Cost of Equity Calculator: Estimate Required Shareholder Returns

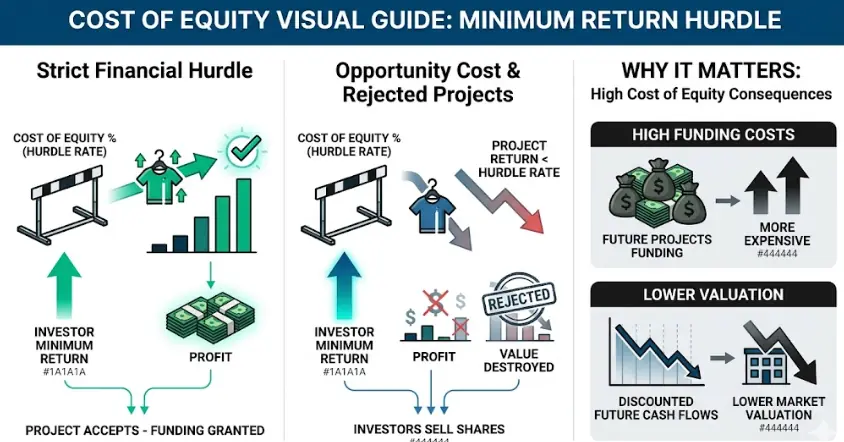

The cost of equity is the lowest rate of return a company must generate to satisfy its shareholders and compensate them for market risk. It serves as the primary “hurdle rate” for evaluating new corporate projects and forms the equity portion of a firm’s Weighted Average Cost of Capital (WACC).

Because equity investors sit at the bottom of the payout structure and get paid last during bankruptcy, they assume more risk than lenders. Consequently, the cost of equity is always higher than the cost of debt. If a company takes on projects that yield less than this required return, it actively destroys shareholder value.

Use this calculator to determine a company’s required return instantly. You can evaluate volatile growth stocks using the Capital Asset Pricing Model (CAPM) or analyze mature, dividend-paying companies using the Dividend Growth Model (DGM).

Quick Facts

- Calculates the minimum required return to justify market risk.

- Supports standard CAPM and custom Equity Risk Premium (ERP).

- Includes Dividend Growth Model (DGM) for mature companies.

- Generates the exact "E" value needed for WACC analysis.

- Updated Jun 10, 2026

- Reviewed by 100Calc Research Team

Corporate Valuation & Risk Engine

Cost of Equity Calculator

Determine the required rate of return for an equity investment using the Capital Asset Pricing Model (CAPM) or the Dividend Growth Model (DGM).

Use Standard CAPM to calculate cost using expected market returns.

Which method should I use?

CAPM is the standard for evaluating an asset's market risk profile via Beta. The Dividend Growth Model (DGM) is an alternative used for mature companies with a predictable dividend history.

Cost of Equity (Ke)

%

Market Benchmark Profile

Yield Composition

Calculation Summary

How do you calculate the cost of equity?

How do you calculate the cost of equity for WACC?

How do you calculate the cost of equity in CAPM?

How much would a $100,000 home equity loan cost per month?

What does Dave Ramsey say about a home equity loan?

What is the $100000 loophole for family loans?

Explore More Calculators

Use this After-Tax Cost of Debt Calculator to find your true effective rate. Factor in corporate tax shields, estimate Bond YTM, and uncover exact…

Try calculatorAre adjusters using flawed reports to lowball your claim? Calculate your true Actual Cash Value (ACV) to expose hidden depreciation and maximize payouts.

Try calculatorIs that high-yield dividend stock a trap? Use our Gordon Growth Model calculator to find its exact intrinsic value, set buy prices, and expose…

Try calculatorStandard IRR inflates your profits. Use our MIRR Calculator with WACC to calculate true project returns, safely reinvest cash, and find exact NPV instantly.

Try calculatorCalculate your true cash flow with our net operating profit after tax calculator. Strip away debt distortions from EBIT, EBITDA, or Net Income instantly.

Try calculatorAre you growing too fast? Use our sustainable growth rate calculator to find your exact revenue ceiling before a hidden cash deficit ruins your…

Try calculatorExplore Related Tools

What Your Cost of Equity Result Means

The final percentage is the absolute minimum return investors demand to hold this stock. It shows the exact financial hurdle your company must clear to justify its market risk.

Understanding Your Result

This percentage acts as a strict profitability baseline. If your company funds new projects that yield a lower return than this number, shareholder value actively drops.

Investors will sell their shares if you fail to meet this expected rate. A higher calculated number means the open market views your stock as a risky asset. The business must generate aggressive profits to maintain its current share price.

Is Your Result Good or Bad?

A lower cost of equity is generally good for corporate management. It means you can fund business operations cheaply because investors view your company as stable.

Rates between 6 and 8 percent typically represent safe assets like established utility companies. Rates above 12 percent indicate high market risk. Volatile technology startups often face these higher required returns to attract funding.

What You Should Do Next

Compare this required percentage directly against your projected internal project returns. Reject any new corporate investments forecasting a lower yield than this specific rate. Plug this exact figure into the equity portion of your Weighted Average Cost of Capital formula. Evaluate your current capital structure to see if issuing cheaper debt might lower your total funding costs.

A Quick Example to Test

Let us test a standard market calculation for a highly volatile technology stock.

Input:

- CAPM (Standard) Risk-Free Rate: 4.0%

- Stock Beta: 1.5

- Expected Market Return: 10.0%

Process:

The calculator subtracts the 4.0 percent safe rate from the 10.0 percent market return to find a 6.0 percent risk premium. It multiplies that 6.0 percent by the 1.5 beta. Finally, it adds the resulting 9.0 percent risk premium back to the 4.0 percent safe baseline.

Result:

- Cost of Equity = 13.00%

- State = High Risk Growth Asset

Meaning:

Investors require a 13.00 percent annual return to hold this volatile asset. Management must generate aggressive profits to justify this high risk level. You will plug this exact 13.00 percent figure directly into the equity portion of your WACC calculation to determine total corporate funding costs.

What is the Cost of Equity in Corporate Finance?

The cost of equity is the minimum rate of return a company must pay its shareholders to compensate them for market risk. It represents the absolute opportunity cost of investing. If a business fails to meet this expected percentage, investors will likely sell their shares and move their money elsewhere.

Think of this metric as a strict financial hurdle. When a business wants to expand, it needs capital. Banks charge interest for loans, which is easy to track on a balance sheet. Shareholders do not charge direct interest, but they still demand a specific profit margin in exchange for funding the business.

Imagine a retail brand launching a new clothing line. If the company’s cost of equity sits at 11 percent, the new product must generate at least an 11 percent profit margin. If the project only projects a 7 percent return, the financial team will reject the idea because it actively destroys shareholder value.

Why This Matters

A high cost of equity makes funding future projects much more expensive. It also directly lowers a company’s total market valuation when analysts discount future cash flows.

How to Use the Cost of Equity Calculator

This tool calculates the minimum return your investors require. It processes market volatility or dividend payouts to find this exact hurdle rate. Follow these five steps to model your capital costs accurately.

Select Your Financial Model

Choose between the Capital Asset Pricing Model or the Dividend Growth Model. Use CAPM to evaluate market volatility and risk premiums. Select the dividend method if you are analyzing a mature company with steady, predictable shareholder payouts.

Enter the Risk-Free Rate

Type in the baseline safe return for your calculation. Analysts typically use the current yield on a ten-year U.S. Treasury bond. This number gives the algorithm a secure foundation before it applies any additional market risk penalties.

Input the Stock Beta

Add the exact beta metric for your chosen company. This figure measures how much the stock price swings compared to the broader market. The system uses this volatility multiplier to scale the required risk premium up or down.

Define the Market Return

Enter the historical stock market average. The system subtracts the safe rate to isolate your equity premium. You can also enter a custom premium directly. For emerging markets, analysts use Aswath Damodaran’s data to add a Country Risk Premium (CRP), creating a highly accurate discount rate.

Review the Required Yield

Check your final calculated percentage to see the absolute minimum return investors demand. Review the visual chart to understand how much yield comes from the safe baseline versus the added market risk. Use this final number in your WACC model.

How do you estimate the required return for a slightly volatile public company?

Let us say you are evaluating a stock with a beta of 1.2 and want to find its total cost of equity. Use these exact inputs to test the CAPM logic.

Use these inputs in the calculator:

- Mode: CAPM (Standard)

- Risk-Free Rate: 4.2%

- Stock Beta: 1.2 Expected

- Market Return: 10.0%

Process:

The system subtracts the 4.2 percent safe rate from the 10.0 percent market return to find a 5.8 percent risk premium. It multiplies that premium by the 1.2 beta. It then adds the safe rate back to find the final yield.

Final Result:

- Cost of Equity: 11.16%

- Status: Moderate Market Risk

Meaning:

Investors demand an 11.16 percent annual return to justify holding this specific asset. Because the stock is slightly more volatile than the overall market, the company must generate strong profits to protect its share price.

How the Cost of Equity Formula Works (Complete Breakdown)

This calculator uses two standard academic equations to measure your required rate of return. Because corporate risk varies based on market conditions and dividend policies, this math compares your specific company inputs against known market baselines to find your true funding cost.

What is the cost of equity formula?

The cost of equity formula calculates the exact return shareholders demand for risking their capital. Financial analysts use two distinct equations. The Capital Asset Pricing Model adds a risk premium to a safe bond rate, while the Dividend Growth Model divides expected dividends by the stock price and adds growth.

CAPM:

Cost of Equity (Ke) = Rf + [Beta * (Rm - Rf)]

Dividend Growth Model (DGM):

Cost of Equity (Ke) = (D1 / Price) + g

These equations translate market risks and dividend payments into a single baseline percentage. The CAPM model scales your risk premium up or down based on your specific stock volatility. Alternatively, the DGM model ignores volatility entirely, focusing strictly on how fast your cash payouts grow over time.

What Each Variable Means in Corporate Valuation

Every value below connects directly to stock market data and corporate financial reports. These specific numbers determine exactly how much profit a company must generate to satisfy its investors.

Risk-Free Rate (Rf)

This represents the guaranteed return from zero-risk government bonds. Most analysts use the current 10-year U.S. Treasury yield as the baseline. It sets the absolute floor for your calculation before any corporate risk gets added.

Beta (β)

This metric tracks how aggressively a company’s stock price responds to broader market movements. A beta of 1.0 means the stock drives perfectly with the market. Higher numbers indicate extreme volatility and risk.

Expected Market Return (Rm)

This is the historical average profit generated by the overall stock market. The system subtracts the risk-free rate from this number to find the exact equity risk premium investors demand.

Current Stock Price (P0)

This equals the exact dollar amount a single share trades for on the open market today. The dividend model uses this current valuation to determine the baseline dividend yield.

Expected Dividend (D1)

This shows the projected cash payout a shareholder will receive per share over the next year. You must use expected future dividends rather than past historical payouts to keep the valuation forward-looking.

Dividend Growth Rate (g)

This tracks the steady annual percentage by which a company increases its dividend payouts. It assumes the business will continue growing its cash distributions at a reliable pace indefinitely.

Another Example Calculation (Step-by-Step)

Let us test the dividend model using a mature blue-chip stock. This helps you understand how steady cash payouts and growth combine to form a required return rate without relying on beta volatility.

Given:

- Current Stock Price = $120.00

- Expected Dividend = $3.60

- Dividend Growth Rate = 4.0%

Calculation:

Dividend Yield = (3.60 / 120.00) * 100 = 3.0%

Cost of Equity = 3.0 + 4.0 = 7.0%

The system divides the $3.60 expected dividend by the $120.00 stock price to find a 3.0 percent base yield. It then adds the 4.0 percent annual growth rate to find the total required return.

Result:

- Dividend Yield: 3.0%

- Cost of Equity: 7.0%

- Status: Defensive Risk Profile

Meaning:

Investors require a 7.0 percent total return to hold this stable dividend-paying stock. The low required yield reflects a highly mature, safe company. Corporate management must ensure new business projects beat this 7.0 percent threshold to create real value.

You Might Also Find These Helpful

Corporate Finance 6

No tools published here yet.

Related Tools People Use Next

Common Mistakes When Using the Cost of Equity Calculator

Financial valuation relies heavily on precise inputs. Even minor data errors in your equity calculations will artificially inflate your company hurdle rate. Avoid these common input traps to ensure your required return accurately reflects true market risk and business realities.

- Entering a short-term bank interest rate instead of the standard ten-year Treasury yield for your risk-free baseline.

- Confusing the overall expected market return with the isolated equity risk premium when building your CAPM inputs.

- Applying the dividend growth model to volatile technology startups that do not issue consistent cash payouts.

- Treating your final cost of equity as the absolute project discount rate rather than blending it into a complete WACC formula.

- Mixing up corporate equity hurdle rates with the standard consumer interest rates charged for residential home equity loans.

Frequently Asked Questions (FAQs)

Why is the cost of equity higher than the cost of debt?

Equity investors take on significantly more financial risk than debt holders. If a business files for bankruptcy, lenders and bondholders legally get paid first during asset liquidation. Shareholders need a higher rate of return to compensate for sitting at the absolute bottom of the payout structure.

What is the difference between levered and unlevered cost of equity?

Levered cost of equity accounts for the extra financial risk added by a company’s existing debt load. Unlevered cost of equity strips away those debt obligations to show the pure risk of the company’s core operations. Analysts use unlevered metrics to compare businesses with completely different capital structures.

Why is it a "cost" if a company pays no dividends?

It represents the shareholders’ opportunity cost. Even if management reinvests all profits instead of issuing cash dividends, investors expect the underlying stock price to grow by that specific percentage. If the company fails to generate that growth, investors sell their shares, destroying the company’s market valuation.

How do you find the cost of equity for a private startup?

Private startups lack public stock prices to measure daily beta volatility. Analysts must find the unlevered beta of comparable public companies in the exact same industry. Venture capitalists also apply massive hurdle rates—often 30 to 50 percent—to account for the extreme survival risk of early-stage investments.

Can the calculated cost of equity ever be negative?

A negative cost of equity is mathematically possible but completely rejected in real-world finance. This anomaly only happens if a stock possesses a severely negative beta. Investors always demand a positive cash return for risking capital, so analysts adjust model inputs if equations produce negative yields.

How does inflation impact my total required return?

Inflation actively drives up the risk-free rate component within the CAPM formula. Central banks raise interest rates to fight growing consumer prices, which directly increases government bond yields. This chain reaction pushes up the baseline floor, forcing your total cost of equity higher across the board.

How do you use the cost of equity formula in Excel?

Financial analysts constantly map these models into spreadsheets. To set up the cost of equity formula in Excel using CAPM, designate three cells: Risk-Free Rate (A1), Beta (A2), and Market Return (A3). Use the formula =A1+(A2*(A3-A1)) to find your required return. For the Dividend Growth Model, input your Expected Dividend (B1), Stock Price (B2), and Growth Rate (B3), then calculate the yield using =(B1/B2)+B3.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.