lenders require a formal, signed gift letter proving no repayment is expected, regardless of the mortgage program you select.

How to Use the Gift of Equity Calculator

Our system simplifies the financial logic behind family real estate transfers. It compares the market appraisal against your discounted family price to locate your instant equity. The engine then checks your exact mortgage terms to calculate monthly costs and IRS thresholds. Here is exactly how the process works behind the scenes.

Enter the Market and Family Sale Prices

Input the official home appraisal value and the discounted family price. The calculator subtracts the sale price from the appraisal to locate the exact gift of equity. This number acts directly as the buyer down payment credit.

Add Cash Down and Loan Terms

Include any physical cash the buyer plans to bring to closing. Select the preferred loan term between a 15-year or 30-year fixed mortgage. The system subtracts this cash from the family sale price to determine the exact new loan amount.

Set the Current Mortgage Interest Rate

Use the slider or text box to input the current market interest rate. The calculator applies standard amortization math using this rate against the new loan amount. This creates the exact monthly principal and interest payment the buyer will owe.

Input the Seller Mortgage Payoff Balance

Enter the exact amount the selling family members still owe their original bank. The tool subtracts this old debt from the new family sale price. This step proves whether the seller will walk away with cash profit or owe money at closing.

Select Your Family Structure for IRS Limits

Choose the exact number of givers and receivers involved in the transaction. The engine multiplies these numbers against the current IRS annual exclusion limit. It instantly flags whether the transfer requires the seller to file a standard IRS Form 709.

How do you calculate a gift of equity transfer with an extra cash down payment?

Find the appraisal value and the agreed family discount. Add any physical cash the buyer brings to the table. The calculator processes these numbers to find the exact final loan amount.

Use these inputs in the calculator:

- Appraised Value: $600,000

- Family Sale Price: $480,000

- Extra Cash Down: $20,000

- Loan Term: 30 Years

- Interest Rate: 7.0%

- Seller Mortgage: $150,000

Process:

The tool subtracts the $480,000 price from the $600,000 appraisal to find a $120,000 gift. It then subtracts the $20,000 cash down from the $480,000 sale price to size the mortgage.

Final Result:

The New Loan Amount is $460,000.

Meaning:

The buyer secures the home using a massive $140,000 combined down payment. This drastically lowers their monthly mortgage cost and completely avoids private mortgage insurance.

Accuracy Behind the Gift of Equity System

Real estate transfers require exact math to satisfy strict bank underwriters and IRS auditors. This system applies standard lending formulas to separate the appraised value from the actual financed loan amount. It ensures your family sale structure remains financially viable before you submit a formal mortgage application.

Key Features & Benefits

- Determines exact Loan-to-Value ratios to flag mandatory private mortgage insurance.

- Audits your transfer amount against the published IRS annual exclusion limits.

- Calculates exact net closing cash to prevent sellers from taking accidental losses.

- Formats automated legal text to meet standard mortgage underwriter documentation rules.

- Processes financial data across multiple global currencies for international family transfers.

Technical Process

Data Capture

Captures property values, loan terms, and family structures to establish a valid financial baseline.

Logic Processing

Applies standard lending formulas and tax thresholds to calculate equity, monthly costs, and profits.

Output Generation

Displays the final mortgage metrics, legal documents, and critical tax alerts for immediate review.

How the Gift of Equity Formula Works (Complete Breakdown)

The gift of equity formula uses basic subtraction to bridge the gap between a property’s market value and your family discount. It calculates the exact down payment credit, sizes the new mortgage, and checks strict IRS exclusion limits. This ensures your family transfer satisfies both lenders and tax auditors perfectly.

The Gift of Equity Formulas

The gift of equity formula uses simple subtraction to bridge the gap between a property’s market value and your family discount. These equations calculate your exact down payment credit, size the new mortgage, and check strict IRS exclusion limits to ensure the transfer satisfies your lender.

Formula:

Gift of Equity = Appraised Value - Family Sale Price

New Loan Amount = Family Sale Price - Cash Down Payment

Seller Net Cash = Family Sale Price - Seller Existing Mortgage

IRS Tax Threshold = Givers × Receivers × 18000

This formula calculates exactly how much paper wealth transfers between family members. It strips away the family discount to find the buyer’s true loan requirement. It also subtracts the seller’s old debt from the new price, guaranteeing the parents or relatives actually walk away with profit instead of owing the bank money.

The Core Variables Decoded

Every family real estate transfer relies on a few critical financial inputs. These specific numbers determine your final mortgage balance, your down payment percentage, and your potential tax reporting obligations. Here is exactly what each variable means for your transaction.

Appraised Value

This is the official market worth of the home. A licensed appraiser determines this number for the bank. It acts as the financial ceiling for your entire transaction and establishes the maximum equity available.

Family Sale Price

This represents the heavily discounted price you agree to pay your relatives. The bank uses this exact number as the actual purchase price. It must sit below the official appraisal to create a valid gift.

Cash Down Payment

This is the physical, out-of-pocket money the buyer brings to the closing table. While optional in these family transactions, adding cash reduces the total loan amount and helps bypass expensive mortgage insurance faster.

Seller Existing Mortgage

This is the exact dollar amount the selling family members still owe their original bank. The final family sale price must completely cover this old debt to prevent the seller from taking a cash loss.

Givers and Receivers

This defines your family structure. The IRS allows each giver to gift a specific amount to each receiver annually without reporting it. Multiplying these people by the $18,000 base limit determines your final tax reporting threshold.

Another Example Calculation (Step-by-Step)

Let’s test a realistic family transfer where parents sell a property to their daughter, including a small cash down payment. This scenario highlights how the system protects the seller’s net proceeds while eliminating the buyer’s mortgage insurance.

Given:

- Appraised Value: $450,000

- Family Sale Price: $350,000

- Cash Down Payment: $10,000

- Seller Existing Mortgage: $210,000

- Givers: 2 (Parents)

- Receivers: 1 (Daughter)

Calculation:

Gift of Equity = 450,000 - 350,000 = $100,000

New Loan Amount = 350,000 - 10,000 = $340,000

Seller Net Cash = 350,000 - 210,000 = $140,000

IRS Tax Threshold = 2 × 1 × 18000 = $36,000

Result:

- Total Gift: $100,000

- New Loan: $340,000

- Seller Profit: $140,000

- Tax Status: Form 709 Required ($100k exceeds $36k limit)

Meaning:

The daughter receives a massive $100,000 instant down payment. She only finances $340,000 and skips PMI entirely. Meanwhile, the parents clear their old $210,000 debt and safely walk away with $140,000 in pure cash. Because the $100,000 gift crosses the $36,000 IRS threshold, the parents simply file a reporting form with their annual tax return.

How do you calculate a gift of equity?

Subtract your agreed family sale price from the official appraised market value. The difference becomes your instant gift of equity. Lenders treat this exact amount as your down payment. You then subtract any extra cash from the sale price to find your final mortgage loan amount.

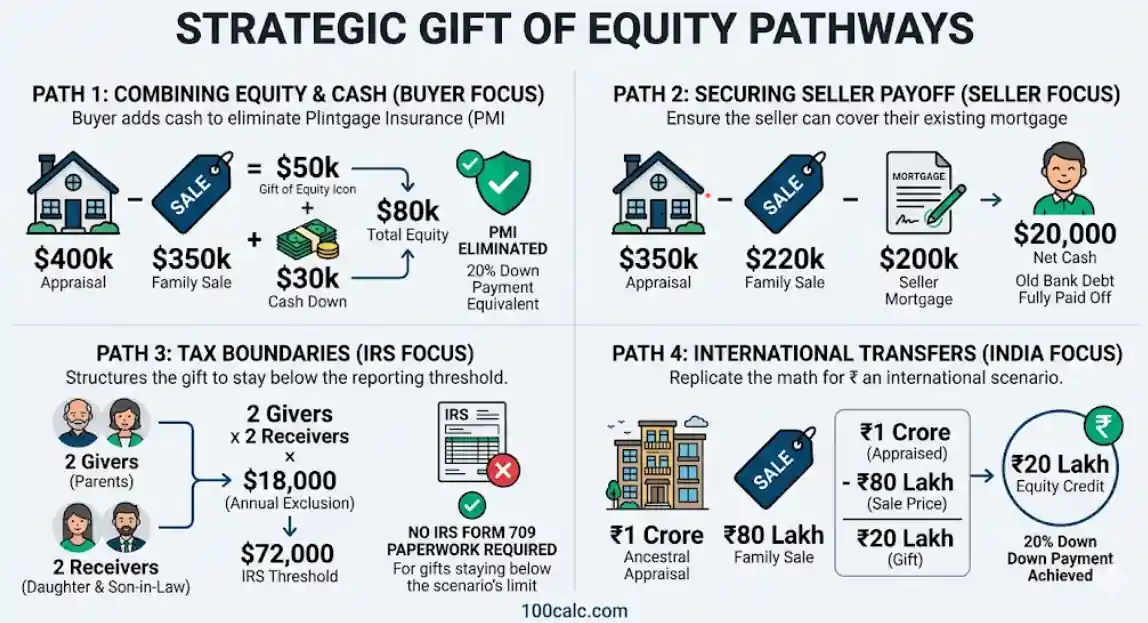

How does a gift of equity work as a down payment with extra cash?

A buyer wants to avoid expensive mortgage insurance but the family discount falls short of 20 percent. They decide to bring personal savings to the closing table.

Input Values:

- Appraised Value: $400,000

- Family Sale Price: $350,000

- Extra Cash Down: $30,000

- Seller Mortgage: $100,000

Process:

The system finds a $50,000 family discount. It adds the $30,000 cash down to reach $80,000 in total equity. The new loan drops to $320,000.

Result:

Effective Down Payment: 20% New Loan Amount: $320,000

Meaning:

The buyer successfully combines the family discount with their own savings to hit the golden 20 percent mark. This strategy completely eliminates monthly private mortgage insurance.

How does a family sale affect the seller's mortgage payoff?

Parents want to give their child a massive discount on the family home. They must price it carefully to ensure they can still pay off their original bank loan.

Input Values:

- Appraised Value: $350,000

- Family Sale Price: $220,000

- Extra Cash Down: $0

- Seller Mortgage: $200,000

Process:

The calculator subtracts the $220,000 sale price from the appraisal to reveal a $130,000 gift. It then subtracts the parents’ old $200,000 debt from the sale price.

Result:

Total Gift of Equity: $130,000 Seller Net Cash: $20,000

Meaning:

The parents safely clear their original bank debt and keep a small $20,000 profit. The child secures a massive down payment without leaving the parents financially underwater.

How do you structure a gift of equity to avoid IRS reporting?

Married parents want to sell a house to their married daughter and son-in-law. They want to maximize their tax-free transfer limit.

Use these inputs in the calculator:

- Appraised Value: $600,000

- Family Sale Price: $540,000

- Givers: 2

- Receivers: 2

Process:

The tool calculates a $60,000 equity gift. It then multiplies the two givers by the two receivers, and multiplies that by the $18,000 base exclusion.

Result:

Total Gift of Equity: $60,000 IRS Tax Threshold: $72,000

Meaning:

The family stays safely below the federal reporting limit. Because four people are involved in the contract, the tax threshold quadruples. This requires zero IRS Form 709 paperwork.

How does a 1 Crore property transfer work in India?

An uncle sells an ancestral flat in Mumbai to his nephew. They need to figure out the exact down payment credit in rupees.

Input Values:

- Appraised Value: ₹10,000,000 (1 Crore)

- Family Sale Price: ₹8,000,000 (80 Lakhs)

- Extra Cash Down: ₹0

- Seller Mortgage: ₹0

Process:

The calculator subtracts the 80 Lakh sale price from the 1 Crore market appraisal.

Result:

Total Gift of Equity: ₹2,000,000 (20 Lakhs) Effective Down Payment: 20%

Meaning:

The nephew receives 20 Lakhs in instant paper wealth. This fulfills the strict down payment requirements for Indian home loans without moving actual rupees between bank accounts.

Quick rule to remember

Look at the seller’s net cash first. Protect the parents from taking an accidental financial loss. Once the old debt is covered, maximize the family discount to eliminate PMI for the buyer. Now you can enter your own property details into the calculator to solve your specific financial problem instantly.

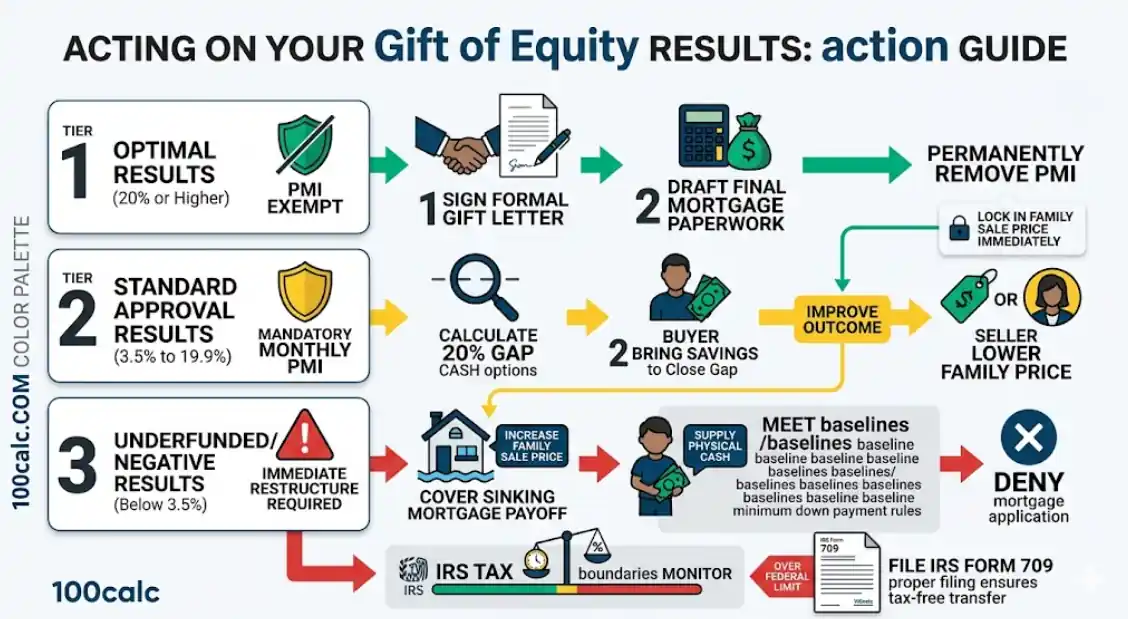

Gift of Equity Result Benchmarks Explained

Your effective down payment percentage dictates your loan approval and monthly costs. It determines if you must pay expensive mortgage insurance. Lenders strictly follow these ranges to evaluate your family transfer. Here is how your result impacts your actual mortgage terms.

| Range | Label | Conventional Loans | FHA Loans | Notes |

|---|---|---|---|---|

| 20% or Higher | Optimal | Bypasses private mortgage insurance entirely. | FHA still requires standard mortgage premiums. | Best case scenario for buyer affordability. |

| 3.5% to 19.9% | Standard | Qualifies but adds costly monthly PMI. | Meets standard 3.5% down requirement. | Expect a higher monthly housing payment. |

| Below 3.5% | Underfunded | Application denied without extra cash. | Application denied (except VA/USDA). | Buyer must bring physical cash to closing. |

Heads-up: Lender underwriting policies change constantly. Always verify exact down payment rules with your local loan officer.

Interpreting Your Loan Status

Hitting the twenty percent mark is your primary financial goal. This optimal range permanently removes mortgage insurance from your monthly bill. Falling into the standard tier still secures the house but increases your long-term expenses. Results below the minimum limit usually trigger a harsh denial from bank underwriters.

Pro Tip:

Always calculate your seller’s remaining mortgage before finalizing the gift amount. You can adjust the family sale price or add physical cash to hit the perfect twenty percent threshold safely.

What to Do After Using the Gift of Equity Calculator

Your final calculator result is a financial starting point, not a guaranteed closing document. The next step is adjusting your family sale price or cash reserves to optimize your mortgage application. Use these targeted recommendations based on your specific equity percentage to finalize a successful family real estate transfer.

For Optimal Results (20% or Higher)

Lock in your family sale price immediately if your gift reaches the 20 percent threshold. This optimal standing permanently removes private mortgage insurance from your loan. Instruct your loan officer to draft the final paperwork using this exact price difference. Ensure both the selling parents and the buyer sign the automated gift letter provided by the calculator before submitting the application.

For Standard Approval Results (3.5% to 19.9%)

You qualify for standard loan programs but will pay mandatory monthly mortgage insurance. To improve this outcome, calculate the exact cash difference needed to reach the full 20 percent mark. The buyer should consider bringing personal savings to the closing table to close that gap. Alternatively, the seller agrees to lower the family sale price slightly to increase the gifted paper equity.

For Underfunded or Negative Results (Below 3.5% or Underwater)

This result requires immediate restructuring before you apply for a loan. If the seller’s net cash drops below zero, increase the family sale price until it safely covers their old mortgage payoff. If the buyer’s equity falls below standard FHA minimums, the buyer must supply physical cash. Lenders will immediately deny a mortgage application if the combined cash and gift do not meet strict baseline down payment rules.

Monitor IRS Tax Boundaries

Watch your IRS threshold result carefully before finalizing the contract. The federal limit for tax-free gifts changes slightly every year. If your equity transfer exceeds the current limit, do not panic or cancel the sale. Hire a certified public accountant to properly file IRS Form 709, ensuring the overage safely applies to your lifetime estate exemption rather than triggering immediate cash taxes.

You Might Also Find These Helpful

Real Estate 3

No tools published here yet.

Related Tools People Use Next

Common Mistakes When Using the Gift of Equity Calculator

Many families struggle with real estate transfers because the math feels like paper money. Small errors in your inputs often lead to rejected loan applications or cash losses. Understanding these common gift of equity calculator mistakes ensures your transaction satisfies bank underwriters.

- Confusing the home appraised market value with your actual new loan amount.

- Forgetting that the family sale price must completely cover the seller's original mortgage.

- Failing to sign a formal gift letter before submitting your final mortgage application.

- Assuming an IRS reporting alert automatically forces you to pay immediate cash taxes.

- Attempting to use your gifted paper equity to satisfy lender cash reserve requirements.

Frequently Asked Questions (FAQs)

Can you use a gift of equity with an FHA loan?

Yes. FHA guidelines allow a gift of equity to cover the entire 3.5% minimum down payment. The gift must come from an approved family member, and the home must serve as your primary residence. You will need an FHA-compliant gift letter to finalize the approval.

Does a gift of equity increase capital gains tax for the seller?

No. Selling below market value reduces your overall profit, which lowers your capital gains liability. However, the IRS still views the transaction as a sale at fair market value for cost-basis purposes. This rule protects the buyer from massive tax hits when they eventually sell.

Can a gift of equity be used on a second home or investment property?

Yes. Conventional Fannie Mae guidelines permit a gift of equity for a primary residence or a second vacation home. However, you generally cannot use a gift of equity to purchase a pure investment property. Lenders restrict family gifts to homes meant for personal use.

What happens if the home appraisal comes in lower than the sale price?

A gift of equity relies entirely on the official appraised value. If the home appraises lower than the agreed family sale price, the equity disappears. You must either lower the family sale price below the new appraisal or bring physical cash to the closing table.

Can a gift of equity cover all of the buyer's closing costs?

Yes. Most conventional and FHA lenders allow you to use excess gifted equity to pay for standard closing costs and loan origination charges. If the family discount is large enough, you can buy the house with zero physical cash out of pocket.

Does the buyer have to pay income tax on gifted equity?

No. A gift of equity is not considered taxable income for the recipient. The IRS views it simply as a transfer of property value. While the seller might need to file a reporting form, the buyer receives the instant wealth completely tax-free.

How exactly does a gift of equity affect the seller?

The seller walks away with less physical cash than they would in a traditional open-market sale. The final family sale price must be high enough to completely pay off any existing mortgage the seller still holds. Otherwise, they will owe money at closing.

Do you need a real estate agent for a gift of equity transfer?

No. Because these transfers usually happen between close family members, most people hire a real estate attorney instead of an agent. Skipping the traditional agent route eliminates standard six percent commission fees. This keeps significantly more wealth inside the family.

What is the relationship between gifted equity and Loan-to-Value (LTV)?

Your LTV compares your new loan amount against the home’s official appraised value. A large equity gift instantly lowers your LTV ratio. Lenders prefer a lower LTV because it reduces their financial risk. This often secures you a much better mortgage interest rate.

What is a non-arm's length transaction?

A non-arm’s length transaction occurs when buyers and sellers have a pre-existing relationship, such as family members. Lenders flag gifts of equity under this category. This simply means the underwriter will require a formal gift letter and a strict independent appraisal to prevent mortgage fraud.

How does a gift affect the buyer's future capital gains?

The buyer inherits the seller’s original tax cost basis, plus the gifted amount. This is called a carryover basis. If the parents bought the house for a very low price decades ago, the child might face higher capital gains taxes when they eventually sell the property to a stranger.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.