Actual Cash Value Calculator: Expose Hidden Insurance Depreciation

Actual cash value (ACV) is the brand-new replacement cost of your property minus physical depreciation. Adjusters use this exact math to calculate your initial payout check.

Recent insurance trends show companies frequently use flawed valuation reports or bad local comparables to over-depreciate your assets. A totaled car or damaged roof does not mean you get a new replacement. You still deserve the true market value your item held seconds before the damage occurred.

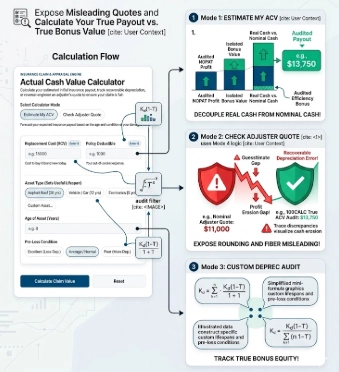

Use this tool to estimate your expected net payout. You can track recoverable depreciation holdbacks easily. The reverse-engineer mode also lets you expose the exact depreciation rate the insurance company applied behind closed doors.

Quick Facts

- Calculates final net payouts after policy deductibles.

- Caps maximum physical depreciation at 80 percent automatically.

- Exposes hidden adjuster depreciation rates instantly.

- Tracks recoverable holdbacks for replacement cost policies.

- Updated Jun 17, 2026

- Reviewed by 100Calc Research Team

Insurance Claim & Appraisal Engine

Actual Cash Value Calculator

Calculate your estimated initial insurance payout, track recoverable depreciation, or reverse-engineer an adjuster's quote to ensure your claim is fair.

Forecast your expected insurance payout based on the age and condition of your damaged asset.

Estimated Initial Check (Net Payout)

Claim Value Breakdown

How do you calculate actual cash value?

How do I find my ACV of my car?

How to calculate the actual cash value of a home?

Where can I find a reliable ACV estimate?

Explore More Calculators

Use this After-Tax Cost of Debt Calculator to find your true effective rate. Factor in corporate tax shields, estimate Bond YTM, and uncover exact…

Try calculatorStop guessing your hurdle rates. Use this Cost of Equity Calculator to run CAPM or DGM models. Expose hidden market risks and find your…

Try calculatorIs that high-yield dividend stock a trap? Use our Gordon Growth Model calculator to find its exact intrinsic value, set buy prices, and expose…

Try calculatorExplore Related Tools

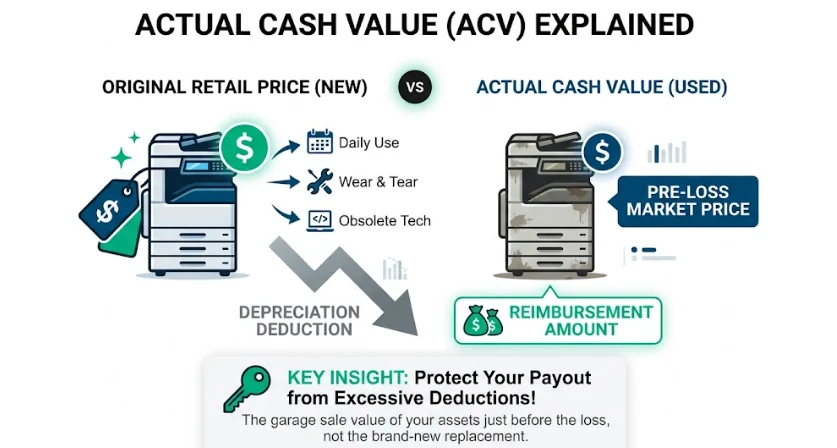

What is Actual Cash Value in Insurance?

Actual cash value is the true open-market price of your used belongings just before a loss occurs. Instead of paying for a brand-new upgrade, insurance providers only reimburse you for the remaining useful life of the damaged property.

Think of this value as the garage sale price of your assets. If you bought a commercial printer five years ago, it no longer commands retail pricing. Daily use, wear and tear, and newer technology naturally lower its overall worth.

When a fire destroys that printer, the adjuster does not buy you a modern replacement. They determine how much that specific five-year-old machine would sell for today. This downward price adjustment is called physical depreciation.

Understanding this concept protects you from unfair payout deductions. Adjusters frequently exaggerate property wear and tear to shrink your final check. Knowing exactly how market depreciation works gives you the leverage to dispute bad estimates and demand a proper settlement.

What Your Actual Cash Value Result Means

The net payout represents the final check you will receive from your insurance company. This number matters most because it shows your exact immediate cash flow after all deductibles and depreciation are subtracted from the replacement cost.

Understanding Your Result

Your base ACV represents the true market value of the item right before the damage occurred. Insurance claims do not cover the cost of a brand-new upgrade. They only reimburse you for the remaining useful life of your specific used property.

If your policy includes alternate cost coverage, you will see a “Recoverable Depreciation” amount. The insurance company holds this exact sum back. They will only release these remaining funds to you after you submit receipts proving you completely repaired or replaced the damaged item.

Is Your Result Good or Bad?

A good result shows a high retained value. This means your asset was relatively new or well-maintained, resulting in a low depreciation penalty. Your net payout will cover a significant portion of the replacement cost.

A bad result shows your net payout equals zero. This happens when the damage costs less than your out-of-pocket deductible. The insurance company will pay nothing, making the entire claim useless.

What You Should Do Next

Compare your estimated ACV directly against the official adjuster quote. If the adjuster’s quote is significantly lower, request their detailed valuation report to check their depreciation rates. Keep all maintenance records and repair receipts safely organized to prove your asset was in excellent pre-loss condition. Never spend your initial ACV check on unrelated expenses if you plan to claim the recoverable depreciation holdback later.

A Quick Example to Test

Let us test a commercial property insurance claim.

Input:

- Estimate My ACV Replacement Cost: $50,000

- Policy Deductible: $2,500

- Asset Type: Electronics (5 yrs)

- Age of Asset: 4 Years

- Pre-Loss Condition: Poor

Process:

The calculator divides 4 by 5 to find an 80 percent base depreciation rate. The poor condition adds a 10 percent penalty, but the system caps the maximum total physical depreciation at 80 percent. The system deducts 80 percent ($40,000) from the $50,000 replacement cost. It then subtracts the $2,500 deductible from the remaining $10,000.

Result:

Net Payout = $7,500 State = Max Depreciation Reached

Meaning:

The damaged electronics had hit their maximum depreciation cap and only retained salvage value. The business owner will receive an initial check for $7,500. The insurance company will hold back $40,000 as recoverable depreciation until the new equipment is purchased.

How to Use the ACV Calculator

This tool determines how much your property is worth today by subtracting age-based depreciation from its brand-new replacement cost. You can estimate a new claim or reverse-engineer an adjuster’s quote to expose hidden depreciation rates.

Select Your Calculation Mode

Choose whether you want to estimate your own expected payout or verify an existing insurance offer. The estimate mode builds a valuation from scratch based on asset details. The reverse mode checks the math on a quote you already received.

Enter Replacement Cost and Deductible

Input the exact dollar amount required to buy the damaged item brand new today. Next, enter your policy deductible. The calculator subtracts this out-of-pocket expense before showing your final net payout.

Define the Asset Profile

Select the type of asset to set its expected useful lifespan. Enter its current age in years. The calculator divides the age by the lifespan to establish a baseline physical depreciation rate.

Adjust for Pre-Loss Condition

Choose whether the item was in excellent, average, or poor condition before the damage occurred. The system adjusts the baseline depreciation up or down based on your selection. It automatically caps the maximum physical depreciation at 80 percent.

Review Your Claim Breakdown

Check your estimated net payout check. Review the interactive visualizer to see exactly how much money the insurance company deducted. The tool isolates your recoverable depreciation holdback so you know exactly what funds you can claim later.

How do you estimate your actual cash value payout for a heavily used vehicle?

Read your replacement cost and note your deductible. To find your true claim value, the system applies age and condition modifiers to depreciate the asset before removing your out-of-pocket costs. Policyholders often struggle to calculate this sequence manually when facing a total loss.

Use these inputs in the calculator:

- Mode: Estimate My ACV

- Replacement Cost: $15,000

- Policy Deductible: $1,000

- Asset Type: Vehicle / Car (12 yrs)

- Age of Asset: 6 Years

- Pre-Loss Condition: Poor

Process:

The system divides the 6-year age by the 12-year lifespan to find a 50 percent base rate. It adds a 10 percent penalty for poor condition. It subtracts 60 percent ($9,000) from the replacement cost to find the ACV, then removes the deductible.

Final Result:

Your estimated initial check is $5,000.

Meaning:

Your car lost significant value due to its age and poor maintenance. The insurance company deducted $9,000 for depreciation and another $1,000 for your deductible, leaving you with a $5,000 net payout check.

How the Actual Cash Value Formula Works (Complete Breakdown)

This calculator uses industry-standard straight-line math to measure physical depreciation. It compares the age of your asset against its total expected lifespan to determine lost value. The final numbers reveal exactly what your property is worth today and how much cash the insurer holds back.

What is the actual cash value formula?

The actual cash value formula calculates the open-market price of a used asset by subtracting physical depreciation from its brand-new replacement cost. Adjusters determine the depreciation rate by dividing the asset’s current age by its expected lifespan. Finally, subtracting your policy deductible reveals your net payout check.

Depreciation Rate (%) = (Age / Expected Lifespan) * 100

Actual Cash Value (ACV) = Replacement Cost (RCV) - Depreciation Amount

Net Payout = ACV - Deductible

This sequence calculates the exact market value of a used asset right before a loss occurs. You divide the age of the item by its expected lifespan to find the base depreciation percentage. The system subtracts that lost value from the current retail price to establish the actual cash value. Finally, it removes your mandatory deductible to forecast your initial payout check.

How Pre-Loss Condition Changes the Math

Your item’s physical state before the damage directly impacts this equation. After calculating the base age-related depreciation, the system applies a condition modifier. Selecting an “Excellent” or “Poor” pre-loss condition automatically adjusts your final depreciation rate down or up by exactly 10 percent before determining your final actual cash value.

What Each Variable Means

Every value below connects directly to your insurance policy and the damaged property. These specific numbers determine exactly how much cash you receive upfront versus how much you must claim later.

Replacement Cost (RCV)

The exact dollar amount required to buy the item brand new today on the open market. Adjusters must base this number on current local prices, not what you originally paid years ago.

Depreciation Amount

The monetary value your property lost over time due to age, daily use, and market obsolescence. Insurance companies subtract this amount from the replacement cost to account for normal wear and tear.

Deductible

Your mandatory out-of-pocket expense agreed upon in your insurance policy. The insurer subtracts this specific amount from the actual cash value before writing your final initial check.

Recoverable Depreciation

The money the insurance company holds back after paying the actual cash value. You can claim these remaining funds later after submitting receipts that prove you actually repaired or replaced the item.

Another Example Calculation (Step-by-Step)

Let us see how the formula works using our ACV calculator for home insurance claims. This will help you understand how depreciation and deductibles impact a high-value property replacement, like a damaged residential roof.

Given:

Replacement Cost (RCV) = $20,000

Deductible = $1,000

Expected Lifespan = 20 Years

Age of Asset = 8 Years

Calculation:

Depreciation Rate = (8 / 20) * 100 = 40%

Depreciation Amount = 20,000 * 0.40 = 8,000

Actual Cash Value = 20,000 - 8,000 = 12,000

Net Payout = 12,000 - 1,000 = 11,000

Your roof lost 40 percent of its value over eight years. The insurance company deducts that $8,000 depreciation from the brand-new $20,000 replacement cost. They then subtract your $1,000 deductible from the remaining $12,000.

Result:

- Actual Cash Value (ACV): $12,000

- Estimated Initial Check: $11,000

- Recoverable Depreciation: $8,000

Meaning:

You will receive an initial check for $11,000 to start your repairs. Because your roof depreciated by $8,000, the insurance company holds that exact amount back. You must finish the construction and submit the final contractor invoices to recover that remaining $8,000 balance.

You Might Also Find These Helpful

Corporate Finance 6

Standard IRR inflates your profits. Use our MIRR Calculator with WACC to calculate true project returns, safely reinvest cash, and find exact NPV instantly.

Try calculatorCalculate your true cash flow with our net operating profit after tax calculator. Strip away debt distortions from EBIT, EBITDA, or Net Income instantly.

Try calculatorAre you growing too fast? Use our sustainable growth rate calculator to find your exact revenue ceiling before a hidden cash deficit ruins your…

Try calculatorRelated Tools People Use Next

Avoid These Insurance Valuation Errors

First, many new policyholders misunderstand basic insurance math. Therefore, you must avoid common claim traps completely. Next, you should understand exactly how our ACV calculator works. Consequently, you will manage your exact property predictions safely.

- Confusing Payout Types: First, many homeowners simply assume guaranteed new prices completely. However, you must never rely on full replacement money safely. Specifically, ignoring your depreciation rules completely breaks your entire financial plan. Therefore, expecting brand new prices causes you to project fake payouts safely. Consequently, you must use our digital tool to protect your exact cash value.

- Guessing the Useful Life: Next, you cannot just guess your item's lifespan safely. Instead, you must thoroughly research standard property years. Consequently, a small age error can ruin your future payout. Specifically, entering the wrong lifespan creates massive valuation problems. Ultimately, rushing the calculation process leaves you with a completely ruined claim.

- Ignoring Physical Condition: Finally, you must record your exact physical wear safely. Specifically, ignoring excellent item condition completely ruins your exact claim strategy. Next, you must check your total depreciation rate perfectly. Consequently, providing excellent daily care helps you safely secure your exact maximum limit. Therefore, failing to apply exact condition proofs destroys your exact ACV calculator results instantly.

Frequently Asked Questions (FAQs)

Is actual cash value the same as replacement cost?

No. Replacement cost pays exactly what it takes to buy a brand-new item today. Actual cash value only reimburses you for what your used item was worth right before the damage occurred. Insurance companies always subtract physical depreciation before issuing an ACV payment.

What is recoverable depreciation?

Recoverable depreciation is the exact monetary difference between the brand-new replacement cost and your actual cash value payout. Insurance companies hold this money back initially. They release these funds only after you submit receipts proving you completed the property repairs.

How do I negotiate an actual cash value offer?

You negotiate by proving the adjuster used incorrect data. Use our reverse-engineer tool to expose their hidden depreciation rate. You can then provide maintenance receipts, proof of recent upgrades, and independent local sales data showing your asset was in better pre-loss condition than they claimed.

Does actual cash value include sales tax and fees?

Yes. In most states, auto insurance companies must include local sales tax, title, and registration fees in your actual cash value settlement. If your adjuster leaves these out of your total loss quote, you should request a revised payout calculation immediately.

Why is my adjuster's car value lower than Kelley Blue Book?

Insurance adjusters rarely use standard consumer tools like Kelley Blue Book. They rely on proprietary software like CCC ONE to find local comparable sales. These corporate systems apply aggressive condition adjustments that drive your final payout lower than standard online consumer estimates.

What happens if my actual cash value is less than my car loan?

If your payout is lower than your remaining loan balance, you still owe the difference to your lender. Gap insurance covers this exact shortfall. Without a gap policy, you must pay the remaining negative equity entirely out of your own pocket.

Is it better to choose an ACV or RCV insurance policy?

Replacement Cost Value (RCV) is almost always the better choice for homeowners and drivers. It guarantees you receive enough money to fully rebuild or replace your property at today’s prices. An ACV policy has cheaper premiums but leaves you paying thousands out of pocket to cover the depreciation gap.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.