Real Estate Calculators: Run Your Own Numbers Before the Bank Does

What are real estate calculators? They are free online tools that help buyers, sellers, and investors estimate true property costs. You can calculate exact monthly mortgage payments, project long-term appreciation, and find your actual return on investment. These tools turn confusing property data into clear financial answers.

Most basic bank calculators just spit out a monthly payment and leave you guessing. Worse, lenders often use biased math to approve you for massive loans that break your actual household budget. You need to run your own “what-if” scenarios before signing any paperwork. Whether you are avoiding a mortgage trap, valuing a family equity transfer, or analyzing a wholesale flip, you need the unvarnished truth.

Browse our complete collection of real estate tools below. Choose the exact calculator you need to measure investment yields, plan your next home purchase, and make smarter property moves with total confidence.

- Fast estimates

- Clear formulas

- Updated regularly

Explore Real Estate Calculators

Pick a calculator based on your exact property goal. Every tool below solves a specific financial problem for buyers, sellers, or wholesale investors. Select the option that matches your current deal. You will get clear numbers and instant results to guide your next move.

Real Estate 4

Calculate your exact strike price with our free Maximum Allowable Offer Calculator. Factor in the 70% rule, repairs, and 2026 holding costs fast.

Try calculatorUse our Car Trade-In Tax Savings Calculator to uncover your exact discount instantly. Stop losing money to hidden showroom math and beat private sales.

Try calculatorBuying a family home? Calculate your exact gift of equity to bypass PMI instantly. See your new mortgage payment, tax limits, and get a…

Try calculatorNominal gains lie. Use our real estate appreciation calculator to track compound growth, subtract inflation, and reveal your true property equity.

Try calculatorOther Finance tools you may find useful

What is Real Estate Finance?

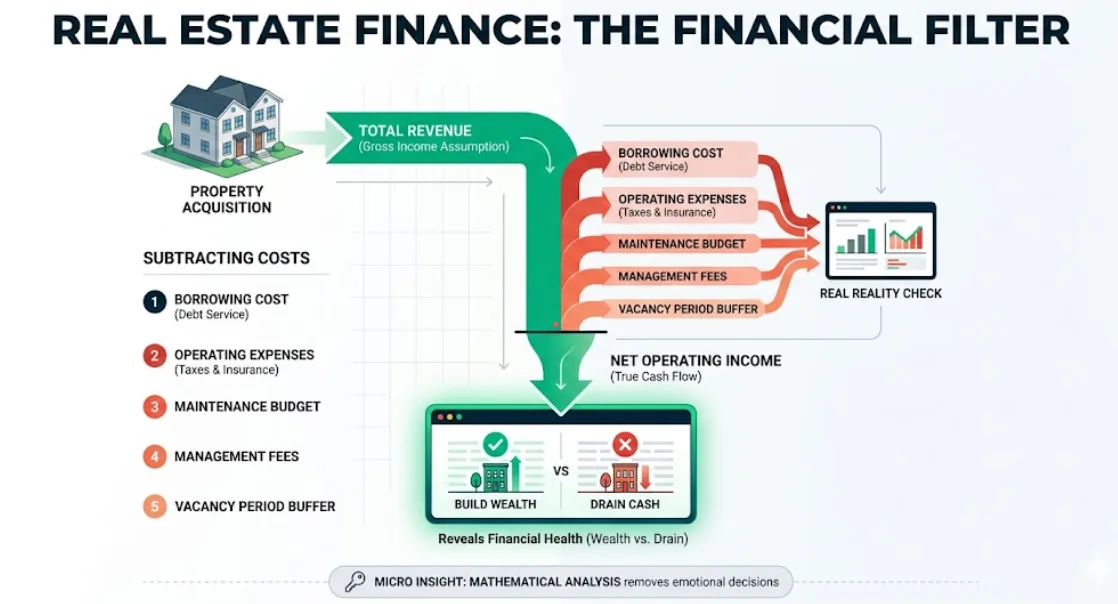

Real estate finance is the management of money used to acquire, hold, or sell property. It moves beyond a simple purchase price to analyze the true cost of borrowing, operating expenses, and long-term cash flow. This math helps buyers and investors determine if a building builds wealth or drains cash.

Standard personal finance deals with liquid assets like savings accounts or stock market shares. Property investment involves physical buildings that require ongoing maintenance, local taxes, and specialized bank loans. You must carefully balance the debt you take on against the income the asset generates. Small changes in interest rates or insurance premiums drastically alter your potential return on investment.

Consider a person purchasing a small duplex to rent out. They might assume the monthly rent perfectly covers the bank loan. True real estate finance forces them to subtract property management fees, repair budgets, and vacancy periods from that gross income. The remaining net operating income dictates whether the deal is actually profitable.

Micro Insight

Mastering these exact numbers protects you from high-risk deals. Clear mathematical analysis removes emotional excitement from buying decisions. It reveals the exact financial health of a property before you sign any legally binding contracts.

What Real Estate Math Actually Exposes Before Closing

Property formulas help you test the exact numbers behind a housing deal. You can project long-term equity, expose hidden holding costs, and find your precise profit margin. Buyers and investors rely on this data to verify bank estimates and avoid bad investments.

Key Tasks Users Perform

Expose true monthly costs

Factor in local property taxes and strict HOA fees to reveal your actual living expenses.

Find your maximum offer

Calculate wholesale flip margins using estimated repair budgets and target profit percentages.

Estimate net sale proceeds

See exactly how much cash remains in your pocket after agent commissions and closing fees.

Project long-term equity

Forecast family wealth growth based on specific local market appreciation trends.

Core Inputs Used

After Repair Value (ARV)

The estimated market price of a distressed property once it is fully renovated and upgraded.

Holding and maintenance costs

The monthly cash required to manage, repair, or float an active investment property.

Agent commissions and fees

The mandatory percentages paid to brokers and title companies during a standard property transfer.

Local tax and insurance rates

The exact annual percentages required to keep the physical asset legally compliant and fully protected.

Exposing Bank Math: How Our Real Estate Calculators Process Your Deal

Our property tools process your inputs using strict underwriting formulas. We combine standard loan amortization rules with real-world investment metrics like net operating income. This delivers mathematically pure estimates and strips away the deceptive marketing assumptions lenders often use to hide true costs.

The Hidden Local Variables That Break Basic Property Estimates

Mathematical accuracy depends strictly on the localized numbers you provide. A pure calculation cannot predict your specific county property tax reassessment. It also cannot guess mandatory homeowners insurance premiums or sudden spikes in local repair budgets.

Real estate costs are heavily driven by local municipality laws. Your actual out-of-pocket expenses will shift based on these external factors. Failing to input realistic tax and insurance data will severely skew your final results.

Insight: Underestimating local property taxes is the primary reason new buyers struggle to afford their monthly payments after closing.

The Processing Engine: How Raw Property Data Becomes Your Monthly Payment

The Processing Engine: How Raw Property Data Becomes Your Monthly Payment Online tools map your inputs against a fixed timeline. The system takes your total purchase price, applies the annual percentage rate, and divides it across your specific loan term. This generates a baseline monthly cost and reveals your total lifetime interest.

Most property debt uses a declining balance model. As you pay down the principal, the interest charge drops. Our tools calculate this exact shift for every single payment period.

Insight: Banks heavily front-load interest charges during the first five years of a mortgage to secure their profits before you sell or refinance.

Unmasking the Formulas: Why We Reject Flat Rate Banking Illusions

We build our logic using recognized commercial real estate equations and compound growth models. Our systems calculate standard home loan amortization and complex capitalization rates. This matches the exact underwriting standards used by licensed mortgage brokers and institutional investors.

We refuse to use simple flat-rate math. Flat assumptions hide the true cost of borrowing money over decades. Our systems break down the compounding effect so you see the real financial impact immediately.

Insight:Lenders often quote a low base interest rate verbally, but process your actual contract using an Annual Percentage Rate that hides expensive origination fees.

The Closing Shock: Why Your Final Bank Documents Will Look Different

Your official loan documents will always look slightly different than a free online estimate. This happens because lenders calculate daily interest based on the exact date you close. Standard calculators assume every month is perfectly equal.

Online tools also assume perfect payment behavior. If you make a payment three days late, your actual amortization timeline shifts instantly. Extra escrow padding required by the title company will also change your final cash-to-close amount.

Insight:A variation of twenty to fifty dollars a month is completely normal when moving from an internet estimate to a legally binding mortgage contract.

Outdated Math is Dangerous: How We Adapt to Shifting Housing Laws

We regularly audit our underlying calculation logic to match current banking regulations and federal tax guidelines. When the financial industry shifts how it handles early payoff penalties or capital gains taxes, we adjust our formulas immediately.

Real estate laws constantly evolve at both the state and federal levels. We monitor these changes to ensure our tools reflect current market realities. This prevents you from using obsolete math to make modern property decisions.

Insight: Relying on an outdated spreadsheet from five years ago is the fastest way to accidentally trigger an unexpected capital gains tax bill when selling a house.

Important note: Results are estimates. For major decisions, verify with a qualified professional.

Are Your Numbers Safe? Standard Real Estate Benchmarks

Knowing your exact monthly payment solves only half the problem. You must also figure out if that payment is actually safe for your budget. These standard benchmarks help you judge whether a property deal builds long-term wealth or pushes you toward bankruptcy.

| Range | Metric | Meaning | What To Do |

|---|---|---|---|

| Below 36% | Healthy DTI | Your total debt compared to income is safe. | Proceed with loan applications confidently. |

| 6% to 10% | Good Cap Rate | Solid return on a commercial rental property. | Verify local vacancy rates before buying. |

| Above 30% | Housing Danger | Your mortgage eats too much of your salary. | Lower your purchase budget to avoid stress. |

Heads-up: These are general guidelines. Exact safety limits depend heavily on your current credit score and economic inflation.

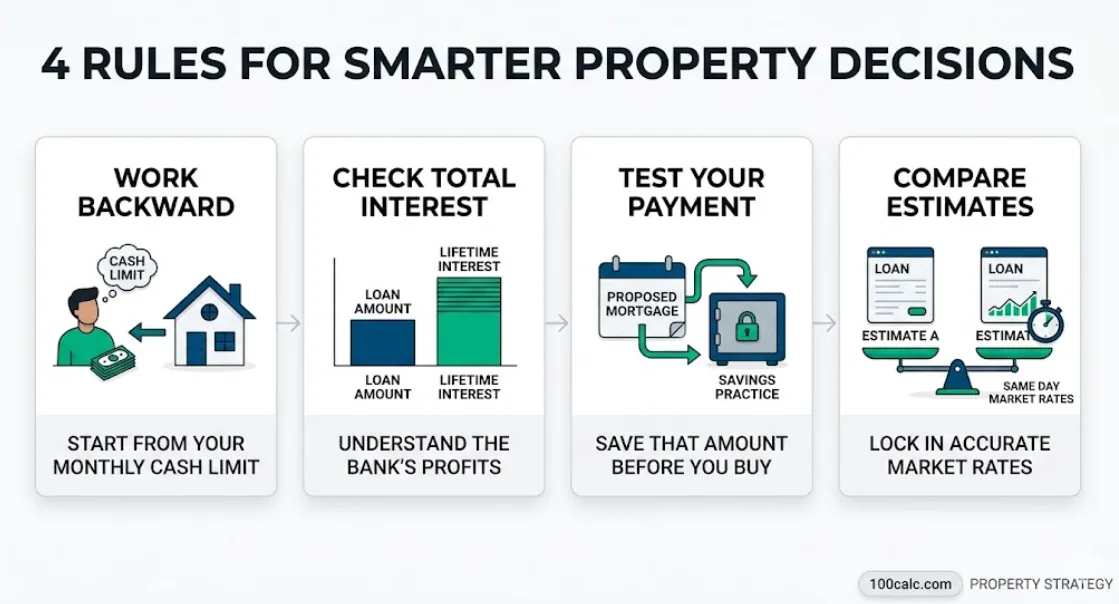

Stop Guessing: Rules for Smarter Property Decisions

- Work backward from your monthly cash limit instead of asking a bank how much you can borrow.

- Always check the total lifetime interest to see how much the bank really profits from your loan.

- Test your proposed mortgage payment by saving that exact amount every month before you buy a house.

- Compare multiple loan estimates on the same day to ensure you lock in the most accurate market rates.

The 5 Most Expensive Property Math Mistakes

- Entering your gross salary when a calculator actually requires your net take-home pay.

- Basing your future property taxes on what the previous owner paid instead of the new purchase price.

- Forgetting to add mandatory HOA fees and private mortgage insurance to your monthly budget.

- Using the low advertised interest rate instead of the Annual Percentage Rate that includes hidden bank fees.

- Estimating a wholesale flip without including the monthly holding costs and final agent commissions.

Frequently Asked Questions (FAQs)

How much house can I really afford?

Do not rely solely on bank affordability calculators. Those tools only tell you the maximum risk a lender will accept, not what your daily budget can handle. Use a mortgage payment calculator and compare the total monthly housing cost directly against your actual take-home pay.

Are online real estate calculators accurate?

Yes, if you input all the real-world variables. A common mistake is calculating only principal and interest while forgetting local property taxes, HOA fees, and maintenance costs. Those hidden fees drastically change your actual monthly payment and cash flow.

What is a good ROI for real estate investing?

Typically, investors aim for an annual cash-on-cash return of 8% to 12%. However, this depends heavily on the local market and the physical condition of the property. Flipping a house requires completely different return targets than holding it for long-term rental income.

Does a Gift of Equity avoid taxes?

A gift of equity allows you to sell a house to a family member below market value. While it reduces the buyer down payment burden, the seller must report the transaction to the IRS if the gift exceeds the annual federal gift tax exclusion limit.

How do I calculate the MAO for a flip?

The standard Maximum Allowable Offer formula multiplies the After Repair Value by 70% and then subtracts your estimated repair costs. This ensures wholesale investors build in enough margin to cover expensive holding costs and secure a reliable net profit.

What is the difference between Cap Rate and Cash-on-Cash return?

Cap rate measures the annual yield of a property based on its total overall purchase price. Cash-on-cash return measures your annual profit compared only to the actual cash you invested out of pocket. Investors use cash-on-cash return to verify the immediate power of their down payment.

How should I estimate maintenance costs for a property?

A common rule of thumb is to allocate 1% of the total property value for annual maintenance. You should divide this number by twelve and add it to your monthly mortgage estimate. Older homes often require up to 2% to cover unexpected plumbing or roof repairs.

Should I use a rent versus buy calculator first?

Yes. Comparing rent against buying is the most critical first step in real estate. Buying a home involves massive upfront closing costs and heavy long-term interest payments. If you plan to move within five years, renting and investing your extra cash is usually the cheaper option.

Do these calculators work for international real estate?

Yes. Standard property formulas like loan amortization, cap rates, and cash-on-cash returns are currency-agnostic. Whether you are analyzing a deal in the USA, buying property in Australia, or investing in India, the underlying mathematical principles remain exactly the same.

Can I use online calculators for the real estate exam?

No. Testing providers like Pearson VUE strictly prohibit smartphones and online calculators during the real estate licensing exam. You are typically only allowed to use a basic, non-programmable handheld calculator provided by the testing center.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.

Ready to Analyze Your Next Deal?

Stop guessing and let the raw numbers guide your next real estate transaction. You already understand the hidden bank costs and know exactly what safety benchmarks to look for. Now it is time to apply this to your own property. Pick a tool below to get instant answers and move forward with total financial confidence.