After-Tax Cost of Debt Calculator: Expose Your True Borrowing Cost

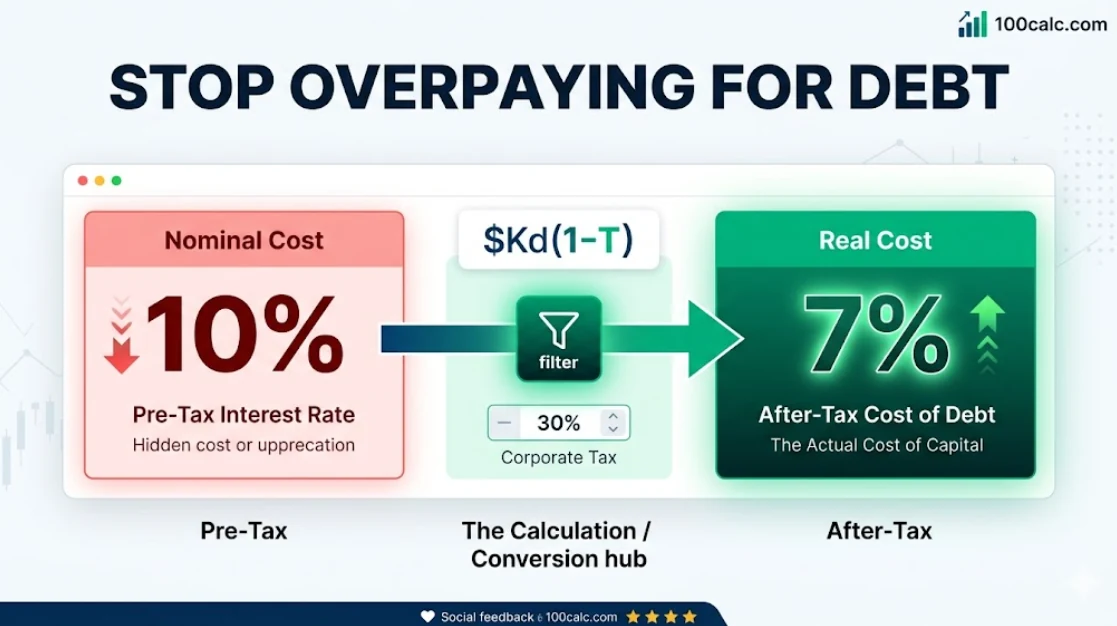

An after-tax cost of debt calculator measures the true financial weight of your corporate loans. It automatically deducts legal tax benefits from your total balance. Business interest payments are tax-deductible. Your quoted bank rate never equals your actual out-of-pocket expense. Our tool converts gross interest into an effective borrowing rate for accurate WACC models.

Are you still using the stated bank rate in your financial forecasts? That mistake artificially inflates your cost of capital. The government actively subsidizes a large portion of your corporate debt. Most business owners fail to extract this exact cash value from their balance sheets.

Enter your interest rate and corporate tax bracket below. You will uncover your true effective borrowing cost instantly. The system reveals the exact dollar amount of your annual tax shield. This confirms whether your current debt structure maximizes your financial efficiency.

Quick Facts

- Invisible Tax Shields: Converts interest payments into immediate cash deductions.

- WACC Integration: Calculates the exact Kd variable for your capital structure models.

- Bond YTM Support: Estimates yield to maturity for accurate public corporate valuation.

- Cash Flow Mode: Isolates real-world interest payments for small business loans.

- Updated Jun 17, 2026

- Reviewed by 100Calc Research Team

Corporate Finance & WACC Tool

After-Tax Cost of Debt Calculator

Calculate your effective borrowing rate and actual cash tax shield. Choose your data type below—whether you have simple percentages, corporate bond data, or flat cash amounts.

Use Simple Rate if you already know your quoted pre-tax interest rate.

Which mode is right for you?

Simple Rate is best for basic loans. Bond YTM is designed for finance students and analysts looking at publicly traded corporate debt. Total Cash is best for business owners who only know their flat annual interest payments.

Effective Borrowing Cost

%

Your after-tax cost of debt estimate will appear here.

The Tax Shield Effect

Math Summary

A direct mathematical summary based on your inputs will appear here.

What does this after-tax rate mean?

Your first dynamic answer will appear here after calculation.

How do I use this in my WACC calculation?

Your second dynamic answer will appear here after calculation.

Explore More Calculators

Are adjusters using flawed reports to lowball your claim? Calculate your true Actual Cash Value (ACV) to expose hidden depreciation and maximize payouts.

Try calculatorStop guessing your hurdle rates. Use this Cost of Equity Calculator to run CAPM or DGM models. Expose hidden market risks and find your…

Try calculatorIs that high-yield dividend stock a trap? Use our Gordon Growth Model calculator to find its exact intrinsic value, set buy prices, and expose…

Try calculatorStandard IRR inflates your profits. Use our MIRR Calculator with WACC to calculate true project returns, safely reinvest cash, and find exact NPV instantly.

Try calculatorCalculate your true cash flow with our net operating profit after tax calculator. Strip away debt distortions from EBIT, EBITDA, or Net Income instantly.

Try calculatorAre you growing too fast? Use our sustainable growth rate calculator to find your exact revenue ceiling before a hidden cash deficit ruins your…

Try calculatorExplore Related Tools

What Your After-Tax Cost of Debt Means

Your result reveals the true financial weight of your company debt. It shows exactly how much you pay after government tax deductions. This effective borrowing cost is the only number you should use for business planning.

Understanding Your Result

This percentage represents your actual out-of-pocket borrowing expense. A bank quotes a gross interest rate. The government lets you deduct interest payments from your revenue.

Your calculated result shows the net rate left over after claiming that tax shield. You must use this lower number to measure your true capital expenses accurately. Relying on the stated bank rate will always inflate your costs.

What to Do After Calculating Your Cost of Debt

Your result is only useful if it drives a better financial decision. If you are building capital structure models, simply copy your final percentage and use it as your after-tax cost of debt formula Excel input for the “Kd” variable. Top analysts use this exact output to determine whether a business should rely on debt financing, issue equity, or restructure existing loans to optimize their overall cost of capital.

A Quick Example to Test

Let’s say a tech company takes out a bank loan to expand operations. Enter these values into the Simple Rate calculator above to see how the tax shield works.

Input:

- Pre-Tax Cost of Debt: 7.5%

- Corporate Tax Rate: 21%

- Total Debt Principal: $500,000

The calculator applies the corporate tax deduction to find your actual expense.

Result:

Effective Borrowing Cost: 5.93%

Annual Tax Shield: $7,875

Meaning:

The bank charges a gross 7.5% interest rate. The legal tax deduction absorbs the 1.57% difference. Your business effectively pays only 5.93% to borrow that money. You also keep $7,875 in cash instead of sending it to the IRS. You must use this 5.93% figure directly in your capital planning models.

Which Cost of Debt Method Fits Your Business?

Your available accounting records determine your calculation method. Finance students analyzing public companies need market-based bond yields. Small business owners usually only know their flat cash payments. Choose the correct method below to ensure your final rate remains completely accurate.

| Calculation Mode | Best For | Required Data | Why Use It | Notes |

|---|---|---|---|---|

| Simple Rate | Basic Loans | Quoted pre-tax rate, corporate tax rate | Fastest way to find effective borrowing cost. | Ideal for quick executive financial reviews. |

| Bond YTM | Public Debt | Market price, coupon, face value, maturity | Required for accurate WACC financial modeling. | Essential for evaluating public market securities. |

| Total Cash | Small Business | Total loan principal, annual interest paid | Focuses strictly on real-world cash flow. | Best for immediate operational accounting audits. |

Micro Insight

Always calculate this hidden tax offset before approving new capital projects. Evaluating a loan using the raw pre-tax rate will artificially limit your company growth potential.

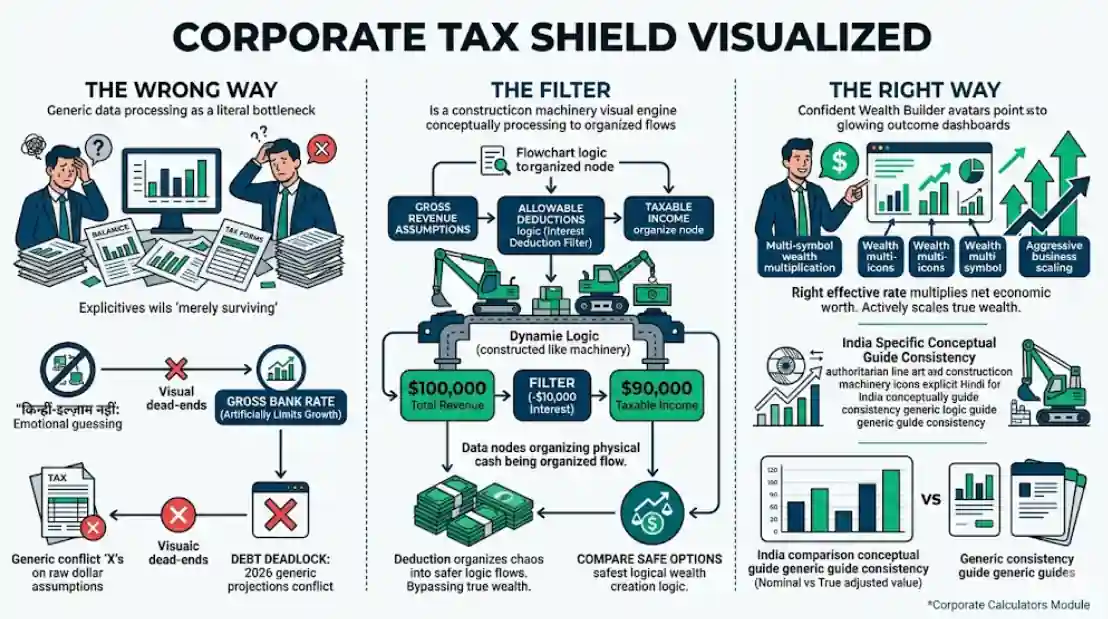

What is a Corporate Tax Shield?

A corporate tax shield is a legal reduction in your company taxes. It happens when you claim allowable deductions like business interest payments. Deducting loan interest from your total revenue lowers your taxable income. This mechanism shrinks your final tax bill and makes debt financing cheaper.

When a business borrows money, the government allows it to write off the interest expense. Imagine your company earns $100,000 and pays $10,000 in loan interest. You only pay taxes on the remaining $90,000 instead of the full revenue amount.

Sending less money to the government means your true borrowing cost drops below the bank rate. This financial dynamic makes debt a highly cost-effective funding source. It usually costs much less than issuing expensive new equity shares to outside investors.

How to Use the After-Tax Cost of Debt Calculator

This tool reveals the true financial cost of your corporate loans. It processes your raw interest rates against your corporate tax bracket. Follow these simple steps to calculate your exact effective borrowing rate and total cash savings.

Select Your Calculation Mode

Choose the data format that matches your financial records. Use the simple rate for basic bank loans. Select the bond option if you are analyzing publicly traded corporate debt. Click the cash option if you only know your flat annual interest payments.

Enter Your Raw Borrowing Costs

Input the gross interest rate your bank charges for the loan. If you selected the bond mode, enter the current trading price along with the coupon rate and face value. The system uses this data to establish your baseline pre-tax expense.

Input Your Corporate Tax Bracket

Add the exact percentage your company pays in state and federal income taxes. The calculator relies on this number to determine the strength of your tax shield. A higher bracket generates a much larger deduction against your overall taxable income.

Add Your Total Debt Principal

Type in the total outstanding balance of your business loan. This field is optional for basic percentage calculations. Adding your exact principal allows the system to extract the real-world dollar amount you save on taxes every single year.

Review Your Final Financial Impact

The system processes your inputs and outputs your true after-tax cost of debt. It drops your quoted bank rate down to your effective out-of-pocket percentage. You can take this final number and plug it directly into your company valuation models.

How do you calculate the after-tax cost of debt from cash flow?

A small manufacturing business only knows its total loan balance and annual interest payment. They want to find their true effective borrowing cost for a financial report.

Use these inputs in the calculator:

- Total Loan Principal: $250,000

- Annual Interest Paid: $20,000

- Effective Corporate Tax Rate: 24%

Process:

The system divides the interest paid by the principal to find the gross 8.0% pre-tax rate. It multiplies this rate by the inverse of the tax bracket.

Final Result:

- Effective Borrowing Cost: 6.08%

- Annual Tax Shield Savings: $4,800

Meaning:

The business pays a raw interest rate of 8.0% to the bank. The 24% corporate tax deduction absorbs a large portion of that expense. The company keeps an extra $4,800 in cash rather than sending it to the IRS. This drops their true borrowing cost to a highly efficient 6.08%.

Accuracy Behind the After-Tax Cost of Debt System

This tool uses standard corporate finance formulas. It processes dynamic bond market variables to estimate Yield to Maturity (YTM) before applying the tax shield. This ensures your final rate aligns perfectly with institutional valuation models.

Key Features & Benefits

- Instantly converts pre-tax rates to effective after-tax costs.

- Estimates Yield to Maturity (YTM) for public corporate bonds.

- Extracts exact cash value of your annual tax shield.

- Supports total cash flow inputs for small business owners.

- Formats output perfectly for immediate WACC integration.

Technical Process

Base Calculation

The system isolates your pre-tax interest rate or estimates the YTM from bond inputs.

Shield Application

It multiplies the pre-tax rate by your inverse corporate tax bracket.

Cash Extraction

It multiplies the tax reduction percentage by your total principal to find real cash savings.

How the After-Tax Cost of Debt Formula Works (Complete Breakdown)

An after-tax cost of debt formula reveals your actual financing expense after claiming government deductions. It multiplies your quoted interest percentage by your remaining tax liability. Mastering this calculation prevents you from overstating your capital costs when building corporate valuation models.

The Financial Cost Formulas

These formulas calculate your exact out-of-pocket borrowing expense. The first equation multiplies your quoted bank rate by your remaining tax liability to find your effective percentage. The second formula scales that rate against your total loan principal to reveal your exact cash savings.

Formula:

After-Tax Rate = Pre-Tax Rate * (1 - (Tax Rate / 100))

Annual Tax Shield = Principal * (Pre-Tax Rate / 100) * (Tax Rate / 100)

Decoding the Equation

This equation isolates the portion of your loan interest that leaves your bank account permanently. It subtracts your tax bracket percentage from the number one to find your net liability multiplier. The second formula calculates exactly how much physical cash stays inside your business due to those interest write-offs.

What Each Debt Variable Means

Each variable in this formula represents a real-world financial metric from your balance sheet. You need your quoted bank rate, your effective corporate tax bracket, and your total loan principal. Combining these specific numbers allows the system to isolate your exact tax shield savings.

Pre-Tax Rate (Kd)

This is the original interest percentage charged by your lender. It can also represent the current yield to maturity on a publicly traded corporate bond. It acts as the starting point for your calculation before any government tax adjustments apply.

Tax Rate (T)

Your company pays a specific percentage in state and federal income taxes. Small businesses often use their historical effective tax rate here. Note that unprofitable startups paying zero taxes receive no tax shield, making their after-tax cost equal to their pre-tax rate.

Principal

This number represents the total outstanding balance of your business loan or bond issue. The system scales your net percentage against this total amount. That multiplication determines your absolute annual dollar savings.

Tax Shield

This value highlights the hard cash saved on your annual tax return. Claiming interest expenses lowers your taxable revenue. You preserve this money for future business operations rather than sending it to the government.

Another Example Calculation (Step-by-Step)

Let us test a standard corporate loan scenario. This example demonstrates how a typical business tax bracket changes the final capital expense. The steps follow standard accounting practices used by financial analysts worldwide.

Given:

- Total Debt Principal = $2,000,000

- Pre-Tax Rate = 9.0%

- Corporate Tax Rate = 30%

Calculation:

After-Tax Rate = 9.0 * (1 - (30 / 100)) = 6.30%

Annual Tax Shield = 2,000,000 * (9.0 / 100) * (30 / 100) = $54,000

Your quoted bank rate drops significantly because of the 30% tax bracket. The business secures a massive deduction that lowers the actual cost of the loan.

Result:

- Effective Borrowing Cost: 6.30%

- Annual Tax Shield: $54,000

Meaning:

A heavy 30% tax burden creates a powerful deduction opportunity. Your raw 9.0% loan transforms into a highly manageable 6.30% net expense. Analysts use this reduced percentage to justify taking on new debt rather than diluting ownership with expensive equity funding.

How do you calculate the after-tax cost of debt?

Multiply your gross interest rate by the inverse of your corporate tax bracket. This simple calculation isolates the exact portion of your loan expenses subsidized by government deductions. The resulting percentage represents your true, out-of-pocket borrowing cost used for corporate valuation.

What is the after-tax cost of debt for a mid-sized retailer?

A retail chain secures a bank loan to open three new store locations.

Use these inputs in the calculator:

- Pre-Tax Rate: 7.0%

- Corporate Tax Rate: 21%

- Total Debt Principal: $1,500,000

Process:

The system subtracts 21% from 100% to find the multiplier. It then applies that figure against the 7.0% base interest rate.

Result:

- Effective Borrowing Cost: 5.53%

- Annual Tax Shield Savings: $22,050

Meaning:

The retailer pays a net rate of 5.53% instead of the quoted 7.0%. They keep $22,050 in cash that would have otherwise gone to federal taxes.

How does a net loss affect the tax shield for startups?

A tech startup borrows money to build software but currently operates at a financial loss.

Use these inputs in the calculator:

- Pre-Tax Rate: 10.0%

- Corporate Tax Rate: 0%

- Total Debt Principal: $500,000

Process:

A zero percent effective tax bracket leaves the net multiplier exactly whole. No deductions take place.

Result:

- Effective Borrowing

- Cost: 10.00%

- Annual Tax Shield Savings: $0

Meaning:

Startups with no taxable income gain zero tax shield benefits. The company must absorb the entire 10% borrowing expense themselves until they become profitable.

How do local businesses calculate effective rates from flat cash payments?

A local bakery owner only knows their total loan balance and yearly interest payment.

Use these inputs in the calculator:

- Total Loan Principal: $200,000

- Annual Interest Paid: $16,000

- Effective Corporate Tax Rate: 15%

Process:

The calculator divides the $16,000 payment by the $200,000 principal to establish an 8.0% pre-tax rate. It then applies the 15% tax deduction.

Result:

- Effective Borrowing Cost: 6.80%

- Annual Tax Shield Savings: $2,400

Meaning:

The bakery owner converts confusing flat cash payments into a clean 6.80% metric. This helps them compare the true cost of their bank loan against other business financing options.

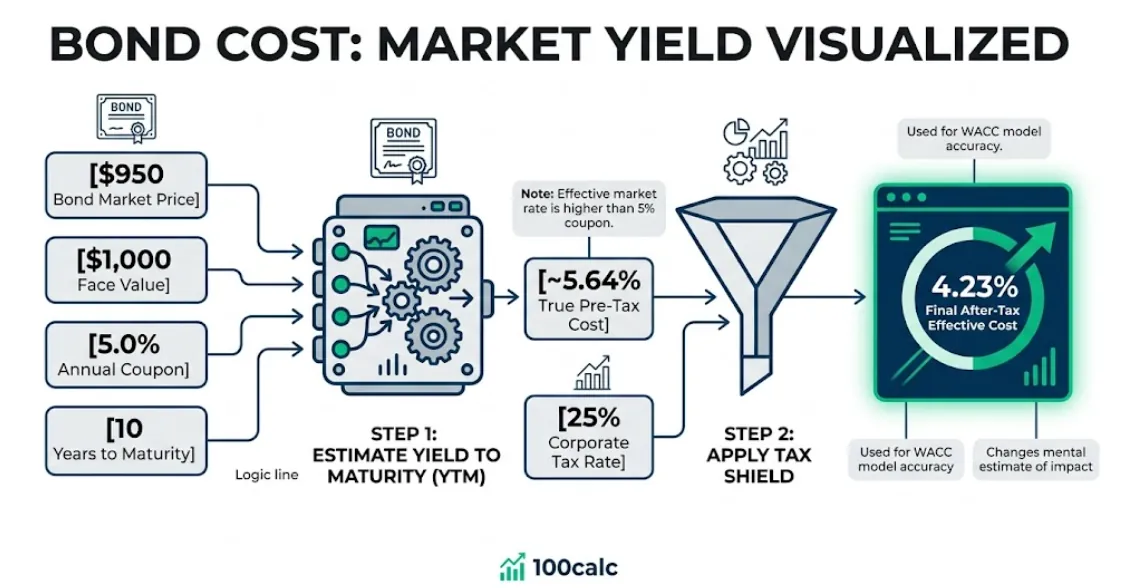

What is the true cost of debt using bond yield to maturity?

A finance analyst evaluates a publicly traded company using current market bond prices rather than historical book values.

Use these inputs in the calculator:

- Bond Market Price: $950

- Face Value: $1,000

- Annual Coupon Rate: 5.0%

- Years to Maturity: 10

- Corporate Tax Rate: 25%

Process:

The system estimates the current Yield to Maturity at approximately 5.64% based on the discounted market price. It then applies the 25% corporate tax shield.

Result:

- Effective Borrowing Cost: 4.23%

- Annual Tax Shield Savings: Calculated based on total bonds issued.

Meaning:

Analysts must use the current market yield rather than the stated coupon rate. A discounted bond pushes the true pre-tax cost up, which slightly changes the final after-tax impact on the WACC model.

Quick rule to remember

Your quoted interest rate is never your final cost if your company generates taxable income. Higher tax brackets create stronger deductions and cheaper debt. Grab your latest loan statement or bond market data, enter your numbers above, and uncover your exact financial standing today.

After-Tax Cost of Debt Result Benchmarks

Your final percentage determines your actual capital expense. A high tax shield makes borrowing highly efficient. Lower tax brackets keep your real expenses dangerously close to the gross bank rate. Review the table below to see where your company stands.

| Tax Bracket | Efficiency Level | Regional Context | Financial Meaning | Strategic Action |

|---|---|---|---|---|

| Above 25% | High Efficiency | Common in high-tax U.S. states and the UK. | The government heavily subsidizes your corporate debt. | Borrowing is highly cost-effective here. |

| 10% to 24% | Standard Shield | Matches the 21% U.S. federal corporate rate. | Provides an average but reliable corporate deduction. | Debt remains much cheaper than issuing equity. |

| Below 10% | Low Efficiency | Typical for unprofitable startups or tax havens. | Delivers minimal to zero tax benefits. | Your true cost equals the quoted bank rate. |

Heads-up: Unprofitable startups paying zero income tax receive no tax shield. Your after-tax cost of debt will equal your pre-tax rate in that scenario.

Interpretation

Most profitable U.S. corporations sit comfortably in the standard efficiency zone. A good result shows a significant drop from your original quoted rate; operating in regions with heavy local income taxes pushes you into the high-efficiency bracket. Conversely, a bad result occurs if your business pays very little in taxes. If your effective tax rate drops near zero, your tax shield disappears entirely and your true cost of borrowing remains very close to the gross interest rate.

Pro Tip

Always use your effective historical tax rate rather than your highest marginal rate for internal planning. This provides a much more accurate picture of your actual cash savings for the upcoming fiscal year.

What to Do After Calculating Your Cost of Debt

Your result is only useful if it drives a better financial decision. The next step is to plug this effective percentage directly into your valuation models to evaluate your capital structure. Top financial analysts use this exact output to determine whether a business should take on new loans, issue equity, or restructure existing liabilities.

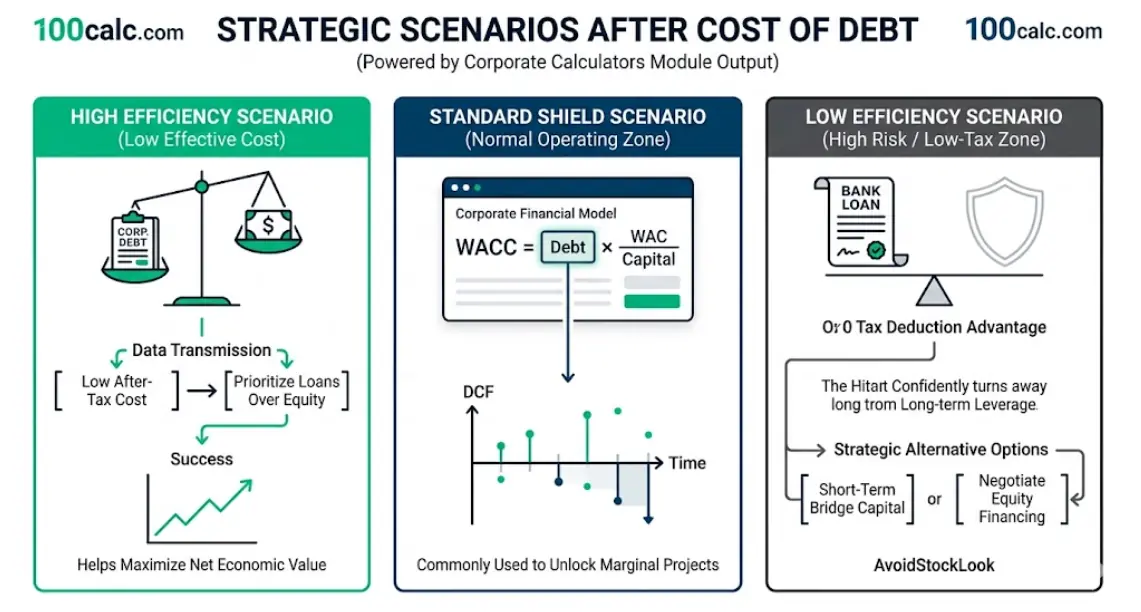

For High Efficiency Results

A high tax bracket creates a massive discount on borrowed capital. If your effective cost is extremely low, debt is clearly your most efficient funding source. You should prioritize taking on commercial loans over issuing expensive new equity shares to fund major expansion projects. Always calculate the projected return on your new investments. Your company actively creates economic value as long as those new projects generate a return higher than this low after-tax borrowing cost.

For Standard Shield Results

This is the normal operating zone for most profitable businesses. Take your final percentage and plug it directly into the debt variable of your Weighted Average Cost of Capital equation. You must use this reduced rate to accurately discount future cash flows. Evaluating new business equipment or real estate using the gross bank rate will artificially limit your growth. That mistake causes managers to reject projects that are actually highly profitable.

For Low Efficiency Results

Unprofitable startups or businesses in low-tax jurisdictions gain almost zero tax advantages from borrowing. Your true cost remains dangerously close to the quoted bank rate. You should avoid heavy leverage until your taxable revenue increases. Focus on securing short-term bridge capital or negotiating equity financing instead of taking on expensive long-term loans. Monitor your effective tax rate quarterly because your capital strategy must shift the moment your company hits profitability.

You Might Also Find These Helpful

Corporate Finance 6

No tools published here yet.

Related Tools People Use Next

Common Mistakes When Calculating Your After-Tax Cost of Debt

Avoid these common financial modeling errors to ensure your capital valuation remains perfectly accurate. Entering incorrect variables or using outdated bond data will artificially distort your corporate tax shield. This simple oversight will completely invalidate your final WACC calculation.

- Inputting the stated coupon rate for bonds instead of calculating the current Yield to Maturity.

- Entering your highest marginal tax rate rather than your actual effective corporate tax bracket.

- Forgetting that personal credit cards and personal loans are not tax-deductible business expenses.

- Relying on the historical book value of corporate debt rather than its true current market value.

- Assuming your effective cost of debt remains fixed even if your company changes tax brackets.

Frequently Asked Questions (FAQs)

How do I calculate the cost of debt using YTM?

Find the bond current market price, face value, coupon rate, and years to maturity to establish the Yield to Maturity. This market yield becomes your base pre-tax rate. Multiply that yield by the inverse of your tax bracket to find your final net cost.

Why is the after-tax cost of debt lower than the pre-tax cost?

The IRS allows businesses to deduct loan interest payments from their total revenue. This deduction actively shrinks your company taxable income and lowers your final tax bill. The cash saved on taxes effectively offsets a large portion of your original borrowing expense.

Can I use this formula to measure personal credit card debt?

No. Personal loans, auto financing, and consumer credit cards do not qualify for interest tax deductions. Without a legal tax shield, your personal borrowing expense always equals the exact gross interest rate charged by your bank.

Where do analysts use the after-tax cost of debt?

Financial analysts plug this exact percentage into the Weighted Average Cost of Capital (WACC) equation. It represents the “Kd” variable. This metric helps corporate teams value companies accurately and determine if new expansion projects will generate profitable returns.

What exactly is a corporate tax shield?

A tax shield is a deliberate reduction in income taxes created by claiming allowable business deductions, like loan interest. It preserves operational capital by keeping hard cash inside your business accounts rather than sending it to the federal government.

Is taking on debt cheaper than issuing new company equity?

Yes. Debt is almost always cheaper because lenders have first claim on your business assets during bankruptcy, making it a lower-risk investment. The legal deductibility of interest payments drives the total cost of debt down even further compared to equity.

Should I use my marginal or effective tax rate for WACC?

Small business owners generally use their historical effective tax rate to measure actual past cash flow. Theoretical corporate finance models prefer the marginal tax rate to evaluate the exact tax savings generated by the next dollar of new debt.

What happens to the tax shield if a startup has no profit?

Unprofitable companies gain zero tax shield benefits. If your business operates at a net loss and pays no income taxes, your effective tax bracket drops to zero. Your after-tax cost of debt will remain exactly equal to your high pre-tax rate.

Why use current market yield instead of the historical bond coupon?

Historical coupon rates represent past financial conditions. Analysts use the current Yield to Maturity (YTM) because it reflects the actual, updated interest rate a company would pay if it tried to raise new debt in today active bond market.

Do bank fees and loan origination costs affect my borrowing rate?

The marginal tax rate is the tax paid on your next dollar of revenue, making it the preferred metric for analysts forecasting new debt financing. The effective tax rate is your historical average, which is much better for small business owners evaluating their past capital structure performance.

What is the difference between marginal and effective tax rate for WACC?

Yes. You must factor loan origination fees and ongoing bank charges into your total interest expense before running this calculation. These extra fees push your true pre-tax borrowing cost higher than the simple interest rate quoted on your loan document.

Questions?

We had love to hear from you! Whether you are reporting an issue, suggesting a new calculator, or exploring collaboration opportunities — we are here to help. Every message helps us make 100calc smarter, faster, and more helpful for everyone.

Why People Trust 100calc

At 100calc.com, we focus on accuracy, speed, and trust. Every calculator we create is designed to give reliable, instant, and easy-to-understand results you can truly depend on.